When I started studying economics I was 17. Young enough to be arrogantly skeptical of everything I heard. One of the many questions and concerns I had as I chomped through the stale bread of first-year economics was why we would believe that firms in competitive markets would put all their efforts into producing at lowest cost, when they could instead put their efforts into deterring competitors.

What was assumed away in the basic competitive market theory we were learning was that firms will fight hard to protect their space. Few firms operate in the unrestrained markets where they live and die red in tooth and claw. Far more operate in spaces where competitors are kept at bay, by owning a key resource (Telstra, Rio Tinto) or by making sure regulations operate in their favour (Woolworths, Commonwealth Bank). Their operations are run with an eye on costs, sure, but also with an eye on the competition.

Competition matters. Western countries run relatively unfettered capitalism because the prediction of competitive market theory is that capitalism will deliver more happiness, more efficiently. But competition is a key input to that theory. If competition falls short, we must question whether relatively unfettered markets are serving us best.

Some new research from the United States shines an important light on competition.

How America Became Uncompetitive and Unequal is a Washington Post op-ed that summarises a great body of work from non-partisan think tank the New America Foundation. It outlines how mergers and market power see prices pushed up and looks at how firms use their power to suppress workers’ wages.

“While dwindling competition hurts the vast majority of Americans, for the well-off it often proves a path to huge payoffs. Indeed, it has even become a basic formula for successful investing. Goldman Sachs in February published a research memo advising investors to seek out “oligopolistic market structure[s]” in which “a smaller set of relevant peers faces lower competitive intensity, greater stickiness and pricing power with customers due to reduced choice, scale cost benefits including stronger leverage over suppliers, and higher barriers to new entrants all at once.” Goldman went on to highlight a few markets, including beer, where dramatic consolidation over the past decade has enabled dominant companies to use their market power to extract more from suppliers and consumers — and thereby enrich investors.”

“The lack of competition in America inhibits dynamism and risk taking. A New America Foundation study shows that the number of job-creating businesses that Americans start every year fell by 53 percent between 1977 and 2010, when measured as a proportion of the U.S. working-age population.”

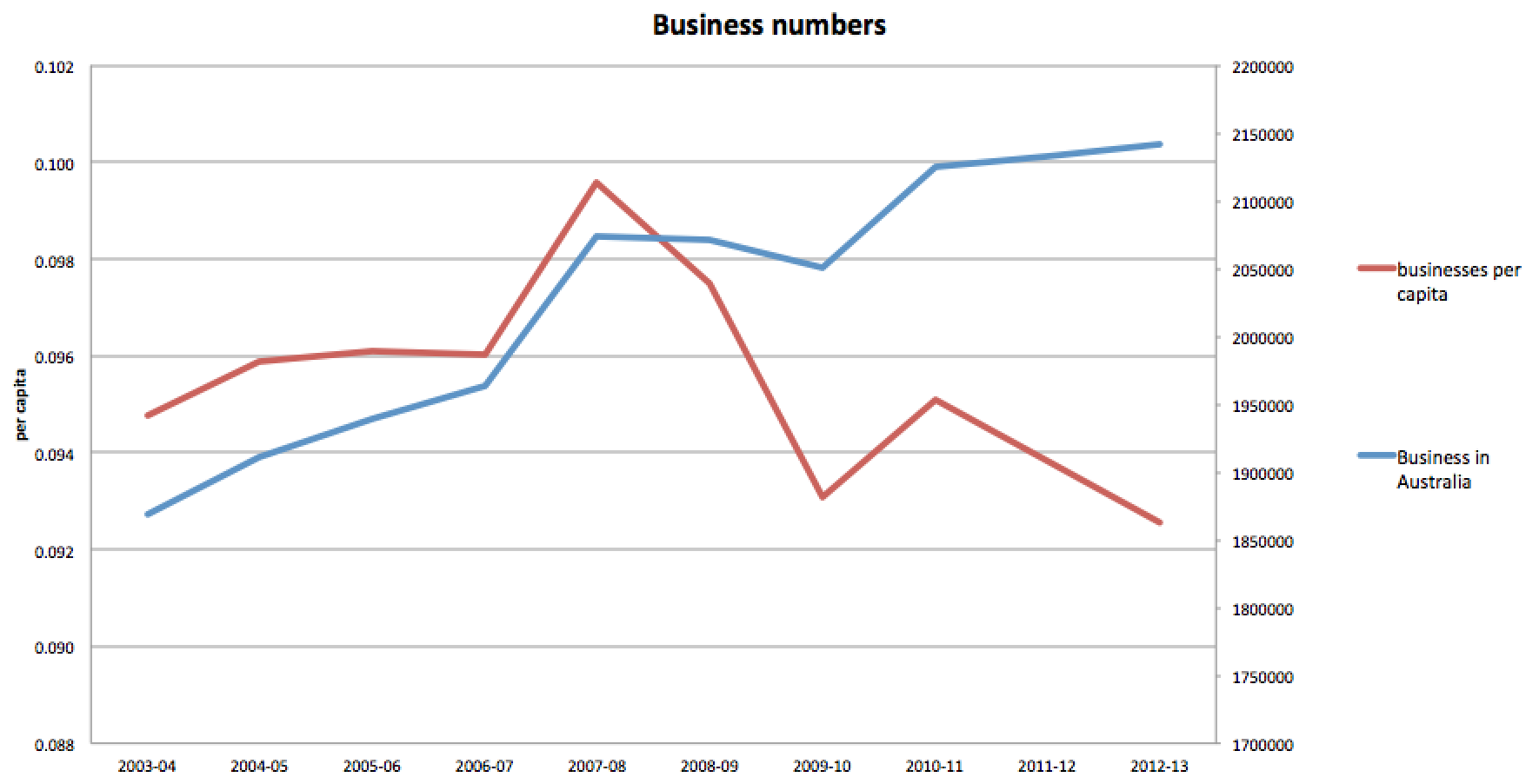

I’ve dived into the ABS figures to see what Australia looks like on the same issue. We don’t have as much historical data as America, but the numbers are just as striking. While Australia is home to ever more businesses, the number of businesses per person has fallen from nearly ten to closer to nine.

The explanation for this is in the willingness of Australians to open businesses. A decade ago, 900 new businesses were registered every day. Now it is under 700.

Bu

This is not necessarily a bad thing. If people can have employment without risking their house on a business idea, then perhaps that’s a good thing. Perhaps something has changed in the economies of scale that mean our economy runs on fewer bigger businesses now.

But the coincidence of rising inequality(1, 2) and higher market concentration makes the application of vigorous competition a huge priority for Australia. If rising inequality is explained by markets becoming more cosy than competitive, that is something we should act on as a matter of urgency.

Competition is something both left and right should be able to get behind. The only people who support market power are plutocrats who grow fat on the cream churned up by insufficiently competitive systems.

Apple’s chance of first-mover advantage is zero. The smart watch market is already quite busy. Samsung and Google have products out. So do others.

smash misses.

None is making much of a splash.

We have a vision of tech breakthroughs as being radical new inventions. But really they stand on the shoulders of others.

Here’s a little extract from an email I got in April 2005, when facebook was still mainly for ivy league students and working on attracting early stage investors.

“I actually don’t know what this Bebo service does, but it looks like some of you are ‘existing members’ so I’m assuming it’s a good thing I need to get on the band wagon with.”

I joined Bebo. I can’t remember if I joined Hi5. I definitely didn’t join MySpace. But I thought about all of them and dismissed their usefulness long before I …

Apple is betting that its smartwatch will be like facebook. That it will enter a market that has been a graveyard for competitors and make them look foolish. You wouldn’t bet on any company that wasn’t Apple being successful. And the Apple of 2009 might have been able to make a smartwatch into a runaway smash hit. But is 2014 Apple equally savvy?

There are clues that the magic began to evaporate when Steve Jobs passed away:

Investors are betting that the combination of fitness monitors and mini-notifications in the smartwatch will be just right. That it will click with the zeitgeist and zoom away until tehre are two types of people. Those who have an iWatch, and those planning to get one.

But when a product already exists in the market, you have to really nail your version to capture the market. That’s an art, not a science, it requires judgment in the 99th percentile, not the 98th. There is evidence a company like Apple can continue to be good for a long time. But can it be very very good? I doubt it.

The iWatch may not turn out not to be a facebook. It could be a hoverboard.

Something from science fiction that is possible to produce, but turns out to have severe limitations.

Not like this.

If that turns out to be the case, the iWatch will be a niche product and eager investors will lose a lot of money on Apple stock.

The World Cup has dozens of sponsors. Companies like McDonalds, Sony and Budwesier, with a combined value of trillions of dollars. Are they wasting their money?

The biggest PR win of the World Cup so far has been by headphone company Beats by Dre.

They got stacks of press when players were banned from wearing their products in the arenas, with FIFA citing Sony’s sponsorship as the reason. (Press examples: 1, 2, 3, 4, 5, 6, 7, 8, 9, 10...)

Here’s the lead from the original Reuters story:

“Neymar likes them Brazil-green. England’s Wayne Rooney, white. Luis Suarez, blue.

Banned from the pitch by FIFA for licensing reasons, the bulky Beats headphones are a favorite for many of the world’s top players, making the World Cup a huge unofficial ad for the company acquired by Apple Inc last month.”

The message is clear: players that are idols to kids around the world really want to wear Beats Headphones – if only the powers that be would get off their back! Somewhere, a PR agent is looking at a payslip with the biggest bonus they have ever seen.

“The company gave hundreds of young women skimpy orange Bavaria-branded dresses before a match between the Netherlands and Denmark. When the women were ejected and a number were arrested under South Africa’s Contravention of Merchandise Marks Act — an anti-ambush marketing law passed in advance of the country’s World Cup — the reaction sparked an international backlash that brought the company loads of free media attention.”

McDonalds is a major sponsor of the World Cup, but appears to be trying to run an ambush marketing campaign anyway, by making tie-in products with names they could have used even without buying a sponsorship.

Wasteful?

Coke and Pepsi are also battling it out for pre-eminence. Pepsi’s Rio-based ad shows that no matter how much you fence off a sponsorship, you can’t own the concept of football, the town where a tournament is based, or the personalities that bring it to life.

Formal association with the tournament means dealing with FIFA – nothing to be proud of. Meanwhile, being associated with Lionel Messi is unambiguously good marketing.

