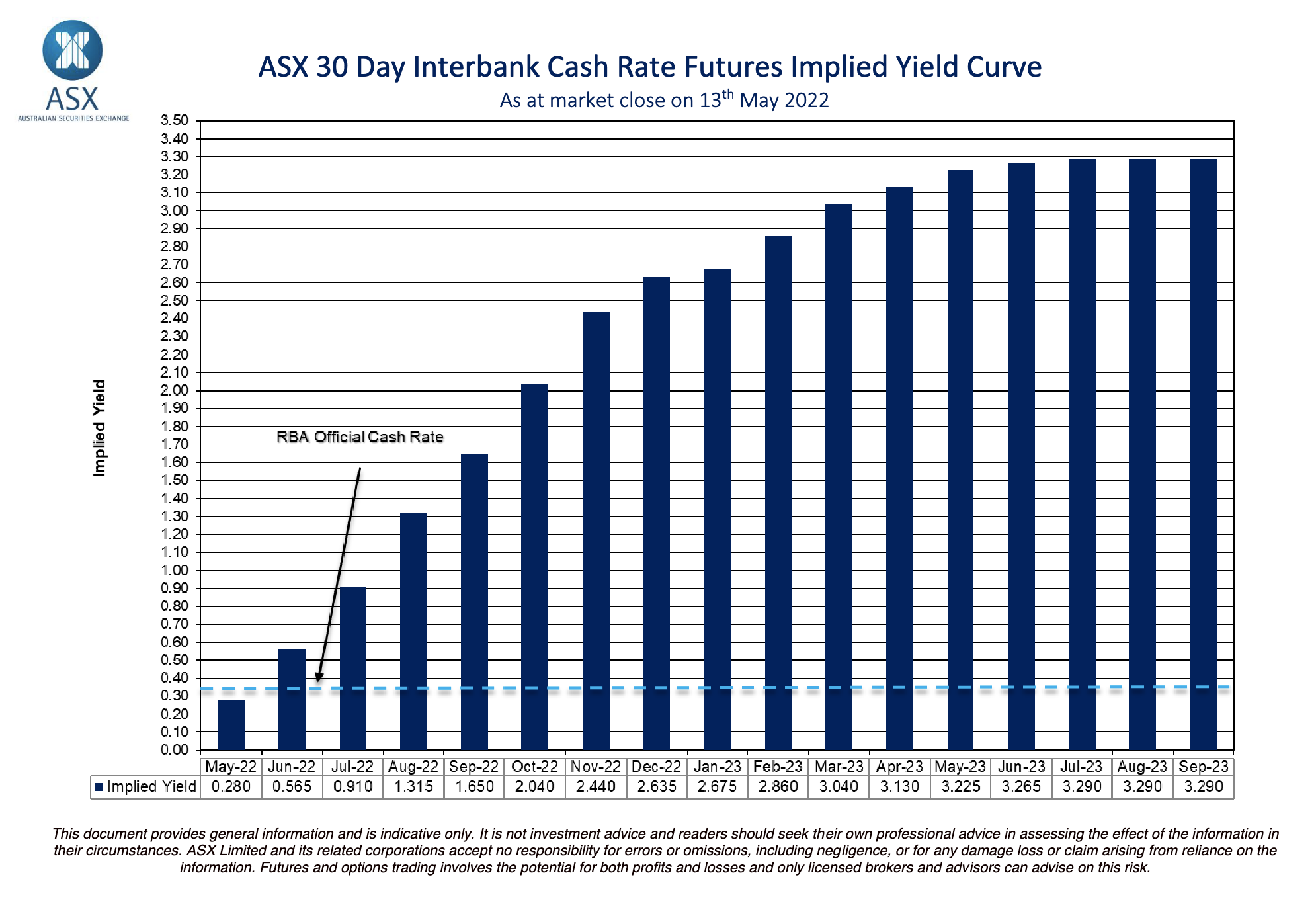

Everyone’s excited about this chart. It shows official interest rates racing up to over 2.5 per cent by the end of the year. That would be one of the fastest interest rate rise cycles in history and would make a lot of people with mortgages rather unhappy.

The chart is not one person’s prediction. Instead it uses the wisdom of crowds: the values are derived from market prices in the Interbank Cash Rate Futures market. This market has a very good recent history of prediction. Back in 2021, It was insisting rate rises were coming in 2022 when the RBA was insisting the opposite and reassuring us they wouldn’t arrive until 2023-2024. But how accurate are these predictions more generally? Where do they come from? What assumptions do they make? I did some digging.

