Which is sending global markets into a bit of a panic.

Source: AFR

But is this really the moment where the Australian economy comes crashing down?

Lower petrol prices are already a reality, which has the same effect for many households as a reduction in interest rates – more money in their pocket.

This is a real boost to the Australian economy at a time when it really needs it.

And our major trading partner, China, is in the same boat. It is an oil importer and it is apparently stockpiling fast during this period of low prices. Like Australia, China is trying to get growth to continue without causing a surge in inflation. The oil price drop just made this a lot easier.

If lower oil prices perk up the Australian consumer just as a lower dollar makes life easier for Australian business, and China is able to continue to grow strongly, that represents just about a best-case scenario for the Australian economy.

But it’s worth remembering: What goes down can go back up.

If consumers in China and Australia re-set their oil price expectations, and then the price of oil goes back up, it will feel like an interest rate hike – at the worst possible time. In that scenario, with Australian consumer confidence falling as China suffers a blow to growth, anything could happen.

I think this must be the most-seen three-word phrase in the history of humanity:

Made in China

Unlike liberte, egalite fraternite, or love thy neighbour, Made in China crosses national boundaries with ease, creating only a minimum of tension.

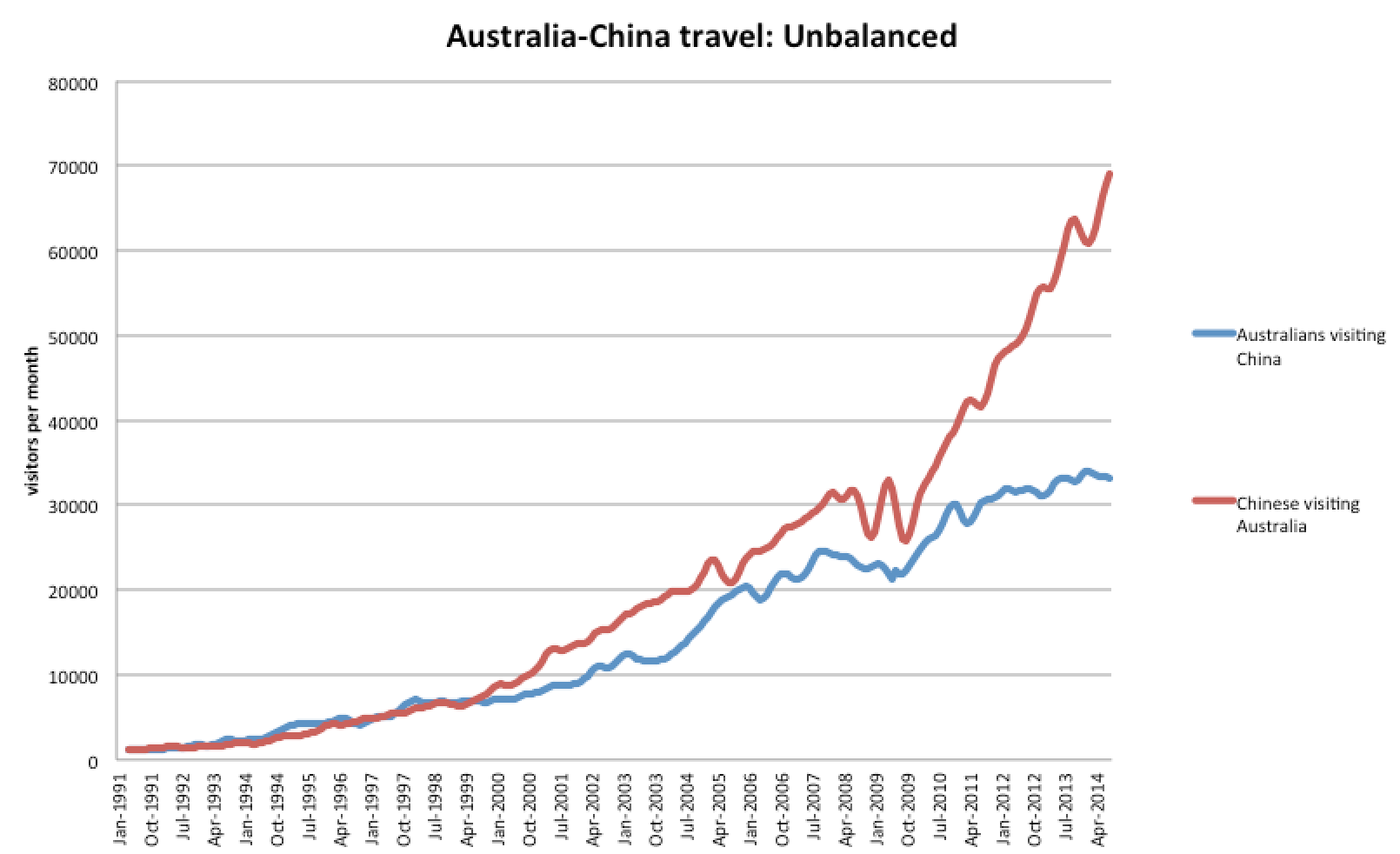

Australia, however, is in the unusual position of running a merchandise trade surplus with China.

This graph shows merchandise imports and exports from Australia’s perspective. Somewhere around 2009, our exports to China started growing much much faster than our imports from China.

So far, so nice. But the imbalance in our relationship has another aspect.

Far more Chinese visit Australia than Australians visit China. This is intriguing.

Should we be worried about this? What does it imply about our level of interest in our #1 customer?

Do Australians not even care about the culture and the people of China?

Or is this just the result of there being 60 times more Chinese people than Australian people in the world? Certainly it is the case that the 23 million richest Chinese are richer on average than the 23 million richest Australians. (That’s all of us).

What will be interesting to see is if there is any correlation between the exports of merchandise and the exports of tourism services. When the taste for our iron ore drops off, will our hotels suddenly lie empty?

IN the meantime, I strongly recommend Beijing, especially if you can get there on a day when it’s not too smoggy.

China’s economic growth has been very strong for a decade, making Australia one of the richest countries in the world. China has buffered us from the GFC, boosted exports, lifted house prices and invested in our businesses.

But Harvard Professor Lant Pritchett is doubtful about those forecasts. The economic development expert has published a working paper full of reasons why China is far more likely to come to a bust than continuing boom. If he is right, the Australian economy will be stuffed (a technical term) and we’ll probably all lose our jobs.

