This post is not altogether different to my last one, on how we might be overestimating the capabilities of robots. The theme is the same. We are putting a frightening excess of faith in the future of technology.

We sit at an inflection point, extrapolating it to the stars.

Technological progress seems suddenly overwhelming. But there is reason to expect a breakdown in the recent rate of growth, reason to expect that we’ve grown deluded about the prospects of the silicon-based slice of progress we like to label “technology.”

I wrote about this the other day in my regular column over at News.

Suddenly people are taking seriously all the following ideas:

• Driverless cars taking over our cities within just a few years;

• Robots putting practically everybody out of work;

• Artificial intelligence becoming so powerful it destroys us;

• Cryogenics letting us come back from the dead;

• Crypto-currencies taking over from money.

This is not just about people speculating on the future of a few companies. This is about believing the life of humans is about to change faster than ever before in human history. It is like a belief that we’re living through the agricultural revolution, the Renaissance and the Industrial revolution all at once — and all in fast forward.

Why so credulous?

Why do we suddenly believe technology will remake the future so utterly and swiftly? Partly because of a cognitive bias called the recency bias. We remember the recent past much better than the time before it. And in the recent past, technology has wreaked havoc on modern life. You’re reading this on a website that didn’t exist before 20 years ago.

In the past 20 years, the world has changed a lot. And technology has been a big part of it. But that doesn’t mean technology can change everything. The personal computing technology we all interact with daily has made it very obvious to us that technology can change very fast.

But this is a classic case of selection bias. If we try to measure the pace of technology by looking at the things that are changing very fast, we will get the wrong picture. We need to look elsewhere too.

If you tried to measure the pace of technology by looking at commercial aviation, say, what you’d discover is a lack of obvious progress. We used to have supersonic commercial aviation, but nowadays most of us fly around in Airbus A320s (a plane launched in the 1980s) and Boeing 737s (a plane first launched in the 1960s).

You can get a similarly glum feeling if you look at progress in fighting Alzheimers disease or Multiple Sclerosis. There hasn’t been any, despite a huge amount of effort. Likewise with the common cold — and we seem to be losing the battle against bacteria as they develop antibiotic resistance.

I don’t mean to say that technology won’t change. It can and surely will. Just to say that there is a certain wildness to the predictions of the future at the moment. People seem willing to believe just about anything, so long as it has a technology angle.

When the bubble finally pops, it will take with it not only the valuations of some of the biggest technology companies, but also a lot of utopian visions of the future.

In the News story I call it a recency bias but you might as easily call it an availability bias. We are very willing to believe technology can change the world utterly and quickly because in living memory personal computing has created very visible changes in our daily lives. (Maximally visible, but not necessarily maximally important – the famous hypothetical is whether you’d give up the internet before you gave up indoor plumbing.)

IT’S THE STUPID ECONOMY

These cognitive biases have been allowed to grow unchallenged because of the peculiar financial circumstances of the times.

Some people argue the loose monetary policy of the last decade does not explain high asset prices, but I think they’re wrong. The simultaneous global bubbles in property, bonds and tech stocks almost certainly trace their roots to the low/zero/negative interest rates across much of the world, and quantitative easing that left developed economies awash with liquidity.

The money flood provided patient capital that gave companies with scant profits a long time to experiment and expand revenues. If you’ve ever taken an Uber using a 50 per cent discount, you’re using some venture capitalist’s money to improve your own lifestyle, while simultaneously propping up the impression that new tech is destined to remake the known world.

(For what it’s worth, Uber is pretty big improvement over taxis! But its major advantage comes from taking on a regulated market with colossal rents, rather than being inherent to the app.)

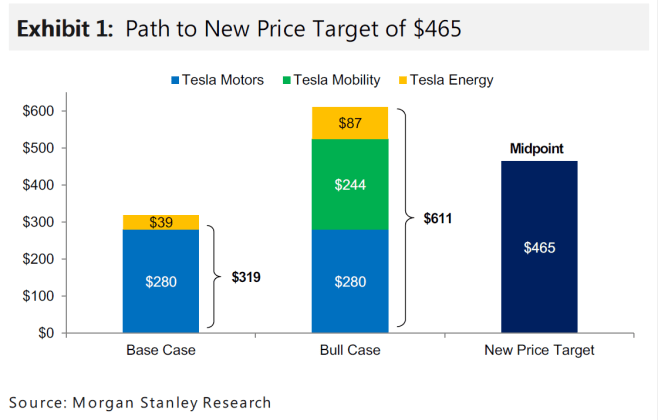

The money flood has propped up some far more dubious beliefs than the prospects of Uber. The faith certain investors have in Tesla’s ability to win a giant share of the “shared mobility market” (fleets of driverless taxis) is intriguing to me.

Valuing a junior company on the prospects of winning a large share of a market that doesn’t yet exist, using technology that is in its infancy? It seems, um … more optimistic than is prudent. If this kind of thing works for Elon Musk, perhaps he should also set up Red Real Estate and start selling rights to land on Mars.

The NASDAQ chart above explains why the cognitive bias we’ve developed has been allowed to progress so far. It’s a feedback loop from confidence, to investment, to expanding revenues, to stock prices, to headlines, to confidence.

And Bitcoin?! … . Actually no. Let’s not even talk about Bitcoin.

(Non-financial evidence that technology really is changing the world, in the shape of temperature records and CO2 concentrations, doesn’t seem quite so influential on the mass mood. I leave it to the reader to ponder why.)

Eventually, the technology cycle of misplaced confidence and out-sized valuations will find it has reached the highest possible equilibrium and begin to tack backward.

It is likely to do that even absent a macroeconomic reason, but one is coming anyway.

Interest rates are rising in the United States and inflation is lifting. The anti-Keynesian Trump stimulus – adding fire to a booming economy – looks set to intensify those trends. The Fed is now slowly soaking back up loose money. This represents a clear and present danger to any asset whose value is not based on making real money right now.

If the market values of all those tech stocks fall, the stories they told about the future will suddenly appear thin. A pin will prick the bubble of credulity and the stories of inevitable autonomy, existential AI risk and imminent interplanetary expansion will fade from our front pages. The distance between the pssible and the probable will lengthen again.

So I’d like to place a stake in the ground and say we will look back on this era – with a TV show called Silicon Valley; a plan for Elon Musk to become the richest man in the world; non-stop headlines about drone delivery; and a relentless faith driverless cars were just a few months away – with a kind of nostalgia for a simpler and more optimistic time.