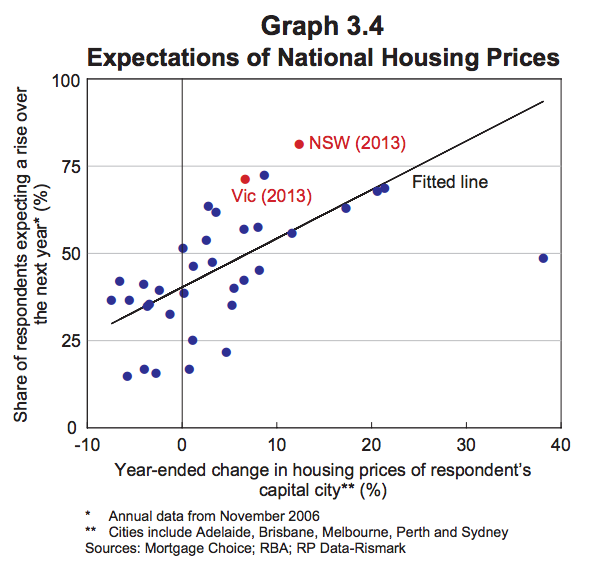

RBA deputy governor Phillip Lowe gave a great speech last night. Lowe is the guy most likely to replace Glenn Stevens when Stevens quits as Governor and it is worth paying attention to what he says.

Last night’s speech was pretty radical. In the guise of a dry discussion of Australia’s balance sheet, Lowe single-handedly deflated arguments for rising house prices.

That puts him in direct opposition to noone other than Prime Minister Tony Abbott. Abbott, of course, said in June “I do hope our house prices are increasing.”

The argument Lowe makes is so smart and so obvious it’s amazing we don’t hear it more often. He starts out by showing that the rise in “house prices” is really a rise in land prices.

“[T]he figures that I have presented invite the conclusion that our national wealth has risen largely because of higher land prices. But is such a conclusion really warranted? Have we really become wealthier as a nation simply because the value of our land has increased?

“[T]he figures that I have presented invite the conclusion that our national wealth has risen largely because of higher land prices. But is such a conclusion really warranted? Have we really become wealthier as a nation simply because the value of our land has increased?

“The answer would clearly be yes if this increase was because we had discovered more land. To my knowledge, though, this has not happened.[7]”

Lowe argues that the rise in house prices is not a nice neat story about the returns to city life increasing. He says prices rose because of financial deregulation and supply constraints.

This creates not a wealth fountain but a money-go-round, he explains.

“from the perspective of society as a whole, much of what is gained on the one hand is lost on the other: there are windfall gains from higher land prices but then everyone pays more for housing services.”

Lowe also reveals that the “baby boomers are ripping off the kids” narrative has some credibility even in that palest of economic ivory towers, the RBA.

“For an older person who owns their own home and has no children, the capital gain from the higher land prices more than offsets the expected higher future housing costs. Such a household is better off. The same is true for owners of investment properties, since they own multiple dwellings on which they earn a capital gain. In contrast, for young homeowners with multiple children, the calculation can look quite different. If they care about the future housing costs of their children, then, in some circumstances, it is possible that the higher future expected housing costs could exceed the capital gain on their dwelling. In a welfare sense, the increase in land prices could make them worse off, even though they own land. The same is obviously true for renters as they do not have any capital gain to offset the higher future housing costs.”

“I think many Australians have an innate understanding of the concept and share the concern. Many parents around the country look at the high housing (really land) prices and worry that their children will not be able to afford the type of property that they themselves have been able to live in, even if their children were to have the same life-time income profile as they have had.”

“So it is arguable that the main impact of higher land prices is not really to increase our national wealth, but to change the distribution of that wealth.”

He goes on to argue that if parents help their kids buy houses, high house prices are perpetuated. But their wealth effect is diminished because the people that have expensive assets are using them as collateral for buying more expensive assets. That is to say the high prices bring no benefit.

If, however, parents don’t help their kids buy houses, and instead spend up big (say on trips overseas) then house prices are more likely to moderate.

This latter scenario, as unpleasant as it may seem to some, is actually the better one for social stability. Because with Australia’s strong immigration profile, not everyone has parents who own property in Australia. The divide between new migrants and established citizens will only grow larger if property wealth is transmitted across generations.