“History teaches that abnormally rapid growth is rarely persistent.”

This is the unique angle of his story. Pritchett doesn’t purport to analyse China in depth. He looks at economic history, comparing China’s streak of success to other countries’ growth spurts, and predicts reversion to mean.

“regression to the mean is the empirically most salient feature of economic growth. It is far more robust in the data than, say, the much-discussed middle-income trap.”

I’m inclined to think this approach has strengths. The current trope about Chinese policy-makers is that they simply set the level of economic growth that they want.

If this is true they are the only country in the world with that power.

What do we really know about the Chinese economic policy-making apparatus? We know only that it has been very successful, according to its own statistics. And everyone acknowledges those statistics are rubbery.

Pritchett compares betting on China to investing in the best-performing managed fund – past performance is no guarantee of future performance, he cautions us.

“The lack of persistence in country growth rates over medium- to long-run horizons implies current growth has very little predictive power for future growth”

Pritchett, it turns out, really hates extrapolation:

“Paul Samuelson’s textbook predicted in 1961 that there was a substantial chance that the USSR would overtake the United States economically by the 1980s. There was a widespread view right up until the end of the 1980s that Japan would continue to grow and outcompete the world. Or in the opposite direction, consider the pervasive pessimism of even a decade ago regarding Africa. Since then, African countries emerged as a majority of the world’s most rapidly growing nations.”

His paper shows the correlation between growth in one decade, and growth in subsequent decades is low: from 0.3 for adjacent decades, down to around 0.1 for decades separated by 20 years.

“The median duration of a super-rapid growth episode is nine years… China’s experience from 1977 to 2010 already holds the distinction of being the only instance, quite possibly in the history of mankind, but certainly in the data, with a sustained episode of super-rapid (> 6 ppa) growth for more than 32 years.”

Pritchett instead suggests China will grow at an average of 3.3 per cent a year over the next decade. That means China’s GDP will be about half of what it would have been by 2033 than if it grew at 7 per cent.

Pritchett does make one concession to analysing China itself, and that is to note that growth is, on average, less variable in countries that are more democratic.

“For China, continuing to have rapid economic growth while maintaining its current level of democracy (as proxied by its Polity score) … would make it more and more anomalous.”

So if China crashes, what should you do?

1. Have a job that doesn’t depend on China (BHP bad, Qantas bad, universities bad, milk exporters bad. Doctor and primary school teacher probably safe.)