First I contacted the ASX, who publish the above chart each afternoon. I asked them: Who trades this market? The market for Interbank Cash Rate Futures, they told me, is on the ASX24 platform, which is traded around the clock by a small number of big name brokers and investment banks – Goldman Sachs, and their ilk – who have to register. The registered users provide access to their clients, being super funds, hedge funds, etc.

Plenty of people told me they thought rates would never get as high as the predictions above and would like to bet against them by trading in this market. Inquiring minds wanted to know: Can retail traders get involved in the market for Interbank cash rate futures? The answer is there could well be retail traders – the identity of who is trading through the big brokers and banks is anonymous. Minimum contract size for interbank futures is $3 million, but on closer inspection that seems to be the face value of the arbitrary contract – when trading it you’re only up for the interest on a contract of that size: A few thousand dollars. So it seems anyone can play if they have a broker.

The ASX also told me you can see prices here with a 20 minute delay.

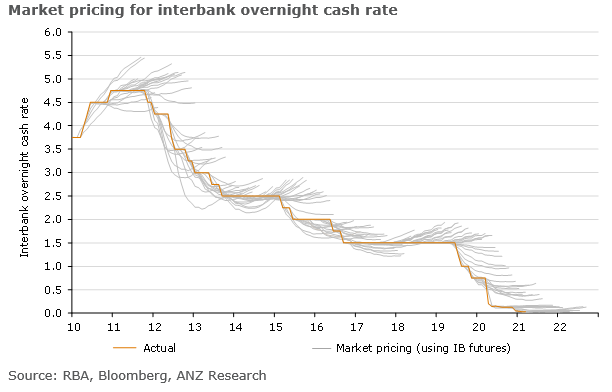

The big question: Does this market really give us the best guess of the cash rate? This chart, from ANZ, seems to show the interbank futures generating a systemic overestimate of the eventual cash rate. There is much more grey line above the orange line than below, especially for the predictions made about later months in each forecast (each grey line is 17 or 18 months long and they almost all seem to bend back up). Is that for some technical reason? Or just because in the 12-year period depicted nobody could quite believe interest rates would not turn around and “normalise”?

Obviously predictions of the later future are more affected by random error. But even when the grey lines slope down at the start, they slope up at the end. Hmm. I found a 2012 RBA paper by Olivan and Finlay – Extracting Information from Financial Market Instruments – that made me worry later months are biased upwards:

“… the forward curve gives the interest rate agreed today for overnight borrowing at a date in the future. The forward curve can be used as an indicator of the path of expected future cash rates, but importantly it becomes less reliable as the tenor lengthens because of the existence of various risk premia, for example term premia. No attempt is made in this article to adjust for these risk premia and so they will affect the estimated zero-coupon curves.”

The RBA and I corresponded and Finlay confirmed there’s probably upward bias in the interbank futures market, but how much, you could never say.

…on average you would expect term premia to be positive (and so bias up the market rate relative to expectations) and to get bigger as the time horizon lengthens. BUT as said it is hard to be absolutely sure – term premia are unobservable and can in theory also be negative.

You can estimate models to separate term premia from expectations, but you need to make a lot of (possibly implausible) assumptions, so again need to take results with some caution.

Other futures traders assured me that over 18 months term premium is not worth worrying about. Does a possible bias in the later months matter a lot right now? No. If you glance back up at the first chart in this post, you will see that the steep part of the curve is in the next 7 months, not the following 11 months. It means this: the signal the market is sending could be wrong, but ignore it at your peril.

I did more digging around in the Interbank Cash Rate futures market, and found something probably more concerning than term premium: the later months are not traded very much at all. But their price appears to update even on days when none changed hands. Quite how this works is not clear to me yet.

There’s another problem with it too: Data on the Interbank cash rate futures market is hard to find. There is no publicly available repository of historical data that I know of (ANZ obviously has it, to make that chart above, but they are not sharing!) The ASX publishes a .pdf of one day’s data every day but when the pdf updates the previous day’s data is lost forever. They also go to the trouble of making it a low-resolution image so it’s hard to collect. Ctrl+c, Ctrl+v is out of the question. You’re either transcribing it manually or using optical character recognition. Thanks, guys.

WHAT ELSE IS THERE?