If I were a shareholder in McDonalds or Coca-Cola, I’d understand. These are massive legacy brands that don’t want to yield an inch to competitors. But for the likes of Sony, Hyundai and Adidas, the decision to sponsor reeks of timidity and a lack of creativity. If they can’t think of a better way to spend their marketing dollar they should probably save it instead.

Melbourne’s weather is poor. It rains often. The city is huge – 100 km from edge to edge – and vast swathes of it are covered in the kind of densely packed contour lines that make cyclists legs tremble.

In winter, Melbourne’s cycling community shrinks by over a third.

On days like today I suspect the number of cyclists is far smaller.

In short, Melbourne will never be the sort of city where 50 per cent of trips are possible by bike. Cycling (and walking) will never ever do the “heavy lifting” in our transport mix. That role will always be split between public transport and private motorised transport.

At the moment, the mode share split between these three is:

Source: 2011 census

And the trends are these:

Cycling is growing fast, more than doubling in eight years.:

The data is tough to aggregate, but one estimate is that roads get four times the investment of public transport.

All the modes are growing. How do we decide what the data means? And why not let the market decide what modes live or die?

The answer to the second question is that transport is going to be a centrally planned space until we can charge users per kilometre.

Public roads built to accommodate cars push the whole investment process into the world of “second-best.” If subsidising roads is a given, subsidising public transport can be efficient. Subsidising public transport makes policy makers wonder if there are other, cheaper ways to move people around, like bikes.

So if we’re going to be centrally planning our transport mix, we must ask: do we like the current 78/17/5 mix?

I’d argue we should not. I’d argue we should be aiming to grow the share of modes that have fewer negative externalities and greater returns to scale.

I’d hazard a guess that for Melbourne, 10 per cent share evenly split between walking and bike, 30 per cent for public transport, and 60 per cent for cars would be optimal.

Does that mean we should start spending 10 per cent of infrastructure funding on active modes, 30 per cent on public transport and 60 per cent on cars?

Only if we want to move very very slowly.

Infrastructure lasts a long time. That means the stock of existing infrastructure is the single biggest determinant of infrastructure in five years time. Marginal changes in expenditure rates affect outcomes only very gently. If we want to effect change, we need to tip the scales massively in favour of the modes we want to grow, in the short term.

In the short term, we could probably usefully spend 60 per cent of the transport infrastructure budget on public transport and 15 per cent on active modes. If we did that for a few years, we would move swiftly towards the outcomes we want, before returning to a “maintenance” split, where expenditure is based on usage.

Spending even $500 million a year on bicycle infrastructure might seem like a lot when the recent budget has been around $30 million. But when you look at what passes for “bicycle infrastructure” and imagine replacing it with global quality bicycle infrastructure, it would be a drop in the ocean.

“Bike boxes” were the sine qua non of Melbourne bicycle infrastructure innovation just a few years ago.

I don’t imagine gold-plated bicycle infrastructure should go everywhere. Far from it. Cycling infrastructure should be optimised in the areas where cycling can thrive, likely to be areas that already see some bicycle traffic. Fixing missing links, creating Copenhagen lanes on major on-road routes, plus widening and lighting off-street bicycle paths would be the top three priorities.

If we want to increase the share of some modes, we need to be bold about throwing money at them, and not be afraid to acknowledge that such a move comes at the expense of other modes.

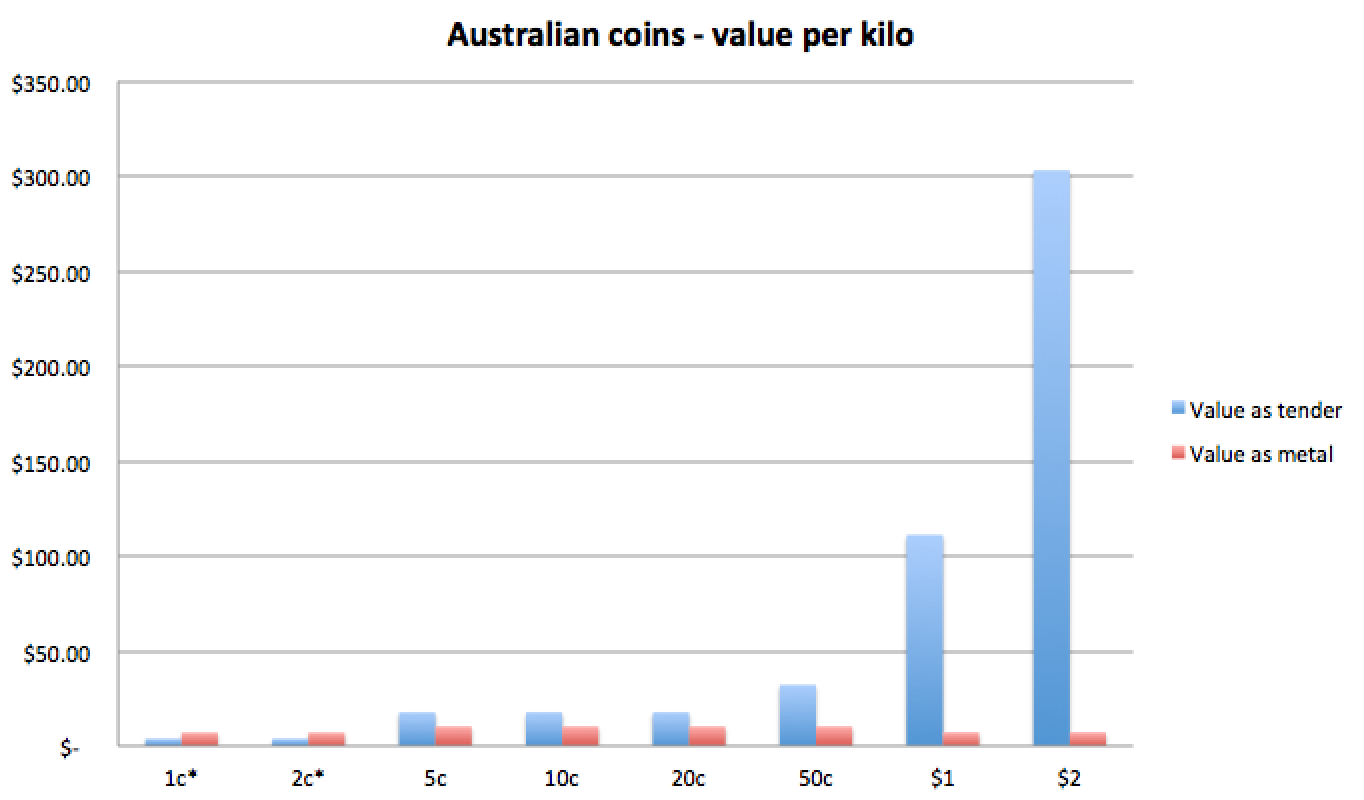

The Australian coin system is all wrong. The weight and bulk of our coins is disproportionately high, to the extent that some are worth over half as much as raw metal.

The 5-cent, 10-cent and 20-cent coins, which have a value of just $17.70 a kilo, are the worst offenders.

The economic damage wrought by Australia’s hefty loose change situation is serious, and I offer as exhibit A my old wallet, which had to be held together by electrical tape after the coin section busted its stitching.

But it’s not just purses, wallets, and pockets being busted by heavy coins. Think of the petrol cost as armoured vans deliver tonnes of change around the city, especially to big coin users like supermarkets, pokie venues and public transport ticket machines.

Even the Royal Australian Mint is at risk if copper prices rise. Copper represents 75 percent of our silver coins and 92 percent of our gold coins. The profit (seigniorage) that the mint makes on selling coins to the RBA was a not-insignificant $96 million in 2012-13. It would be crazy to put that upside at risk for the sake of big fat coins.

During 2011, it looked like our coins might soon be worth melting down.

The solution to these problems is obvious. Smaller coins. We have the answer in front of our noses, in the shape of our $2 coin, whose outstanding value-to-weight ratio makes it the Bradman of coins.

The $2 coin is the only one you’re actually pleased to find in your wallet. Introduced in place of the two dollar note in 1988, it’s worth keeping around. You never take a handful of them and dump them into a jar.

The second best way to carry around two dollars in coins is nearly three times heavier

The Canadians call their $2 coin a Toonie, yet for some reason, this nickname-mad nation has yet to come up with a diminutive for our Mighty Two.

If we want to try to make our coins a bit more like the Mighty Two, we need not look far afield for a model. In 2005 New Zealand got rid of 5¢ coins and changed its 10¢, 20¢ and 50¢ coins from copper and nickel to plated steel. Their new coins are much smaller and much lighter than ours.

Extinct kiwi specimens.

Businesses who have to heft big bags of change back from the banks would welcome the change – you might imagine only the vending machine industry would object. But even they are increasingly moving towards electronic payments, because the industry wants to cut costs by diminishing the frequency with which it collects coins from its machines.

The argument for smaller coins is a simpler one than the argument for getting rid of the smallest denomination.

If you try to get rid of the 5-cent piece, everyone gets up in arms about supermarkets rounding up the price of things to the nearest ten. Never mind that this argument doesn’t hold water. It’s what keeps the pennies circulating in the US, and 5-cent pieces in Australia. The case for smaller coins is much simpler.

I remember third-year economics. The lecturer played some sort of Wheel of Fortune game where he had students answer questions correctly for the chance to guess a letter. It was around the time we were learning about how markets would reach general equilibrium if left alone. The eventual phrase spelled out “Don’t screw with our markets.”

“It’s beautiful,” said the lecturer as he delivered the mathematical proof.

“Why can’t the arts students just see this!” exclaimed the girl in the row in front of me.

Classical Economics has some beautiful theories.

John “beauty is truth” Keats may well have been a free-marketeer. But beautiful theories are a trap.

The human brain has a wide range of biases, the most risky of which is a conclusion bias. We are inclined to latch on to an answer as soon as possible, which then goes on to frame our subsequent information gathering and processing.

Of course, a beautiful unifying theory will be very tempting for us. Succumbing to that temptation explains a lot, from biblical literalists, to libertarians and communists.

But the real world is very messy, and the project of the entire enlightenment is to get us engaged with that complexity and put aside our tendency to simplify.

Some of the most intuitively appealing theories in history (e.g. from each according to his abilities, to each according to his needs) have proved unworkable.

The point I’m driving at is well encapsulated by the parable of the fox and the hedgehog. An ancient Greek Poem turned into an essay by Isaiah Berlin, the Fox vs Hedgehog debate has been given a new life by statistical guru and seer Nate Silver.