2. Have a job that can survive in a downturn. (BMW retailing bad, electricity retailing good)

3. Get out of shares. Australia’s corporate profits depend on Australia’s growth, which depends on exports to China. A China collapse and a stock-market collapse would look like that Olympic event where the two divers leap from the platforms at the same time.

4. Sell your property. China props up our house prices directly (by bidding on them) and indirectly (by making us wealthy). When the firecrackers stop popping in Beijing, auctions in Australia are going to be cold and quiet for a few years.

5. Put your money in a government guaranteed deposit account (and get ready to get very little interest indeed, because the RBA will be busy cutting rates to near-zero.)

In summary, let’s all hope Mr Pritchett is really wrong.

Are they right? The question we are asking here is not merely academic. If we bet on China and lose, the following are likely to fall:

The Australian dollar.

Australian economic growth.

Australian share market.

Australian house prices.

The Chinese government obviously wants the economy to keep growing. The continued existence of the Communist Party is tied to the performance of the Chinese economy. They have to keep it ticking over. Their motivation is clear and pure and strong. But motivation is not always enough.

Can we distinguish warnings signs from red flags?

Consider this. The only reason markets need to trust the Chinese government to add more stimulus is that previous rounds of stimulus haven’t done enough. Financial markets are betting the guys that got the market into this pickle can safely navigate out again.

“We expect Beijing to launch a series of policy measures to stabilize growth. Likely options include lowering entry barriers for private investment, targeted spending on subways, air-cleaning and public housing, and guiding lending rates lower,” said Hongbin Qu, chief China economist at HSBC.

A few iterations is enough for the human brain to learn a pattern. We’ve seen the Chinese government come to the party during the GFC and during the European debt crisis that followed, keeping China’s growth rate up over 7 per cent, rain hail or shine.

No wonder traders and hedge fund gurus trust their guts on whether the dragon will roar again. But a well established patten hurts the most when it breaks.

This time the problems in China seem to be inside China. They are not dips in demand caused by a failing USA or Europe.

You can bet these weird Grotto apartments in Shanghai sell at a premium.

The question is what will happen when Chinese house prices fall. It’s easy to imagine that it will happen in a controlled way, or simply not be too important. That’s what Ben Bernanke imagined pre-GFC too.

China is enormous and its government freer to act than most, due to the absence of democracy. I suspect any crash would be over sooner than some expect. But even a short dip would be a big problem.

The value of China’s growth has been that it is consistent. It can be counted on. Having to risk-weight China’s future growth will take a lot of shine off Australian asset prices. House prices would be under attack from all quarters, with receding Chinese purchases, a falling share-market, and a weakening Australian economy. Bank shares, which account for a quarter of our stock market, tend to follow house prices. The Chinese government’s ability to manage its economy has become, it seems, one of the biggest risks to our wealth and well-being.

A nation with an average income of $205 in 1980 now has average income of $6000.

If the world’s aid programs had lifted 400 million people out of poverty, aid policy makers would barely be able to get out of bed for the pile of OBEs, Pulitzers, Nobels, Honorary doctorates, emmys, grammys and groupies littering their house.

Beacon of hope (retired)

These crucial policy changes in China have come while “leading” democracies have spent billions of dollars on wars of whimsy in the middle east, blown up their financial systems, had great big shouting matches over threats to shoot themselves in the leg (i.e. government shutdowns), and put the greatest policy development efforts into “stopping the boats”.

That’s one reason why Australia’s biggest policy success of recent times has been monetary policy. It is set by an independent body, the RBA.

That’s also why Infrastructure Australia was set up, to try to wrest control of important billion-dollar investments out of the hands of here-today, gone-tomorrow MPs.

“People in political debates no longer distinguish the phrase “you’re wrong” from the phrase “you’re stupid.” To disagree is to insult. To correct another is to be a hater.”

“unskilled individuals suffer from illusory superiority, mistakenly rating their ability much higher than is accurate. This bias is attributed to a metacognitive inability of the unskilled to recognize their ineptitude”

Are we too stupid and arrogant to be allowed to manage our own government? They say you get the government you deserve, and when I look at Australian governments at federal and state level, I conclude we must have been very bad indeed.

So. Should we look into benevolent dictatorship? The argument is an easy one to make when you are browsing World Bank statistics.

