What will the RBA do next Tuesday?

Last year, the RBA left rates on hold. Despite increasing unemployment and modest inflation, the bank decided that “a period of stability” was the best course for interest rates.

At the December meeting of the RBA board, they seemed calm. The statement released said

“…most data are consistent with moderate growth in the economy……. monetary policy is appropriately configured. … the most prudent course is likely to be a period of stability in interest rates.”

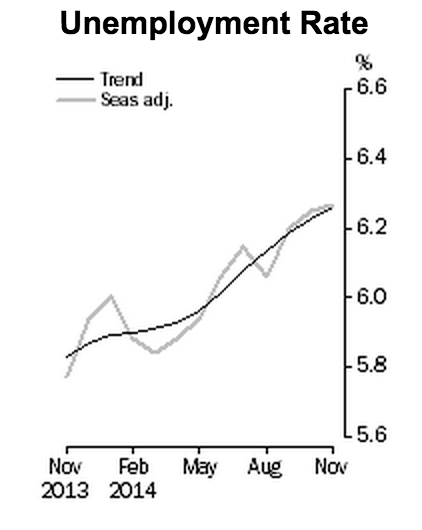

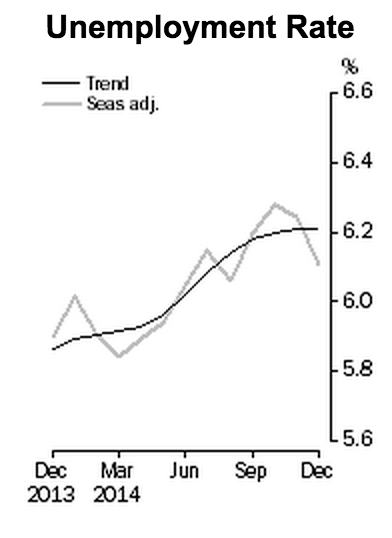

But the meeting was followed the very next day by the release of the National Accounts which showed “dreadful” growth in the quarter, of 0.3 per cent. And shortly thereafter, unemployment figures came out looking like a horror show. Trend and seasonally adjusted measures converged on 6.3 per cent. A record high.

The bank suddenly seemed perturbed. In an interview published by the AFR on 12 December, the Governor said:

“…if at some point we can be more helpful for confidence by doing something different, then obviously that will be on the table, and we will take a fresh look at all these things in the new year”

In the minutes of the meeting, released two weeks after the meeting and four days after publication of that interview, the labour market was singled out:

“…members noted that subdued labour market conditions were likely to weigh on consumption growth and consumer confidence more generally.”

So perhaps Glenn Stevens spent the long summer fretting he’d left the interest rate unchanged for too long. Perhaps he sipped light beer by the pool and bored his bbq guests by extemporising on how a two-month break between the December and February meetings was inappropriate for a modern economy. Perhaps his long summer nights were filled of dreams of a rate cut.

But then the New Year began and with it came more positive news on the economy.

Unemployment, when the December figures were released in mid-January, was suddenly much better.

This gelled with labour market survey findings that showed job advertisements had been rising for seven consecutive months (PDF in link).

At the same time, the Aussie dollar went into freefall. It has gone from US85c at the time of the December meeting to just under US78c today. (under seventy-eight?! oh my god this upcoming American trip is going to kill me.) The speed at which the economy can expand is affected not only by interest rates but also the exchange rate, which are lumped together under the terminology “monetary conditions.”

The lower exchange rate boosts the economy in several ways. Both by making imports less competitive, and by making it easier to export. It should also reverse the enormous disparity between the number of Aussies who go offshore and the number of tourists who arrive. (A lower exchange rate is not without costs, of course, as many goods, especially capital equipment, is imported).

In all these ways, a lower exchange rate does the same work as a rate cut, all without Mr Stevens lifting a finger. Best of all, the lower exchange rate should not lead to higher house prices, which is very welcome as bubbles remain a topic of great importance to the RBA.

Last but probably not least, the falling oil price is going to put stacks of cash in consumer pockets. I filled up the car with glee the other day. Unlike falling interest rates, which rob from savers to give to borrowers, lower oil prices are pure upside for consumer buying power, and therefore a more powerful spur to consumer confidence.

Which is why it’s interesting to see that the actual measure of consumer confidence is down in the dumps, still.

It fell 5.7 per cent in December and recovered just 2.4 per cent in January (PDF in link).

That same PDF, authored by Westpac, predicts two rate cuts this year. But is that really going to happen? For that to come about, the bank would need to have changed.

Inflation was not a major concern and probably won’t be so long as the falling dollar is pushing average prices up, cancelling out the falling oil price.

The bank’s two big worries have been the housing market and the unemployment rate. With house prices still rising at the end of last year, it must surely be frightened of a 2015 full of headlines featuring a median house price nearing $1 million in Sydney. And unemployment looks like easing.

I bet the RBA will leave rates on hold again.

But the one thing that sticks in my mind is this article in the Herald Sun. Business Editor Terry McCrann has a long report on why the RBA will cut interest rates. It is specific enough and well-researched enough to appear to be a leak rather than (like this piece) the author’s own ideas.

McCrann writes:

“The RBA will be reducing both its growth and inflation forecasts in this statement [a report to be released after the board meeting]….

Critically, on (underlying) inflation, the RBA will also make its first point-forecast for June. It is likely to be 2.25 per cent, it could be as low as 2 per cent — either way, significantly, very significantly,below the 2.5 per cent midpoint of its 2-3 per cent target range.

Almost as significantly, it will cut its December forecast inflation range to 2-3 per cent and do the same for at least the first half of 2016.

In short it will be forecasting weakish growth and inflation below target. It quite simply could not release those figures on the Friday and have left its official rate unchanged on the preceding Tuesday. Or at least signalled a pending rate cut.”

If he is right and the forces pushing down on inflation are far greater than those lifting up, then you can’t help but expect a rate cut. It’s an inflation-targeting bank, after all. Tuesday will tell.