It classifies people into two groups, foxes – who rely on lots of little scraps of knowledge, and hedgehogs, who know one big thing. Nate Silver shows that in making predictions, having one big belief can be a block to seeing the future well, and being a fox is the better approach.

(Of course, that itself is a simplification, and a truly foxy approach will accept there are times when a big simple truth is just that: big, simple and true.)

I raise this issue now because I see two big examples where a simple, hedgehoggy application of economics seems to be taking sway.

1. Our federal government. A political fox willing to try anything to get into power, Tony Abbott turned into a policy hedgehog after occupying the Prime Minister’s Office. His latest budget is the repetition of one simple trick: apply market forces. From higher education to GP visits, via cuts to social security payments, the Budget tries to fix Australia by allowing the power of markets to seep in.

It’s not nuanced but it is no doubt deeply satisfying to those elements of the base for whom the solution to the world’s problems is obvious.

2.Piketty. A French economist working on inequality, Mr Piketty has made an enormous splash in 2014. His very long book entitled Capital in the 21st Century considers a lot of evidence and distills it to one simple equation: r>g. That posits that the growth in inequality is due to a mathematical problem – the return on capital (r) is higher than the rate of growth (g). Existing stocks of wealth grow more than the paycheques of workers and so the world grows more unequal.

I do not claim to be smart enough to prove that r<g, or that applying market forces to government services will always undermine them. But I hope to be smart enough to watch the debates unfold while remembering that a simple answer pleases a simple mind.

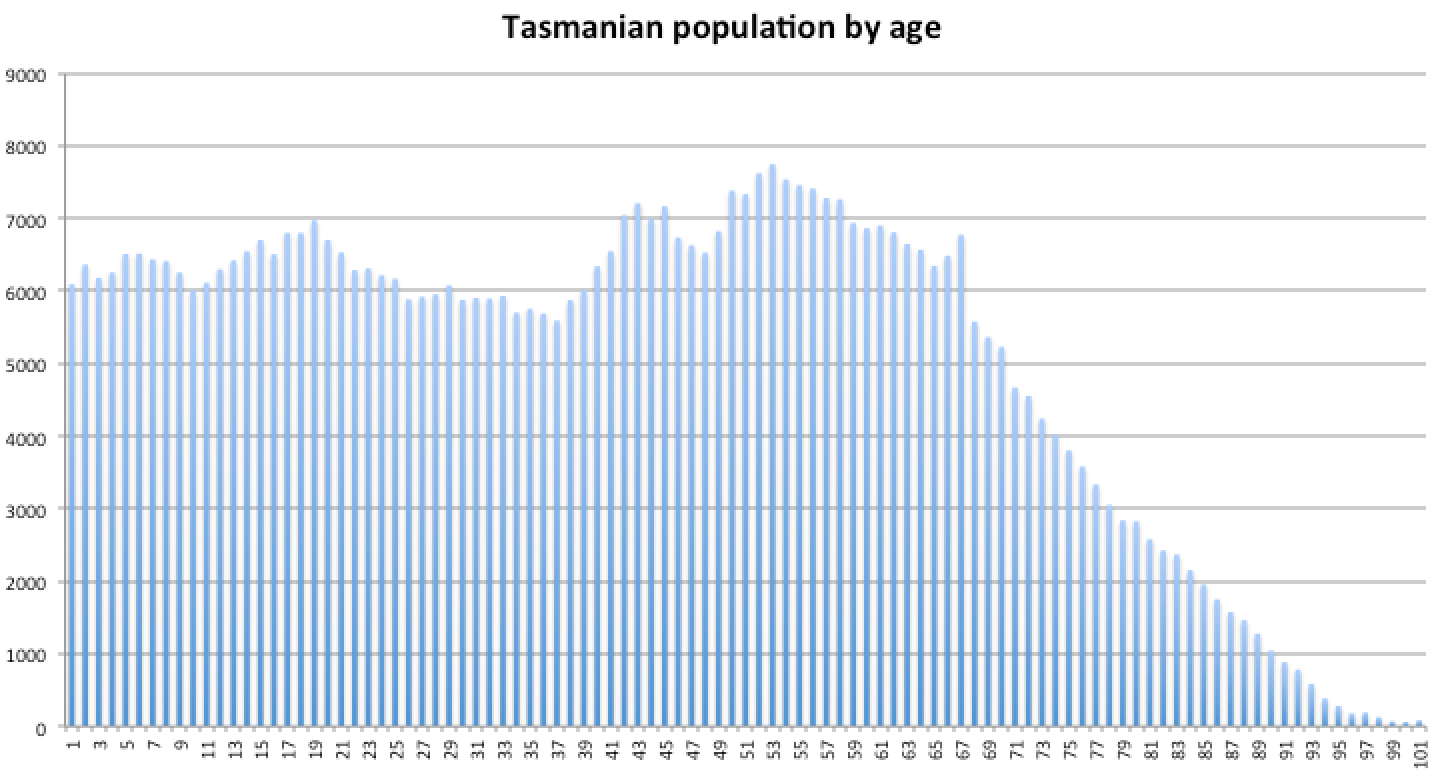

Even though a similar property in Melbourne would cost probably seven times as much, a multi-million dollar saving is apparently not enough to actually tempt people to live in Hobart.

Demographic data out today show the Apple Isle circling the plug hole. Its population growth rate is not far from zero, and people continue to leave in large numbers.

In the 36 years since 1981, Tasmania has managed to actually lose people to interstate migration, despite the Australian population more than doubling. They’ve been saved from extinction by overseas migration and the birth rate. But will that continue?

The entire state has managed just 700 babies in the last six months, an amazing new low.

The Tasmanian fecundity shortfall looks especially stark when you compare it to other states. WA has had 9800 babies in the last six months.

The reason for Tassie’s child shortfall is not unguessable: Too few mums and dads, and too many grandmas and grandpas.

How does Tasmania break out of this cycle? If mainland house price growth continues, there should eventually be push factors. Once the price of new housing in country Victoria and outer Melbourne starts to be much higher than the price of new housing in Tasmania, people might start moving there.

Also if climate change picks up, Tasmania will offer the last temperate zone in Australia.

Essentially, the lesson of migration everywhere is that most people (except retirees) will move for jobs. That’s something Tasmania has too little of.

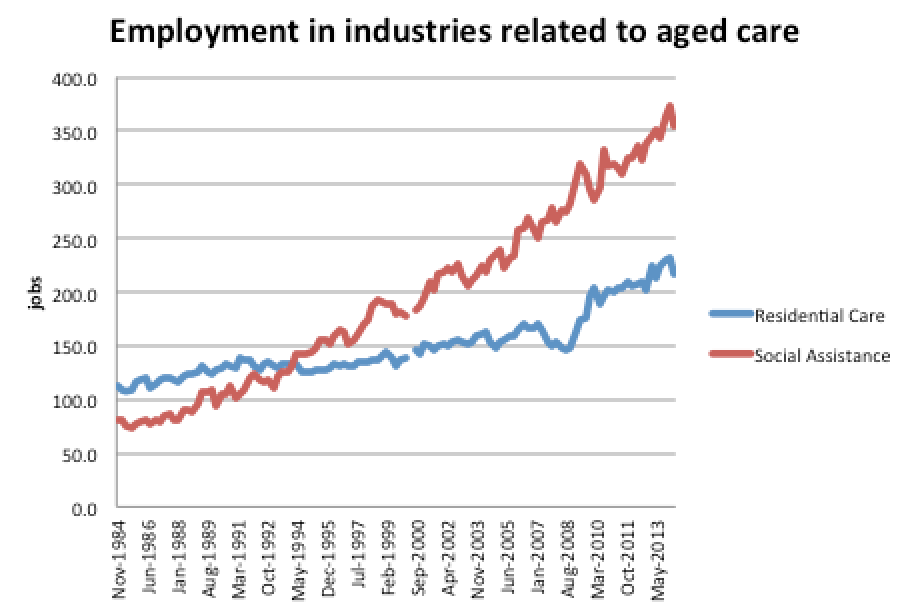

How to fix? There are glimmers of hope in the data above. Australia’s next big boom will be looking after the aged. If Tasmania can turn itself into Australia’s Florida (the place to move when you retire), there should be lots of jobs in aged care.

It just needs to convince the mainland-dwelling elderly that if they don’t want to work all the way to Tony Abbott’s new pension age, they should downsize to a much cheaper house on the other side of Bass Strait.

That would bring an influx of wealth to the island, and provide for a lot of jobs. The aged care industry is already showing a lot of growth.

Can the Apple Isle fill those creaky old Hobart mansions with happy retirees? The key to Florida’s success has been “Weather, effective marketing, low taxes and a herd mentality.” Tasmania can match two of those already (good marketing and a retiree flow). Lower stamp duty for over-55s buying a new property might be a good policy move.

As for the weather? It can’t do much more than it’s doing already, by logging those virgin forests and exacerbating climate change.

The state government is prepared to make big investments to make train travel easier and faster. So they should. They are contemplating a $9 billion tunnel that will make journeys faster and more reliable.

But what if I told you there was a much much cheaper way to improve travel times of the rail system, while making people’s journeys to work more comfortable?

The solution requires thinking outside the box. This is not about putting faster motors on the trains. Not about improving signalling or driver training or anything to do with the train system itself. It’s about cutting walking times to the station.