But one morning in late October, as I was about to pass under the Gate of Heavenly Peace in a cloud of smog, we saw a big bunch of protestors being dragged off to one side by Chinese police and secret police. I’d lived in China in 2003 and never seen this sort of thing before.

That was frightening. The Chinese government blames the East Turkestan Islamic movement, based out in the majority-Uyghur west of China. They seek independence for a sliver of China near Russia. The Chinese goverment’s behaviour out there has been described by Amnesty as “years of attempted erosion of the ethnic identity of the Uighur people of the region by the ruling Han majority.”

You can’t as easily get away with that in a country with a free press and representative democracy.

Perhaps the most enduring image of Tiananmen square, for me, is these fire extinguishers, which are dotted around. When I saw them, I thought “What for? This square is made one-hundred per cent of stone. There is nothing flammable here.”

Then I looked around. Realised what the flammable material was. And I started to feel a bit sick.

But that does not mean Beijing has given up. When I was in Beijing in 2003, there were just three subway lines. Now there are a dozen.

New stations are popping up everywhere like a game of whack-a-mole. On our holiday in 2013, we picked up a subway map (actually it said subwang) at our accommodation, and it was already out of date.

This is something Australia could learn from. When you build a road to solve a traffic jam, that road will likely last until the collapse of the civilisation it supports.

What you are doing – in the long run – is not “solving a traffic jam” but shaping your city.

People like to talk about induced traffic from new roads – “if you build it they will use it.” I don’t doubt this is partly true, but I think the long-run effect of a new road is far greater than whether or not you get your traffic jam back within 18 months.

This is why I am so excited about the prospects of improvements to rail networks. They can also last a very long time, and have long-run positive effects, not least of which is discouraging the building of more roads.

The city-shaping effects of an efficient metro system in Melbourne would be huge. But a great deal of political change will have to happen for it to get built.

Last night “tea guy” came on the show and talked non-stop about tea. He may have been on the autistic spectrum – couldn’t listen, kept talking on top of the hosts and other contestants. No wonder he got kicked off.

Oh you didn’t see that episode? I’m talking about If You Are The One, the Chinese dating show that is currently storming the world.

Last night, on twitter, the hashtag #ifyouaretheone was trending higher than the hashtag for the tennis #ausopen.

The format of If You Are The One is elaborate:

24 accomplished and attractive women are arrayed behind podiums. A man comes down in an elevator with music blaring. From the minute his shoes appear, the women can start “turning off their lights.” The man has to answer a bunch of questions from the girls and the three hosts, and he shows videos about himself. If any of the girls leave their lights on until the end, he gets a date. You can watch an episode here.

What makes the show so fascinating is that within a few minutes of his arrival, the male contestant’s score – shown on a big screen – is generally down to about 4/24. It is nail-biting. Then he says one dumb thing and it’s down to 0/24. Then he has to leave. With the demographic imbalance in China, the women are harsh.

It’s like an episode of the Bachelor where all the ladies walk out in the first few minutes and we watch the Bachelor’s bottom lip tremble as he struggles to hold it together.

“Tea guy” who I mentioned earlier, bombed slower than most, because it was like watching a car crash in slow motion.

For the failures, they put up an email address on screen at the end, which interested parties can email in search of love.

All this is a breakthrough for China – the first TV show that has proved to be a successful export. That has the capacity to dramatically change the way we see China.

China didn’t have that. Monolitihic state-run media strangled the life out of the creative sectors.

And that means people believe things about China that are not true – Chinese people are all the same; Chinese people just love to work; Chinese people are not funny. It’s this last one that gets me the most.

Sure, Chinese people aren’t always funny in their second language. That requires a lot of fluency. But over there, there is a huge premium on being a joke-teller. A night out with Chinese people involves lots of raucous laughter. And there’s an extremely popular kind of stand-up comedy, unique to China, called cross-talk.

China does have cultural exports. It’s just that at the moment, most Chinese icons are from a previous era – the great wall or the forbidden city.

There’s not much out of contemporary China to love. Top Chinese brands are Hai’er, which makes white goods, and Lenovo, which makes computers. They lack the cachet of Miele and Mac.

But “Made in China” is losing its shame. We know Chinese-made products will be of good quality. That can extend to cultural products, not just physical products.

What If You Are The One shows, is that a Chinese PSY (gangnam style), is not too far away. A breakthrough cultural product that reveals modern China to be more than just smog and factories.

