“Unbalanced” and “out of proportion” are the words they use in a brand new report out today.

“Recent housing price growth seems to have encouraged further investor activity. As a result, the composition of housing and mortgage markets is becoming unbalanced, with new lending to investors being out of proportion to rental housing’s share of the housing stock. “

Do not get the impression the RBA thinks this will be a minor:

“In the first instance, the risks associated with this lending behaviour are likely to be macroeconomic in nature rather than direct risks to the stability of financial institutions.”

nb. “In the first instance…”

Who knows what sort of calamity could follow a macroeconomic event associated with a big house price fall? And if you think not owning a house makes you safe then you are wrong.

“…a broader risk remains that additional speculative demand can amplify the property price cycle and increase the potential for prices to fall later, with associated effects on household wealth and spending. These dynamics can affect households more widely than just those that are currently taking out loans: the households most affected by the declines in wealth need not necessarily be those that contributed to heightened activity”

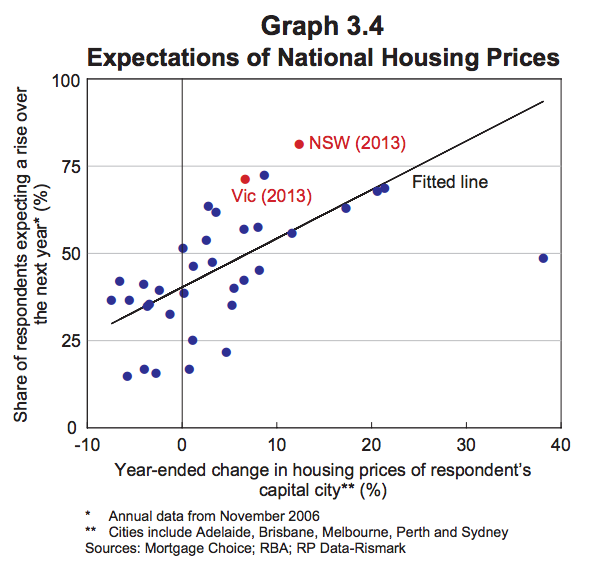

This chart got the RBA concerned:

“… expectations of future housing prices seem to be influenced by the recent past (Graph 3.4). This tendency was stronger than average in New South Wales and Victoria at the end of last year. The risks associated with this behaviour are likely to be macroeconomic in nature if households were to react to declines in their wealth and any repayment difficulties by cutting back their spending. “

The recent rise in interest-only loans (yellow line below) also has the RBA worried about whether speculation is rife.

They are so worried about house prices they are cracking open the weapons safe and rustling around for some ammo to try to scare off packs of hungry investors.

“The Bank is discussing with APRA, and other members of the Council of Financial Regulators, additional steps that might be taken to reinforce sound lending practices, particularly for lending to investors. “

The most likely step is not to mimic NZ and try to control Loan-to-Value ratios (as you can see in the above graph, LVRs seem to be under control). It is to make banks add a bigger buffer to their lending criteria. Currently they add 2 per cent to the existing interest rate. That might rise.

The last warning the RBA delivers may be important for anyone considering buying a small apartment in central Melbourne:

“A speculative upswing in demand can also be damaging if it brings forth an increase in construction on a scale that leads to a future overhang of supply. This risk is more likely to arise in particular local markets than at the national level.”

CAVEAT: The RBA points out that housing market dynamics are most skewed in Melbourne and Sydney. I’ve noted myself that buying in Brisbane looks like a pretty clever move.

FULL DISCLOSURE: The author is not invested in property.