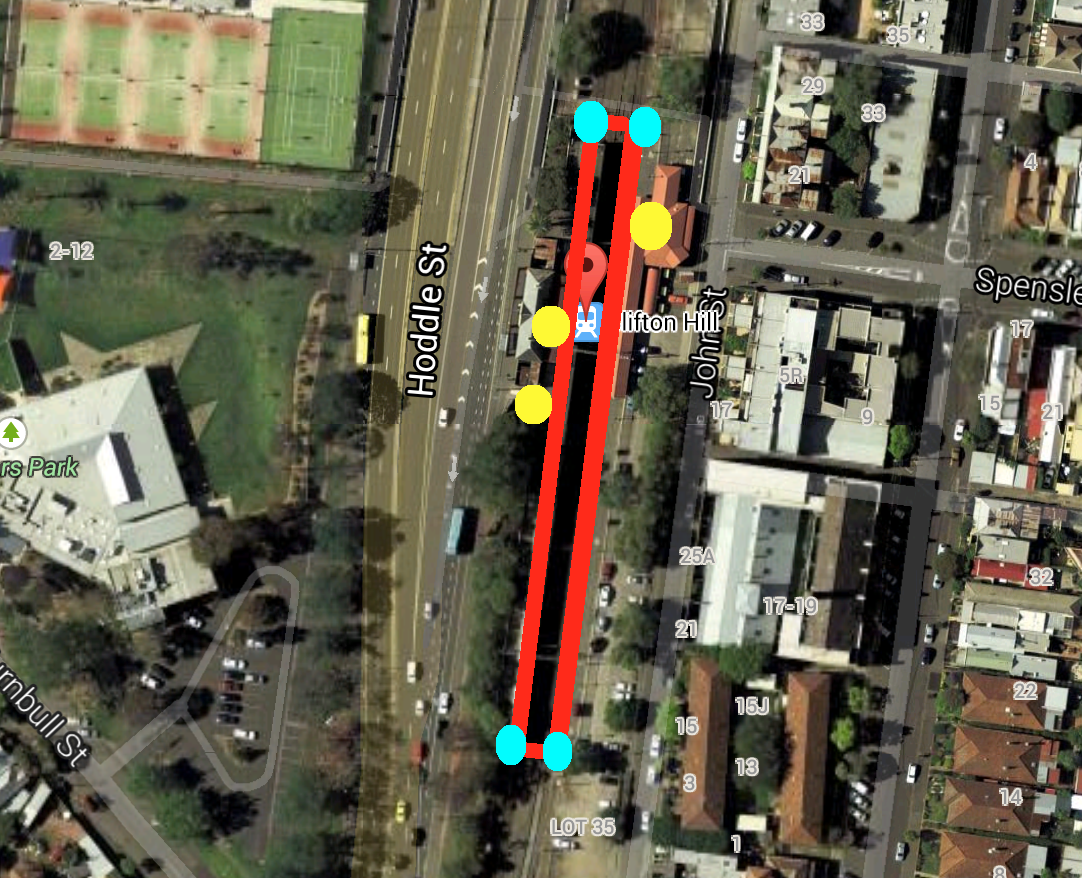

Let’s look at my local station, Clifton Hill.

Yellow dots mark the entrances

There are just three entrances, all clustered up the northern end of the station.

Placing the entrance at the northern end means passengers walking from the south have to walk an additional 120 metres to get on the platform. (I reckon 2 minutes is an overestimate by our friends at Google Maps.)

This is not a passenger-centric design, but an operator-centric design.

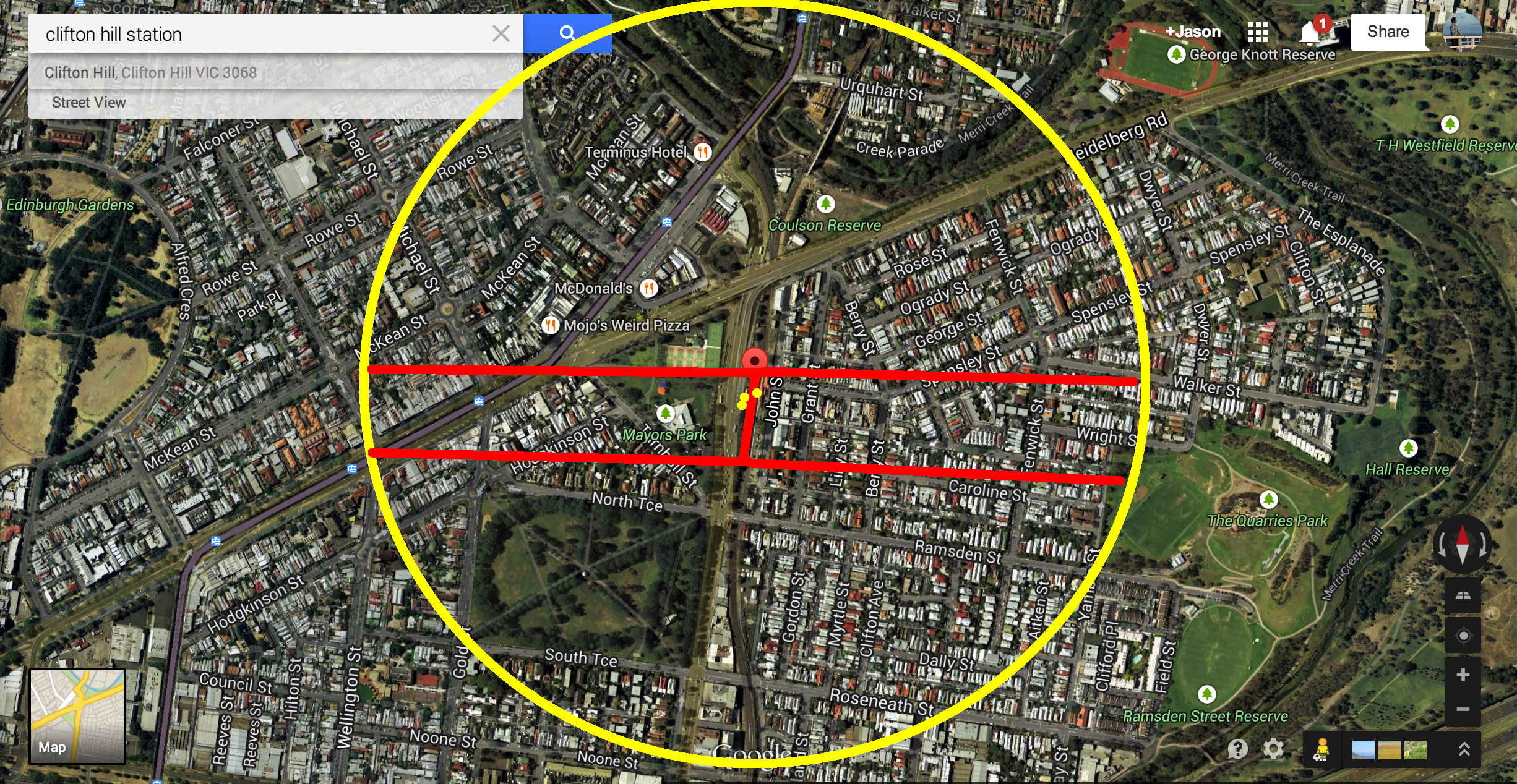

I’ve made a model for the benefits at Clifton Hill station. Clifton Hill Station got 3,009 boardings per weekday in the 2011-12.

I model it like this: 25 per cent of the users who walk to the station live in line with the platform, so moving entrances to the end is of no benefit, while 75 per cent of users currently walk past the end of the platform to get to the entrance. An amazing isochrone map app I found shows that my model is probably conservative, because of the local geography.

Those inside the yellow circle and not between the red lines can be assumed to benefit from new platform entrances.12-minute walking map. Source: Cartoo

There are 90 car parks at Clifton Hill Station, and it is served by buses. There are trams not so far away. I estimate two-thirds of people walk to the station. (2000 users a day.) Let’s say 1500 of them could potentially access the station via the new gates I propose.

But smart public transport users know not all carriages are equally useful. Depending on what station you get off at, and where you’re headed, your train exit may be speeded up most by being at the front, back, or middle of the train.

If you come to Clifton Hill Station from the south, but you want to board the southbound train’s last carriages (and you’re not running late) it provides you no advantage to have an extra gate at the south end of the station.

But if you’re coming from the south and you want to be in the front carriages of that southbound train, you need to walk that distance twice. Once along the street outside the station, and then back again along the platform.

Putting an entrance at each end of the platform, replacing a northern-end entrance

–

WALKING DISTANCE SAVED (m)

–

Southerners

Middlers

Northerners

front carriage riders

150

0

0

mid train riders

75

0

0

last carriage riders

0

0

0

12 per cent of the 2000 walkers will save a conservatively estimated 150 metres, or 90 seconds. 12 per cent of them will save an estimated 75 metres, or 45 seconds. That adds up to 563 minutes on access to the station. That makes 9.4 hours. If the same effect is present when they return home, it’s worth 18.8 hours.

The model does not assign any benefit to all the trains that may now *just* be caught when before they were just missed.

Assuming a value of time of $30 an hour, the value of the additional exits would be $146,000 a year, just measuring weekday trips. For a gap in the fence, a bit of concrete paving and some extra Myki machines, which I estimate to cost perhaps $500,000, it would pay itself off within a few years, yielding a positive rate of return.

You may think a minute here or there is not important, but there is no single change that can cut a train journey’s duration in half. If we want improvements to service we need the operators to accumulate small easy changes like this across the network.

Clifton Hill Station is not even the worst offender. Camberwell station has the entrance to two of its three platforms about 100 metres away from the main road it serves.

Camberwell station served 6,571 passengers each weekday in 2011-12.

Why haven’t they thought of these fixes already?

There will be a perceived trade-off with safety. I don’t doubt the ex-post rationalisers are currently saying “but having one entrance allows for surveillance!” But a single entrance also funnels station users past a single choke point. In the same way a narrow alley feels dangerous at night, so can a single station entrance with no alternatives.

In fact, more exits and entrances should mean fewer people spending time at stations, increasing the visibility of anyone loitering with malicious intent and decreasing their opportunities.

I contend the reason this sort of station design is not widespread is institutional. The Public Transport Victoria guidelines for station design seem to support this kind of solution:

“Many aspects of the local context and surrounding urban design will influence the station entry configuration. A thorough study of the station catchment area is required to determine the most appropriate placement of the entry or entries in order to attract patronage by:

a) Encouraging the use of the station by simplifying connections with existing and future urban design;

b) Providing accessibility, convenience, clarity and quality of arrival to and from the station;

c) Providing safe and attractive public spaces that contribute positively to the local identity;”

But in fact, station access runs second to concerns over train boarding patterns. PTV tries to alternate whether station entrances are at one end of the train or the other, to prevent any one carriage getting too full. Their conception of their job focuses on the trains, not the passengers.

But building more station entrances should be a priority. It won’t help just walkers. At the margin, making walking distances to train stations shorter will encourage more people to walk, and free up scarce car parking spots for people who live even further away.

As well as institutional bias from the departments, there is a ribbon-cutting bias in public transport investment. Politicians want grand visions. The Premier can’t imagine himself showing up to the construction of a new station entrance, so he doesn’t push for it to get done. But that doesn’t mean it’s not the best idea.

Doubling the amount of time poor kids in Chicago spent studying algebra in grade nine led to an 8 per cent increase in their high school graduation rate, and an 11 per cent increase in college enrolment.