On my most recent trip to China I visited the 798 Art precinct in the north of Beijing, a former industrial zone packed with more galleries, studios, craft shops and street art than you could see in a day. (as this blog calls it, the hipster district.) It was amazing. Chinese creativity is there and it is just about to break out of its cage.

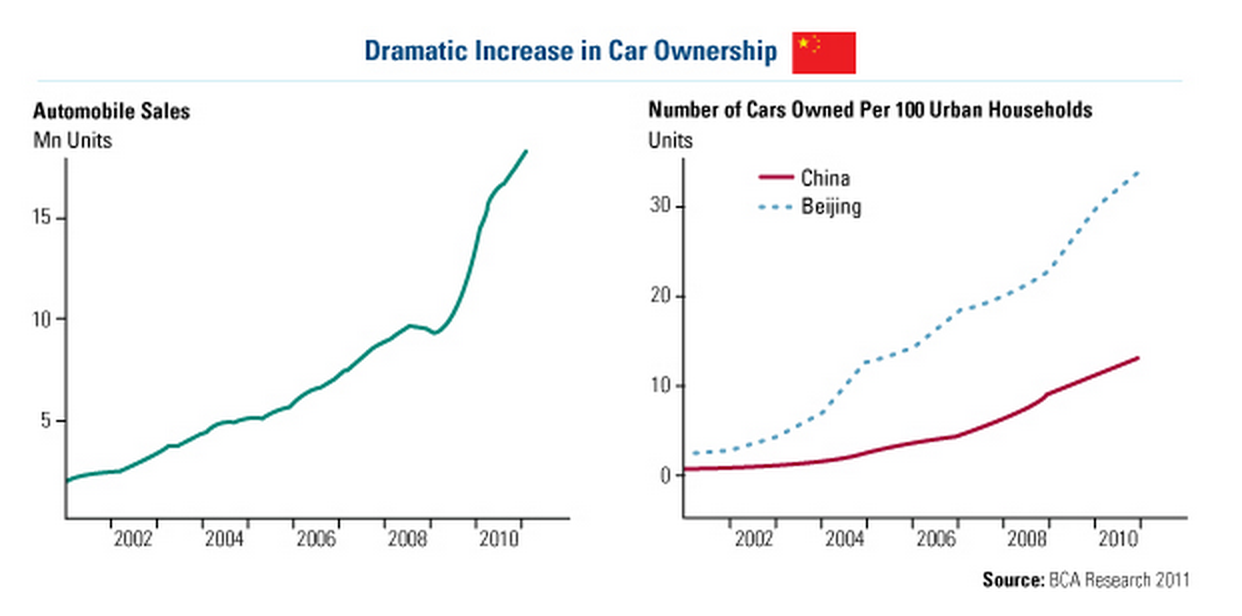

On my recent trip I was gobsmacked by the number of buildings going up in China.

North BeijingWay outside BeijingJust off the Bund, ShanghaiShanghaiShanghai

Economists are trained to be cautious around their intuitions and gut feelings. The best bits of economics are, after all, counter-intuitive.

But I couldn’t help wondering what would become of all this building. A lot of old buildings are being knocked down, sure, but if the replacements for two storey courtyard houses are 20 storey apartment blocks, and there is no population boom afoot, the risk of over-building is real.

If China’s property boom turns out to be a bubble, and Chinese growth slows or reverses, the effect on Australia will be nothing short of a calamity. The mining industry and the housing market will do a simultaneous nose-dive. The biggest companies in our stock exchange will lose a lot of their value. Wealth will be crushed, spending will stop, bankruptcy will be rife, firings and downsizing will follow. In short, a recession.

(And if we have Tony Abbott and Joe Hockey in charge at the time, we are unlikely to get an adequately Keynesian response)

One closely watched canary in the coal mine is the interest rate between Chinese banks.

It spiked in June, December, and again this week. The precise meaning of that is uncertain. But it certainly looks like the central government trying to discourage cheap capital flows. So far, each spike has been short-lived.

“Yes, the property market has overheated in certain areas and yes, perhaps property prices will come down, but it won’t necessarily have a major detrimental effect on the banking system, primarily because the banking system hasn’t been the main funder of property prices.”

The thing about the Chinese financial system is that because the banks are so regulated, people lend money through the “shadow banking” system. That name sounds a little spooky, and so it should.