Interbank futures are not the only kind of futures product you can use to predict the future of interest rates. Another is called overnight indexed swaps (OIS) (aka overnight index swaps, both terms seem to be in use.) These are a bigger and more liquid market. They can trade differently to the interbank futures, directly between parties, rather than on an exchange. That would mean we don’t have data on them. However ever since the 2008 global financial crisis, governments like to keep an eye on derivatives like OIS, so (at least some of) the trades clear through a clearing house which collects data and provides it to government.

Historical OIS data is free from the RBA so long as you want to look only 6 months in the future. (But longer data must be out there somewhere- the big London clearing house LCH will clear Australian OIS with maturities of up to 31 years!) The following chart shows two different OIS prices, which contain information on predictions of the official cash rate in one and six months time. The data shows an expectation for six months in the future (i.e November) of rates at 1.42%. That’s gone dramatically higher in the last month or two as expected, but it is also a dramatically lower prediction than the Interbank Futures market’s prediction of 2.77 per cent! Why? This confused me for a while

The reason it is lower than the other chart turns out to be that the OIS pricing is an average of the cash rate over the future period, rather than the value of the cash rate at the end of the period. You can, however, do some maths on the value and derive the value at the end of the period, called the “forward” rate. The RBA helpfully provides this in table F17. You can see the OIS forwards compared to the Interbank futures in the next chart. They’re similar but not identical!

OIS forwards are the market pricing the RBA “typically” uses as an input to their forecasts. Does their use of it suggest the OIS forwards might be more reliable? Have we finally found the one optimal prediction we should rely on? Here’s an interesting wrinkle: The RBA governor recently said they now blend this series with economists predictions.

I can confirm that we’ve used the same assumption as last time, an average of the market path and the economists’ path. And just to be specific about that, we’re assuming in preparing these forecasts that the interest rate by the end of the year is between 1½ and 1¾ per cent. And then by the end of next year at 2½ per cent. So that’s a technical forecasting assumption.

That is new!

The RBA started averaging market data with economist predictions only recently. That approach has been used in the last two Statements on Monetary Policy. They previously used pure market pricing in their forecasts. Why the change?

My first instinct is the change came because the path of interest rates predicted by the market is now terrifyingly steep and when they feed that into the models we are a good chance of going into recession. Is that possible? The next chart shows the OIS-derived forecasts published by the RBA in May 2022. It tells us, yep, the RBA’s assumptions (e.g 2.5% at end-2023) are now well below the market predictions (3.5% at end-2023).

So most likely they were forced to abandon market pricing as an input to their forecasts because it made the forecasts look terrible!

Should we be worried about the sudden desire to dilute strong market forecasts with watery economist forecasts? Maybe. The economists are likely using similar methods to the RBA – and many bank economists are ex-RBA analysts – so the amount of truly independent information feeding into the RBA’s forecast is now much lower. Two downsides for transparency in all this:

- These economist predictions are not easily available. I believe they are available on the Bloomberg terminal – I remember seeing them when I used to have access to that. However it costs US$24,000 per year to subscribe (this is why Michael Bloomberg is a multi-billionaire.)

- The RBA hasn’t explained why they suddenly changed methodology (or at least I have not seen an explanation) opening up space for the type of speculation seen above.

Here’s an important question: Are the OIS forecasts usually an overestimate? Could that that justify the RBA’s choice? It’s a hard question, as the next chart shows. Mostly they overshoot, sometimes they undershoot, it is possible they have a bias to predicting a return to the status quo.

If we zoom in on the last hike cycle though we see that some of the predictions made at the start of that hiking cycle (the palest blue ones) were pretty accurate, at least for the first 12 months or so. Given this, maybe skepticism of the RBA’s changed approach is warranted? Maybe rates are going to shoot up more than they think?

Of course the RBA is not at the mercy of the futures market. Official rates don’t move by themselves: the RBA makes the decisions to lift them. The central bank’s choice to not use pure market pricing in its forecasts tells us it doesn’t expect to follow that path. So what we might infer from the steepness of the cash rate futures curve and the RBA’s desire to tread a less steep path?

Perhaps that the market is wrong about what it will take to control inflation? That would be good news. Or perhaps that the RBA realises it will have to let inflation run high for quite a while to avoid recession? That would be very bad news indeed. It’s worth watching these forecasts very closely, keeping an eye on inflation both here and overseas, and watching the RBA to see which way this tension resolves.

There’s one remaining mystery in all this: Why the difference in price between the two markets for cash rate futures, Interbank and OIS? And is the difference big enough for a clever blog reader to make money by aribtraging it? Let me know!