Given that US high school dropouts die earlier than graduates by 3-5 years and make up 7 out of 10 prisoners in the US, it is fair to argue that for thousands of these kids, algebra has saved their life.

The paper exploits a natural experiment whereby students in the Chicago Public School System were placed into double dose algebra classes (largely replacing music or art classes) if they scored below the national median on an eighth-grade math test. The researchers compare kids just above and below the cut-off.

The numbers of students in the algebra courses is substantial, because maths skills are thin on the ground in the 73 public high schools studied. In the US, just 20 per cent of hispanic students, 13 percent of black students, and 17 per cent of students poor enough to qualify for free lunches are rated proficient in maths. In the Chicago Public School System 90 percent of students are black or Hispanic.

“In the Chicago Public Schools (CPS), the focus of this study, roughly half of high school freshmen fail at least one course, with the highest failure rates in math courses”

Schools assigned weak students to a back-to-back lesson in Algebra with the regular algebra teacher, and gave the teachers professional development, permitting them to use different instruction methods, including working in small groups, solving problems verbally, and having students set problems for each other.

The impact on test scores was modest. But the impact on the students lives was not.

“…the test score impacts of this policy dramatically understate its long-run benefits as measured by educational attainment.”

The effect of double dosing in the first year of high school remained over time. Students who were in the program were 9.3 per cent more likely to pass algebra in that year. But they are also 7 per cent more likely to still be in school in the fourth and final year of high school.

The students who got the most out of the instruction were ones with poor reading skills. They end up passing three more subjects in high school on average, after taking the double dose, creating a 13 per cent increase in the number of poor readers who complete enough subjects to pass high school. The researchers suggest that the focus on using verbal methods to solve maths problems may explain this result.

Black students who got the double dose also saw a dramatic effect, with a 15 per cent increase in college enrolment. For the double-dose population at large, the increase was 11 per cent. The effect can be seen in this chart:

For some of these student, the impact of these classes – which their 14 and 15 year old selves no doubt dreaded – will be dramatic over their life times.

Australians are living with their parents longer and longer, and prospective empty-nesters might be pulling their hair out if they saw the latest data.

Just 48.2 per cent of people aged 18-24 in 2001 moved out of their parents home by 2011. And what’s more, 8 per cent of those aged 25-29 in 2001 had moved back in with their parents by 2011.

The data come from HILDA, an absolutely amazing study by the good folks at the University of Melbourne. It follows thousands of people through their life, to deliver data that are richer than the regular snapshots from the ABS.

The trend is global and its causes are probably economic. The ratio of minimum wage to rent suggests moving out of home is hard.

I would have done the above graph for house prices too, but the line would go down so fast you’d have to scroll a long way to see it all, and I don’t want my readers getting RSI in their scrolling fingers.

Anecdotally, high house prices pin kids to the parental home in another way too. To buy a house you need a deposit. The best way to save for a deposit is to stay at home for a long time (or return home – this generation is called the boomerang generation for a reason).

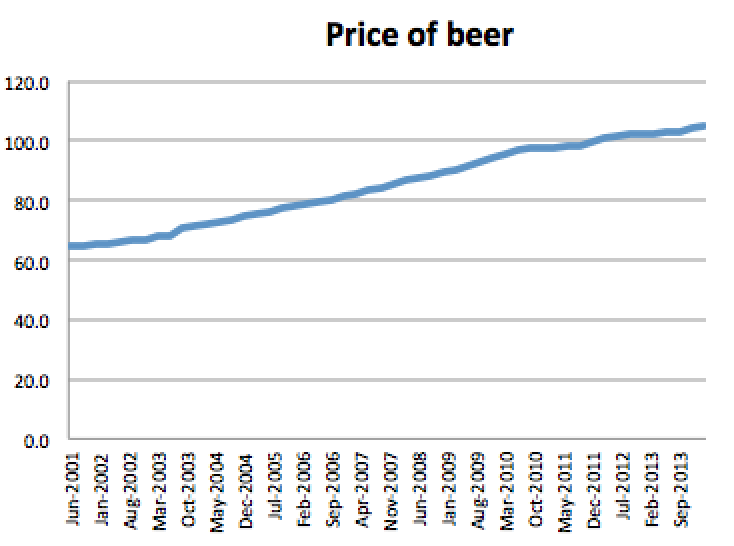

That’s not all. While trying to save, kids are also worried about student debts. The cost of university has also doubled in the last ten years, far exceeding the rate of inflation.

Incidentally, the price of beer has shot up too, and given how much of my student budget went on that, I’m glad I attended university over a decade ago.

For wealthy people from wealthy families, living at home is a simple matter of balancing material comfort against mild embarrassment. Kids who choose to live at home are a grand source of humour and pensive Guardian opinion pieces.

But really, the option is a blessing for those of us whose parents have stable housing situations. Not everybody is so fortunate.

Its share price has doubled in the last twelve months, taking its market value to $25 billion, as its cars are voted Car of the Year, Best Car Ever Tested, etc.

By pricing electric cars in the $100,000 – $200,000 range, Tesla have made them highly desirable. (Performance may also be helping. The Tesla Roadster reaches 100km/h in 3.9 seconds.)

Tesla has an eye for good PR. But this is more than that. It’s an attack on the whole patent system.

“When I started out with my first company, Zip2, I thought patents were a good thing and worked hard to obtain them. And maybe they were good long ago, but too often these days they serve merely to stifle progress, entrench the positions of giant corporations and enrich those in the legal profession, rather than the actual inventors. After Zip2, when I realized that receiving a patent really just meant that you bought a lottery ticket to a lawsuit, I avoided them whenever possible.” – Elon Musk, June 2014.

Musk has tapped into something vital. Patents (like copyright and trademarks) have long since broken their moorings to the island of usefulness and drifted off into an ocean of fantasy, where piratical lawyers rule the waves.

It’s not just inventions that can be patented, but “business processes.”

For example, Amazon patented “one-click shopping.” That means every other online store has to make sure you click twice to buy online, license the “process” or risk a patent lawsuit from the internet commerce giant.

Patents are private property though, so this should be fair enough, right? Wrong. From society’s perspective, possession of patents is very different to possession of something physical.

Owning an idea is a contrivance invented for the sole purpose of encouraging ideas. But ideas work best when they spread. A patent is therefore of most value when it balances encouraging new ideas and spreading existing ideas. Exclusive, indefinite use of a patent is arguably worse than never having a patent at all.

Some industries thrive without patents. Australia’s restaurant industry, for example, is electric with innovation. But you never see a chef hiring a patent attorney to show that a pumpkin and fennel soup on a menu across town is similar enough to warrant the paying of royalties.

A patent for a process for turning warm bean juice into a big deal by the application of hipsters? I may have just made a fortune with this idea.

The Australian government’s current review of competition policy has patent law under the microscope. The issues paper (released April 2014) appears to show willingness to move Australia even further from the clutches of the patent trolls.

“…[P]roviding too much protection for IP can deter competition and limit choice for consumers… Are there restrictions arising from IP laws that have an unduly adverse impact on competition? Can the objectives of these IP laws be achieved in a manner more conducive to competition?”

That could see patents renewable where a new use can be found for an existing product, and copyright protections lasting up to 70 years beyond the life of the author.

“Australians could pay more for drugs and medicines, movies, computer games and software, and be placed under surveillance as part of a US-led crackdown on internet piracy…” according to an article in the Sydney Morning Herald.

In Australia at present, copyright is a bigger issue than patents.

Consider the copyright over the tune “Kookaburra Sits in the Old Gum Tree.” That classic children’s tune was composed in 1932. But when, in 2008, a faint similarity was heard with the Men At Work song Land Down Under (itself released in 1981) the record label that owned copyright to Kookaburra pursued the songwriters. Some months later Men at Work’s Greg Ham – who played the riff deemed to be plagiarised – was dead by his own hand.

The courts required five per cent of royalties from the hit song to be paid to the owner of the copyright, and in 2011, the Federal Court refused to hear an appeal.

(The Song Happy Birthday is also copyrighted. It is owned by Warner/Chappell Music, which collects a reported $2 million a year in royalties.)

I’d be willing to sell off every childhood song we have, from Twinkle Twinkle to the Incy Wincy Spider, if it spurred more innovation in childhood songs. Similarly, I’d be happy for patents to establish a chokehold on the technology industry, if they clearly generated better products for consumers.

And that’s what inspired this surprising move by Tesla. Let’s hope many more follow them.

“Technology leadership is not defined by patents, which history has repeatedly shown to be small protection indeed against a determined competitor, but rather by the ability of a company to attract and motivate the world’s most talented engineers. We believe that applying the open source philosophy to our patents will strengthen rather than diminish Tesla’s position in this regard.” – Elon Musk

In order to answer this question, I’ve surveyed six people who started PhDs – friends of mine – from the following fields: physics, biology, computer science, chemistry, economics and history.

Five emerged from their programs with a Doctorate, one turned theirs into a Masters. (Given the PhD completion rate in Australia is 60-61 per cent, this sample is biased towards survivors.) One works in academia.

Their answers make a very interesting set. But before I let them speak for themselves, a confession: I was accused of asking leading questions. It may be true, but it’s the zeal of the convert.

As an undergrad, surrounded by lecturers with PhDs, I wanted one too. Then I got a job offer at the end of my degree. Starting that job I met plenty of public servants with doctorates. We were doing the same jobs, making the same pay. I came to see my desire for a PhD as the result of sample bias: Most powerful people in universities have PhDs, but most people with PhDs are not powerful people in universities.

With that noted, let’s hear from the experts!

BENEFITS OF A PHD?

Physics at Australian National University: I’m a researcher/lecturer, which I fundamentally couldn’t do without my PhD of course. I haven’t had any other profession since graduating. On a personal level, I really enjoyed it. I learn’t much more than just the topic of my thesis. I really learnt a lot about problem solving, logic, and life from being in close contact with world class researchers. During my PhD, I had the pleasure of interacting with four Nobel laureates at various times.

Biology at Melbourne University:I became a specialist in a very narrow field of study, possibly even an expert in said field. I also gained valuable generalist skills in experimental design, data analysis, working independently and as part of a team, critical thinking and the effective oral and written presentation of data and ideas. A PhD is also an exercise in persistence and perseverance, not necessarily intelligence, so I consider that most people who have completed aPhD are good at troubleshooting and are quite resourceful.