That reminds me of the Pyramid Building Society, which went broke in the 80s. Crazy high rates can genuinely prove too good to be true. If Alibaba is raising capital at a high rate, and lending to property investors, it is worth asking if it could end up insolvent when property prices fall. And it is worth asking if that might spread.

“[O]ur expectations about the possible macroeconomic effects of house price declines were shaped by the apparent analogy to the bursting of the dot-com bubble a few years earlier. That earlier bust also involved a large reduction in paper wealth but was followed by only a mild recession. In the event, of course, the bursting of the housing bubble helped trigger the most severe financial crisis since the Great Depression. It did so because, unlike the earlier decline in equity prices, it interacted with critical vulnerabilities in the financial system and in government regulation that allowed what were initially moderate aggregate losses to subprime mortgage holders to cascade through the financial system. In the private sector, key vulnerabilities included high levels of leverage, excessive dependence on unstable short-term funding, deficiencies in risk measurement and management, and the use of exotic financial instruments that redistributed risk in nontransparent ways.”

China’s shadow banking system has helped propel the country’s debt-to-GDP ratio over 200 per cent.The biggest burst of economic growth in history stretches back to 1975. It will end one day. Probably not in 2014. But it will be worth being prepared when it happens.

Since Chinese New Year is approaching, this week will feature a series of posts on the biggest fish in the economic pond. Click through for Part 2, and Part 3

I recently went back to a town I used to live in. Beijing.

They say: “You can’t step in the same river twice,”

Nowhere could this statement be more relevant. Since I arrived on a snowy afternoon in 2003, until late 2013, Beijing has experienced average annual economic growth of 10.4 per cent and changed presidents twice.

OLDNEW

To return to Beijing is to find yourself in a very easy game of spot the difference.

When I emerged from the subway on my way into town from the airport, I was sure I could navigate to the hotel. But before long my companion saw my confident stride slow, my mouth hang open, my head swivel side to side as I searched for familiar landmarks.

McDonalds DaZhaLan

Right in the middle of Beijing, in a place I knew inside out, a brand new six-lane road had been built, right through what had once been an area of narrow alleyways and traditional courtyards. And on the corner of that horrible traffic funnel and one of the famous silk-selling streets was now a McDonalds.

I was upset. I raved on and on about it until my companion put earplugs in.

It was only a couple of days later when I discovered why this disruptive and massive road – Meishi Jie – had been built. And I was suddenly willing to forgive it entirely.

There is another road two minutes away called Qianmen Street. It lies on the crucial north-south axis of Beijing. If you followed it north, you’d drive right through Mao ZeDong’s resting place, the monument to the people’s heros, the gate of heavenly peace, the centre of the Forbidden City, etc etc.

Despite its feng shui importance, when I lived in China in 2003/04 it was a traffic-choked abyss of unpleasantness. I avoided walking down it when I could.

But now! Now it was a pedestrianised mall. And not only pedestrianised. I could have just about died of delight when I saw, rolling along among the tourists and touts, a tram.

ding ding!

China’s reputation for traffic problems and air pollution problems is well-deserved. As the traffic status of the old Qianmen Street was a bellwether for the state of China across the following decade, so this new, improved Qianmen Street might be a sign of a smarter, more urbanist future. So I thought.

My eagerness to ride the tram was at boiling point. [nb. I am not now, and never will be, cool.] So imagine my shock, nay abject disgust, when I learned that the thing travels just 840 metres and costs 20 yuan.

At today’s exchange rate that’s $A3.77, or $US3.31. That is not just more than a Melbourne tram ticket ($3.58), it’s ten times the price of the Beijing subway fare (2 yuan).

Even the outrageous San Francisco Cable Car ($5 a ride) is only about 50 per cent more expensive than taking a ride on BART.

In the time I saw the tram rolling up and down, it had at most two passengers. Of course it won’t go broke – it has the might of the PRC behind it.

But the tram is pure symbolism, which has an insidious effect. It undermines people’s views about the true usefulness of that kind of transport. (Incidentally, this is why Canberra should not build a tram. It will run very visibly empty up and down the middle of the city and reinforce perceptions Canberra can’t do PT.)

Thank god China has an undying love affair with trains, or their troubles would be about to multiply very fast indeed.