Computer Science, RMIT: I (arguably) got my foot in the door of my first job in industry from my PhD, and some of the domain knowledge I acquired there was useful in my job. My written and verbal presentation skills were also improved during my PhD, and I learned to have a healthy disrespect for authority. I also had a lot of fun! I found my PhD years to be quite relaxed (despite the odd moment of stress) and it was actually quite a nice transition between undergraduate spoonfeeding and the “real world” of the workplace.

Chemistry Masters, ANU: Benefit is a fancier CV. Without a masters I wouldn’t have gotten either my first or second job in consulting. In terms of education I am far more adept at seeing the ulterior motives and ugly manipulative side of people after working for my pitiable (but totally hatable) supervisor.

Economics, Oxford: Time to read and develop deeper / broader domain knowledge. For me, that was Chinese language, China’s economy and history, econometric techniques. Got supervision re: use of econometric analysis and thinking through data, and technical skills. I also played a lot of squash and improved my cooking. Those are the main benefits!

History, Melbourne University: For me, the three years doing it was probably the biggest benefit. I had a scholarship which is a privileged position to be in because it enables you to study something that fascinates you without having to work full time. I had a clear idea of what I needed to achieve each day, and if I got it done more quickly I gave myself the rest of the day off. More recently there have been career benefits I think, but like many people when I finished the thesis I wanted to do something totally different from research.

Graduation day.

DOWNSIDES?

Physics at ANU: More than once I felt like quitting. In hindsight, the pay is tiny compared to what you could be earning, but I didn’t really think about that at the time. You have no guarantee that you will finish. There are people who try as hard as they can for over 4 years and come away with nothing.

Biology at Melbourne University: The downside is that you are very cheap labour at the bottom of a pyramid scheme. You know that chapter in Freakonomics where drug dealing is compared to a pyramid scheme? Well, I’d change the “drug dealing” to “research” and “academia” and the chapter would still be quite accurate (minus the crack cocaine and guns). Everyone’s ego is complimented when they are asked to do a PhD. What hindsight has taught me is that there is very little money in Australian research and really not enough for most senior researchers (lecturers etc) to hire employees (such as postdocs or research assistants) so there is a huge reliance on the cheap PhD labour that the federal government (or uni) pays for.

Computer Science, RMIT: I didn’t earn that much money (although I found my stipend to be perfectly adequate) and, obviously, my entry to the workforce was delayed by a few years. In terms of climbing the career ladder it was probably not great bang for buck, but I don’t care too much about that sort of thing so don’t consider that a downside.

Chemistry Masters, ANU: Downside was three years of near-suicide misery and lost opportunity. I could have done a law or engineering degree in that time. I still feel that sense of loss – I am always years older than my peers.

Economics, Oxford: Long distance relationship. I’m not sure Oxford was the best place for me. 3-4 years out of workforce and foregone income and job experience.

History, Melbourne University: Honestly, the main downside was the public speaking obligations and pressure to publish along the way.

The academic job market is tight

WHO SHOULD START A DOCTORATE?

Physics at ANU: I believe that you shouldn’t do a PhD because you want a piece of paper that says “I have a PhD“. The people who I know who were trying to prove something, either to themselves or to others, always had a terrible time. If you have had a taste of research, and still feel like more, then you should consider a PhD. There’s also the question of talent. There are people who love science, yet just aren’t cut out for research. Fundamentally, if you’re not driven by curiosity, and have a hunger for discovery, specifically towards your project, you probably shouldn’t be there.

Biology at Melbourne University:I actively discourage most people from starting a PhD. For most professions, the experience you gain in the workplace will be better. For anyone wanting to do scientific research, then permanent positions in Unis or CSIRO are few and far between (see pyramid scheme comments above). With this in mind, I know plenty of people who I did my science PhD with who now work outside of academia, in the public service, as patent attorneys, as technical sales reps, and in private biotech/pharma firms and consulting. Someone contemplating a science PhD should realise that these non-academic jobs are actually where they are most likely to end up and then determine whether a PhD is really still necessary. And realise that their PhD supervisor is always going to encourage the singular academic trajectory (ie they are much happier to be a reference for further academic appointments than anything else).

Computer Science, RMIT: To consider doing a PhD you will need to be convinced you have the necessary skills and temperament to undertake a prolonged exercise in independent research, and at least one of the following should be true:

-You think you will enjoy doing a PhD for its own sake;

-Your chosen profession requires a PhD (e.g. academia);

-You will acquire **specific** skills that will help your career in your chosen profession.

These are bad reasons to do a PhD:

-You’re not sure what else to do after you finish your undergrad;

-You think it would be cool to get to call yourself “doctor”;

-You expect some ill-specified career advantage from having one;

-Your parents would be proud;

-It’s “prestigious”.

Chemistry Masters, ANU: The only people who should do PhDs are either saintly types who just love their subject and have no expectation of any type of employment related advantage or psychopathic sadists who will enjoy destroying promising young people.

Economics, Oxford: Almost definitely do one: if you want to become an academic; its paid for; have world leading supervisor who has top track record of placing their students into great academic jobs; at world class research institution, great city, great classmates etc.

Never ever do one: in the opposite scenario: Unsure if academia is the path; not at top ranking place and doing a major where job placements are super tough; where PhDs take 6-7 years; or living in a shit city.

History, Melbourne University: The peers I had that struggled the most were those who set themselves additional challenges such as designing research involving lengthy ethics processes and multiple methods, including undertaking lots of complex interviews and all the responsibilities that come with that. This type of research makes a huge contribution to the evidence base but goes well beyond the three years you sign up for and requires a significant time investment in project management.

There’s more than one way to prove you are a big shot.

WHAT PROPORTION OF SMART UNDERGRADUATES SHOULD SERIOUSLY CONSIDER IT?

Physics at ANU: Only those who tick the boxes in the above question. How many PhD grads do we need? Well, that’s a different story. In the Australian employment market, a PhD isn’t really valued. From an employment point of view, the only reason to do a phd is if you want to become a researcher. The number of permanent research positions that open up every year, divided by the number of phd graduates is bugger all squared.

Biology at Melbourne University: A large proportion of smart undergrads will contemplate it, and even be asked by lecturers to do a PhD. As above, I would suggest that only a very few should take it up. There are too many easily available PhD scholarships in this country and not enough investment in other parts of the research infrastructure, hence the pyramid scheme. If they are smart, they can get the benefits I mentioned above from plenty of other roles.

Chemistry Masters, ANU: Maybe 5 per cent of undergraduates? We need to rethink PhD candidature. There are things to be learnt, but should acknowledge that phd students teach each other and are self taught in what can be an educationally nutritious environment – it all depends on the calibre of your fellow students. With ten students to a professor this will always be the way. The idea of charging tuition for a PhD is outrageous. My only hope is this will decimate the ranks of the fools who sign up for one.

I see PhD years as a type of national service, where you accept below minimum wage for contributing to the R&D pie for the nation. We should acknowledge this and stop pretending it is training for an academic or other research career – those jobs don’t exist. Also we should acknowledge that growing the R&D pie is of national importance. Slave student labour will be cheapest.

Also I would like to see universities sued for misleading students regarding their employment prospects. Or scolded for false advertising. A PhD contract (because you sign a contract) should include a disclaimer with real graduate outcome figures. And then you should have a counselling session to determine if you’re likely to kill yourself.

Economics, Oxford: I’m not going to tell anyone they shouldn’t do it if they’re interested. I just think they should be fully aware of the academic labor market conditions and that it is in supervisor’s interests NOT to be fully candid / upfront about this. By this, I mean how tough the market is, especially in humanities, etc.

History, Melbourne University: Lots. It’s important to have a great topic and a good supervisor and that you like to work alone a lot. I worked part time doing something completely different which was a good balance for me.

—

I feel like we got a great range of answers there, with evangelism from both sides and plenty of middle ground. No matter your pre-existing biases, there is something to grasp onto!

The 2014 Budget is the most significant in a long time. I have an eager – some would say obsessive – interest in federal budgets, and I cannot remember a Budget that has got as much attention as this one.

Today marks four weeks since the second Tuesday in May, and Budget headlines are still around. For example:

I went through the internet archive. It shows the 2014 Budget produced not only a much bigger spike in interest in the Budget, but a much longer tail. It is not common for budgets to be sparking discussion three weeks after they are released – people normally move on fast and a government only dreams about getting three weeks of “traction”.

The graph above compiles mentions of the word Budget on the homepages of The Age and The Australian in the month around the Budget. I did an analysis for 2008 too, because the first Budget of the Rudd government would be a good comparison to the first Budget under Abbott. The data is a lot more spotty, but the pattern is the same. In 2008, Budget headlines died out after no more than a week.

Google trends data confirms that this Budget was a whopper as far as public interest goes. The graph below shows share of searches from within Australia. (Google omits the vertical axis – I guess that’s proprietary data).

Imagine putting your money in the bank, and getting a negative interest rate. You’d want to get it out again as soon as possible, right? That’s the point.

If the interest rate is negative, the central bank is goading you into using your money, not just sitting on it. That should mean more spending. More spending makes more jobs. And like this they hope to get Europe out of the quicksand of high unemployment.

So, if this works, how come it’s never been tried before?

The thing is, interest rates don’t just work on their own. You’ve got to consider inflation. If you get 2 per cent interest on your deposit but inflation is 3 per cent, then really you are losing the purchasing power of your money. (in the business this is called “negative real interest rates” where the word “real” means inflation is taken into account).

You can make “negative real interest rates” by setting the interest rate below inflation. That’s easy. The problem in Europe is there’s so little activity that inflation is very, very low. They have to make the advertised interest rate negative to get the “real” interest rate negative.

Now, it’s worth noting that the negative interest rates don’t apply to the average punter. They are for the deposits that banks have with the central bank. (Millions and billions of euros every night).

The reason for that is simple. If you or I see that the $11.50 we have in the bank is attracting a negative interest rate (here I am ignoring the “real” interest rate), there’s a simple trick we can use – take it out of the bank and turn it into cash. Cash gets an interest rate of zero, so that’s a lot better than leaving your money in the bank.

If you only have your money in electronic form, there’s no way to avoid keeping it in a bank account. You can’t put 1s and 0s in a shoebox under your bed.

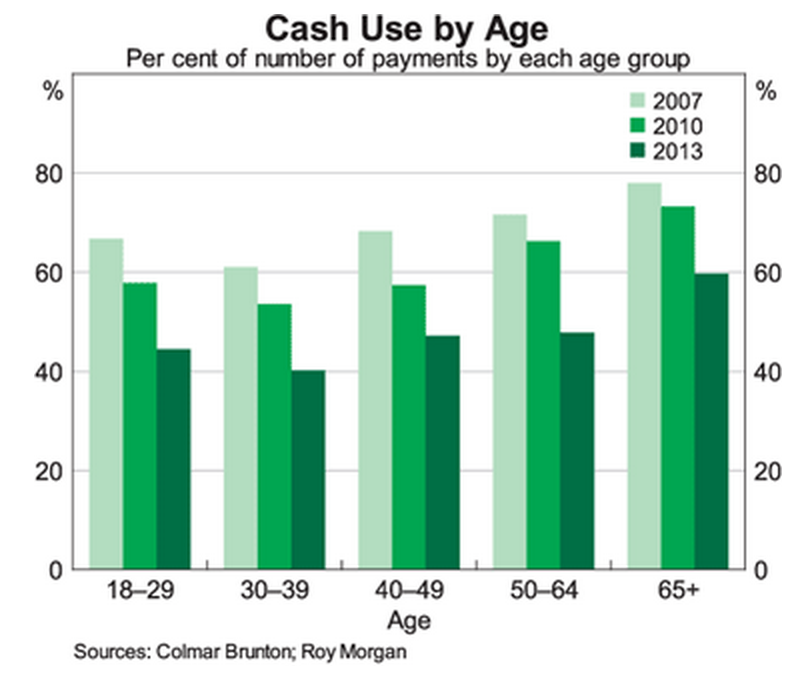

Negative interest rates would not necessarily cause a riot. Bank fees already work in such a way that we’re used to seeing our bank balances retreat when left alone. A cash free future is plausible. People are using cash less and less.

Cash use falls sharply in all age groups. (Source: RBA)

While the rise of Paypass could end up stranding us in a future where we actually pay banks to hang onto our money instead of the other way around, there are other innovations that make a cashless society with negative interest rates unlikely.

I am talking about Bitcoin. The rise of a kind of cash that is beyond the control of central banks means attempts to control rates on government-issued cash are more futile than in the past.

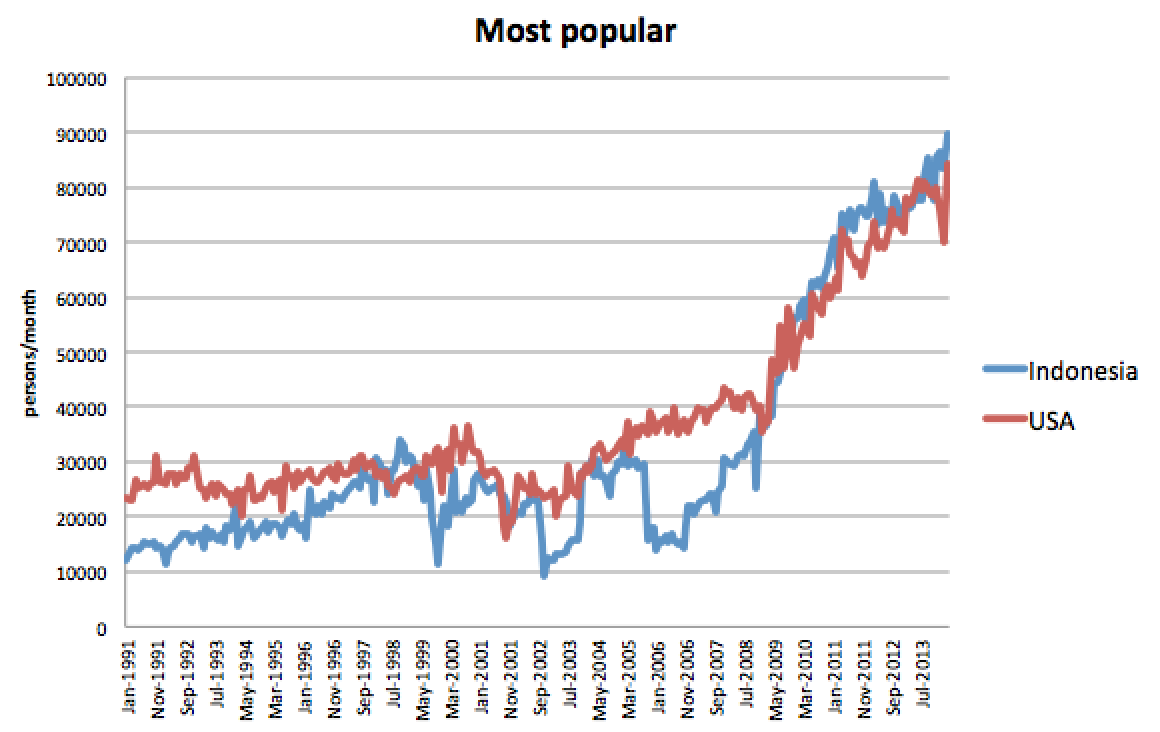

“Alabama-born, Dallas-raised Jeremy Sutphin, chef at Le Bon Ton, attributes it to adventure and awareness. ”I’ve been here eight years and the palates are searching for something different – and people are becoming more aware.” “

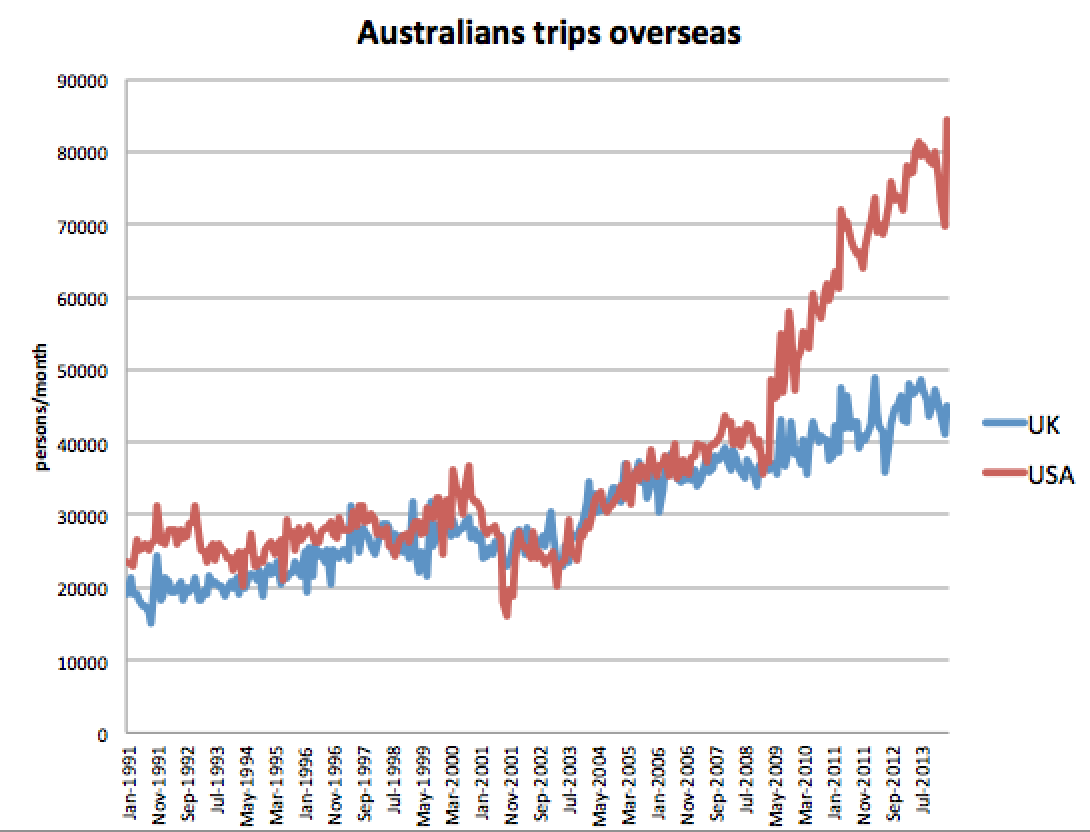

He’s right about that awareness. Australia’s knowledge of America is now a lot deeper and wider – we’ve now been to America enough that we’ve ventured beyond LA and New York.

“This agreement will be good for competition and it could … lower airfares.”

We’ll forgive him for not predicting the great barbecue explosion of 2012/13/14.

Of course, post-2009 also coincides with a much higher Aussie dollar. There were three good years there where you could buy a greenback for less than one Aussie dollar. Of course, those days are behind us.

So if travel predicts what we’ll be eating next, what’s the next big wave?

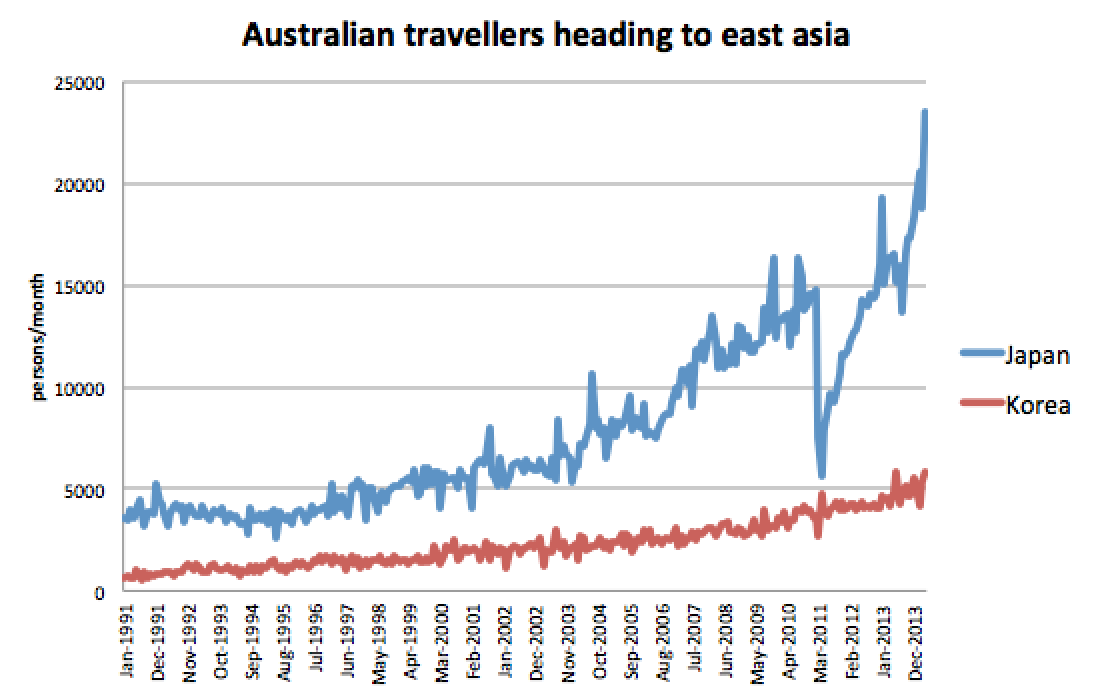

Might a renaissance of Japanese cuisine be on the cards? Perhaps. But Japan’s post-Fukushima bounce back still looks modest compared to other places Australians love to fly.