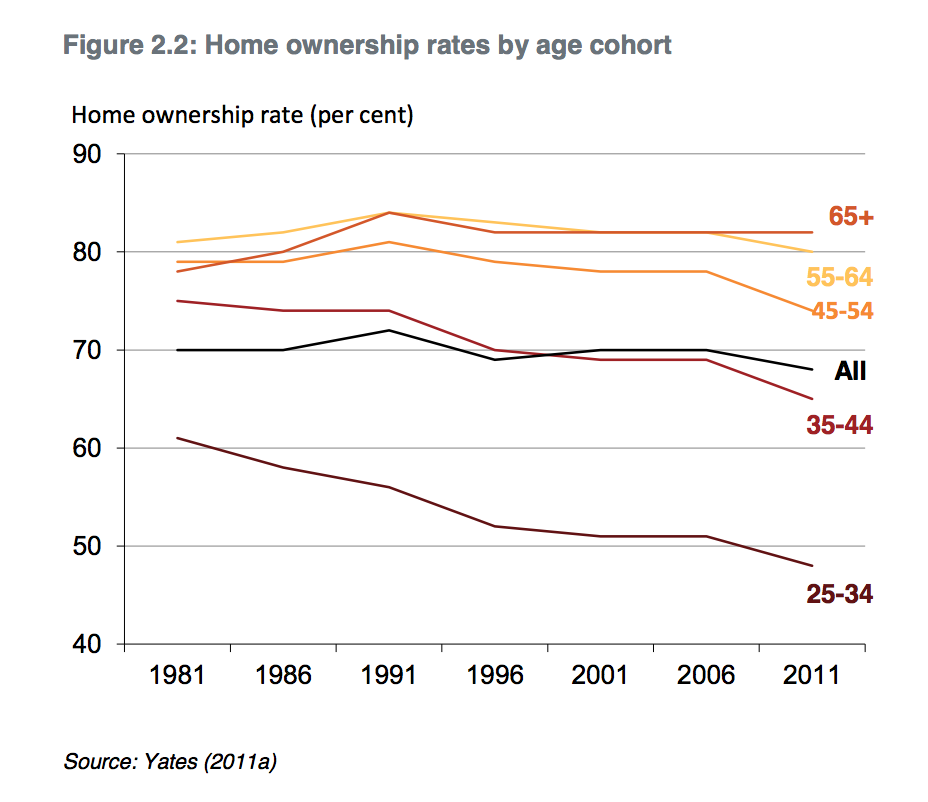

This chart from a Grattan Institute report was used as a hand grenade in a war over house prices on Twitter a couple of days ago. Union economist Matt Cowgill argued house prices may be too high if they are pushing people out of the market.

Another economist, Stephen Koukoulas, argued everything was fine and you should just go and borrow from the bank since interest rates are at record lows.

(Just as a declaration of my interest, I’m 32 years old and do not own property.)

Some people argue house purchase has simply been delayed, just like moving out of home, getting married, and having children

This is a pretty good theory to explain the above. But it doesn’t do such a good job of explaining the declining rate of first home purchase. That has hit a record low of 12.3 per cent in the most recent data.

You have to assume that low – which coincides with recent house price growth – is temporary. So what will give?

Will we observe a quiet tsunami of saving that allows first home buyers to collect together huge deposits, then climb back into the market with heaps of spending power?

Bad news if you are relying on that. Gen Y is not scrooging it up.

While young people’s net worth rose around 25 per cent in this period, the price of established homes rose 40 per cent.

The average value of the savings of people aged 25-34 (bank accounts and shares, not including super) has risen from $11,000 to $16,300. It’s not nothing, but it’s not exactly a deposit on a house, either.

So will the 65+ demographic eventually be forced to release their vast real estate holdings onto an anaemic market?

Can we conclude that house prices are going to fall?

Not necessarily.

The x-factor in Australia’s housing market may be off-shore buyers. Chinese wealth is pouring into the market at both ends, propping up the value of both million dollar mansions and cheap apartments.

Economists understand that markets operate at the margin. It doesn’t matter what most people do so long as at the margin there is one bidder with deep pockets.

Foreign investment in Australian real estate rose from $41.5 billion in 2010-11 to $59.1 billion in 2011-12. Fast-growing China was the 3rd biggest source, behind the USA and Singapore.

Location, Location, Location.

So long as foreign wealth, and especially Chinese wealth keeps accumulating, domestic dynamics are only part of the picture. I intend to return to this topic soon, because the pace of accumulation of Chinese wealth is now not just a historic record but a gigantic outlier. Whether it can continue is of intense relevance to all of us, and there’s plenty of people who think a crash is coming soon.

{kind=link}

{kind=link}