There is one extremely popular destination still terribly under-represented at the fancy end of the food business.

Indonesia’s surge is even bigger than America’s. Looks like queueing up to pay $40 for a plate of nasi goreng cannot be far away.

Talking about narrative goes deep into policy making circles:

“Narratives are stories, in whatever form they take – oral, written or visual. Conventional narratives in literature, the theatre or the cinema have a beginning, middle and end. Good ones provide drama, arising from a predicament that ensnares the principal character; they have plenty of action – the steps the character takes to escape the predicament – with unexpected plot twists and complications thrown in; and there is a resolution, culminating in the achievement of a visionary aspiration or objective. Economic narratives have some similarities.”

All this talk about narrative in politics has coincided with what many people agree is a golden age of story-telling in the ascendant medium of television (1, 2, 3, 4)

But I see no sign of politicians learning from it.

Our leaders scarcely ever admit to watching the box. They prefer to project an image of someone working tirelessly for their constituents. Why have they spurned the chance to learn from TV?

Politicians fetishise staying on message. That – they believe – is the only way to get voters to hear the one thing you want them to hear. It is true only if you assume that people won’t be listening, and it is a catch-22.

Would you tune into a show where the main character just repeated the same lines, week-in and week-out?

What about a show where they never admitted they were wrong? Never grew as a person? Never got into trouble and squeaked back out?

Our political characters all claim to be good people from ordinary backgrounds, and play down their weirdness. It’s immensely boring.

They end up with a script that’s all issues, no characters. But (most) humans don’t care about issues in the abstract. We are drawn to characters.

In the HBO western Deadwood, the opening credits are all about a tough but fair sherriff called Bullock. But after a few episodes Bullock’s role fades and the writers turn saloon-owner Swearengen into the main focus.

He’s a murderer, bully and brothel owner. But his motivations and relationships are complex. They make us love him in the end, and we forgive far more from him than we would from the rest.

Viewers don’t mind complexity. We can even feel for Sergeant Brody, the muslim terrorist at the centre of Homeland, because we get insight into his home life and terrible back-story.

We barrack for Walter White from Breaking Bad, who is a meth cook. We barrack for Omar in The Wire and the inmates in Orange is the New Black. All because we get to know them. We see not only their strengths but their weaknesses. We see them as humans, not message delivery machines.

Can politicians learn from this?

I’m not saying the front benches should start dealing drugs. Just that it doesn’t hurt to show a little of their real struggles. There should be plenty there. Difficult lives turn people to politics and politics is hard on humans.

A political career is a story written over the really long-term. It is not a movie. If it is to remain compelling, the main characters have to have depth. Depth means complexity and complexity requires ambiguity.

At the moment, political narratives strive to kill ambiguity. But this generates only the most superficial interaction with issues.

We might actually be a chance of engaging with university reform if we saw how Joe Hockey’s mother-in-law hates him for it, if we knew it kept him up at night, if we saw how his background and values explain why he balanced it off against other priorities.

As presented, there’s no meat to the political narratives. They are the kind of narrative you might get in a child’s story book. See Spot Run appears to have inspired See Joe Repair Budget.

There is little to grasp on to in the Coalition’s story. Nothing to stop us from painting them as simple villains. Nothing to stop us rolling our eyes and changing the channel. Nothing to make us focus in the short run, empathise in the medium run and barrack in the long run.

Bill Shorten could learn a lot from Batman. We know more about how Batman begins than Bill begins. Why is that?

But it doesn’t just have to be about the leaders. The Avengers or Oceans Eleven may be an even better metaphor for a political party. A raggedy team with distinct flaws and skills have to fit together to get a job done. There’s alliances and fractures that keep us focused on them, and those alliances and fractures are strengths, not weaknesses, in the narrative. Political parties try to keep talk of factions down. But they can be a fascinating sub-plot.

There are some politicians that modern messaging experts can’t explain. They include Bob Katter, Clive Palmer, and Lee Rhiannon. These people understand something of how eye-catching, complex characters can take an outsize role in a narrative. But does the political world learn from them?

Politics is much like it was 20 years ago and the time is right for a change in the way it is practised. It is a cozy old duopoly using old school communications techniques that are increasingly out of favour with the youth. In TV terms, the major parties are the Simpsons and the Bold and the Beautiful. Popular once, they are now the same old thing over and over.

Who is authoring The Sopranos of politics, writing a script that looses the foundations and doesn’t care who it shocks?

Is it Clive Palmer? Or is he just some sort of free-form experiment, like a drama student let loose with a digital camera.

When will we get a real narrative made up of characters real Australians actually care about? I cannot wait for such a show to hit the air.

Imagine you’re doing some internet shopping. You want some shoes to replace a favourite pair that is worn out. You type in the name of the place where you got the last pair, and click the first link that comes up. You choose the exact same pair, sling the credit card, and start waiting for the postman.

The shoe retailer sees this: someone searched for their name, clicked the link they paid Google to install, and then went on to make a purchase. They add that to their return on investment for buying ads associated with their own company name.

“search advertising only works if the consumer has no idea that the company has the desired product”

This also applies for ads with both the retailer name and a product in it. Like “Myer suits” or “Kogan TV”.

The effect of suspending paid search for branded terms like ebay shoes

The research is not some wishy-washy lab experiment. It was done by eBay Research, and involved a giant control experiment. eBay started by cancelling all the paid search advertisements for terms like “ebay shoes” in 30 per cent of America.

It then widened the experiment to non-branded searches, like “shoes”

What it found was startling: “on average, U.S. consumers do not shop more on eBay when they are exposed to paid search ads.“

The reason is this. Search engine marketing causes a big leap in traffic from people that have never used eBay before. But a vast majority of people that use eBay are experienced users. because the search engine can’t target the newbies, the return on investment ends up being very poor.

“consumers who have completed at least three eBay transactions in the year before our experiment are likely to be familiar with eBay’s offerings and value proposition, and are unaffected by the presence of paid search advertising”

effect of paid ads is very low among frequent users

So search engine marketing is still good for people who don’t regularly use your site. But here’s the rub. Among people who shop on eBay all the time (50+ purchases a year), they use paid links 4 per cent of the time. eBay pays for all those clicks and an unsophisticated measure of the effectiveness of paid advertising would therefore show that paid links are effective.

Turning off ads left eBay with 99.5 per cent of its normal sales. The differences between the period with ads and the period without are far from striking:

Obviously small companies can still get bang for their buck advertising online. But big companies perhaps less so, and that might hurt Google.

“Of the $31.7 billion that was spent in the U.S. in 2011 on internet advertising, estimates project that the top 10 spenders in this channel account for about $2.36 billion.”

The study can’t reveal eBay’s actual expenditure on Google paid search, but it uses an estimate of $51 million a year, based on google’s public statements. That delivers a return on investment of -63 per cent.

Forget the millions spent on building a brand that was recognised immediately across the state.

Forget the strategies that have made Victoria the clear leader among the states on cutting injuries and fatalities for years. (source)

Worksafe was a brilliant invention. By combining the regulator of workplace safety with the insurer, the economic incentives are all aligned. The company wants to reduce injuries, keep its customers happy and get the ill and injured back to work.

It’s a revolutionary piece of policy-making (mirrored in the design of the Transport Accident Commission, which has helped bring automobile accidents down to their lowest level in history, and among the best in the world.)

A huge part of the job of Worksafe is raising awareness of dangers in workplaces.

This is why Worksafe spent big bucks using proper advertising agencies and sponsors the Western Bulldogs. We are all familiar with its very successful advertising campaigns.

Awareness is enormously important in promoting safety and Worksafe has always used free publicity too. Whenever a prosecution or fatality happened, Worksafe would put out a press release, and papers would report on it.

Worksafe could not prosecute every little business with a safety breach. Amplifying successful prosecutions creates the impression firms face legal risks if they do not focus on safety. Worksafe would also issue a press release whenever a worker was killed or seriously injured at work. This served to keep workplace safety in the news.

But then.

In late 2013, the Hon Gordon Rich-Phillips, minister in charge of Worksafe, must have spotted one of these stories in the newspaper. Was Worksafe “anti-business”? Things changed.

The honourable member is an amateur aviation enthusiast.

Since then, Worksafe’s media strategy has transformed.

Worksafe issued 41 press releases in the first part of 2013. They did not stint on death and blood and gore, or big whopping fines.

But 2014 is extremely sanitised.

A change of tune

And it’s not as if there was nothing newsworthy. For example, at a factory owned by the company that makes Kettle chips and CCs, a man was dragged into a conveyor belt and lost his arm above the the elbow. That resulted in a $45,000 fine in February.

The organisation that was a world-leading innovator in public policy is no longer free to run in the best interests of workers and its own insurance scheme. It now dances to the tune of the government.

Now new ads have hit the papers with the name Worksafe nowhere to be seen.

“The important work that we do across Victoria is much broader than just safety, so using our legal name – VWA – better reflects all areas of our business” – the press release.

Changing your brand when you’ve spent so much on it will make your organisation less effective.

People are already confused about the difference between the Victorian Workcover Authority and Worksafe. (They are the same. The former is the legal name of the organisation. The latter was an effective brand designed to reinforce the idea the organisation should be more dynamic and less bureaucratic .)

Emasculating this powerful and effective brand will mean more injuries. Workers will suffer, and so will business owners who do the right thing and keep their workplaces safe. They will have to pay higher premiums to cover compensation for the injured and dead.

Worksafe’s creative communications: Spare parts vending machine. [source]That a good strategy and a powerful brand can be eliminated on a whim of a minister speaks of an anti-intellectual approach in the Coalition party-room. The state government ought to be ashamed.

Forget the millions spent on building a brand that was recognised immediately across the state.

Forget the millions spent on building a brand that was recognised immediately across the state.

{kind=link}