Is the housing sector so pumped full of credit it is about to explode? Or is the business sector so credit starved it is about to die?

Is the housing sector so pumped full of credit it is about to explode? Or is the business sector so credit starved it is about to die?

EDITED on Tuesday September 29 to make it better, fairer, more accurate.

My hypothesis is this: A large part of the Australian public does not understand the tax reform “debate” at all. a substantial part of the tax reform debate.

I hypothesise these people are smart, capable and have Australia’s interests extremely close to their heart. But they have no training in tax theory and therefore lack mental models to understand why, for example, Labor’s Chris Bowen, Shadow Treasurer, would be willing to consider cutting corporate tax to 25 per cent.

They just don’t see how tax affects growth.

The most mentally available model of tax is not one where tax is an ingredient in making the cake, but a knife to cut it up with at the end. This matches lived experience. As a worker and consumer, tax happens at the end of transactions. You get paid, then you pay tax. You buy something then you pay GST at the checkout.

So my hypothesis is the concept of tax as an input to the rate of economic growth is not one that is available to most people.

I’ve been thinking about this hypothesis for a while. Today I decided to test it. I chose the following four tax-related articles and read the comments in all of them.

The Age: Malcolm Turnbull halts tax white paper in major reset (163 comments)

Herald Sun: Imbalanced Tax system stunting growth, says Business Council of Australia (7 Comments)

The New Daily: Scott Morrison wants to give us tax cuts (22 comments)

SMH: Scott Morrison: Work Save Invest the Mantra for the new Treasurer (90 Comments).

If people understood that the tax reform was about boosting growth, I expected to see comments engaging on that topic – supporting the link or refuting it, talking about high-tax high-growth countries like Scandinavia, and low-tax low-growth countries too.

If people did not bring this frame of reference, I expected to see the comments focus on other topics, especially distribution.

I read about 280 internet comments. (Which – as you can imagine – meant deciphering a great number of garbled sentences and enjoying an even greater number of insults.)

I coded them according to whether they mentioned growth or output; distributional outcomes; loopholes; or ‘other’. ‘Other’ accounted for over 200. The remaining results were crystal clear.

Discussion of growth was present in just over two per cent of total responses and was outweighed by discussion of distributional issues about 9:1.

Discussion of growth was present in just over two per cent of total responses and was outweighed by discussion of distributional issues about 9:1.

I tried to be generous with the comments I coded as addressing issues of growth. Here’s one:

“The most important thing to do to fix the economy is to get the taxation right! Fact is the economy under Abbott and Hockey was a blatant disaster getting worse!”

Here’s another:

“Penalty levels of taxation combined with high levels of social welfare payments result in deficites, high borrowing costs and a downward spiral of he economy. That is exactly what is happening in Australia. Our economy is headed the same way as the Greek economy. To reverse this Australia needs to increase the incentive to work and invest and reduce the reward for not working.”

In the 61 comments about “loopholes” there were very many along these lines:

“No change in the policies, give the big end of town a tax cut, and spread the burden over everyone with an increase in the GST. Lower income people are worse off as a result.”

Please note that I am not criticising this last comment. Distributional issues are a crucial part of tax policy and that kind of comment is an important input to a well-grounded tax debate.

The point is we do not have a well-grounded tax debate until everyone is on the same page.

The broader tax debate does not address the impact of tax settings on the output capacity of the economy. It is far more focused on fairness.

The “elites” must work to understand the grip matters distributional have on the public imagination. If they still want to press on with tax reforms – and I think they probably should – they need to take two courses of action.

Elites, building a case for reform does not mean repeating the phrase “We need reform!” It’s truistic to the people who understand it, while confusing and annoying to everyone else. It sounds like you’re talking in code, and that implies you’re plotting something.

Instead, talk about “changing tax law so businesses want to do more work in Australia and hire more people.”

If you hector people about tax by saying “it affects investment decisions!” you’re unlikely to cut through. “Investment decisions” sounds like it has something to do with Macquarie Bank.

The comments on the article about Scott Morrison’s “Work Save Invest” slogan showed “investment” was uniformly interpreted as being about buying shares. Many commenters pointed out they couldn’t afford to do that. “Foreign investment decisions” is probably even worse language. It conjures Chase Manhattan and Bank of China conspiring to rip us off.

Talk about economic growth in language people can understand. Use this language even among yourselves, so when it comes time to talk to “real people” it comes naturally.

One way to build capacity in the community is through using metaphors:

But that can’t be all. The explanation needs stories about business owners who expand their business once their returns meet a benchmark, and how returns are affected by tax. I can imagine an animation. A business owner making a business plan. Every time she does the maths she comes out in the red, until the tax percentage becomes lower. Then she opens her shop and hires some staff.

Understanding a concept requires knowing several mutually-reinforcing stories that illustrate the same point. The Australian people have not heard enough of these stories. And that is why Tax reform is going nowhere.

NB: In todays’ Fin Review, Laura Tingle talks about this exact issue:

Just as the tax reform debate threatened to choke itself on too many conflicting agendas – increasing the GST, lowering company tax, fixing bracket creep, doing something about superannuation tax concessions – our new treasurer has injected a rather important ingredient: the need to define a reason to do it all.Some of the contributors to the AFR Tax Reform Summit this week have made the observation that an organising principle for the tax reform debate has only rarely been seen amid the worthy, but perhaps too often repeated, calls for individual tax measures to be addressed.

The organising principle needs to be a political argument to voters about why you actually need to mess around with tax in the first place. An argument about corporate competitiveness isn’t really going to cut it out in the ‘burbs.

Yes, we all heard Tony Abbott and Joe Hockey talk ad nauseum about “lower, simpler, fairer” taxes. But they were never able to cut through to voters about why this was such a good idea: that it would – or should – help boost and transform the economy. Instead, it just sounded like a bit of conservative government ideology.”

So if Morrison wants to prosecute that case for tax reform he needs to formulate a story that’s as clear as “Stop the Boats” but for a much more complex concept. Good luck Scott.

Here’s a late-breaking caveat I decided to add.

Among the people who appear to not understand the nature of tax reform are a group who understand it perfectly well but oppose it. They fan the flames of the distributional arguments.

They’re not the only self-interested sorts in the debate.

The fact company tax cuts are now widely accepted as the most growth-crucial tax cuts in our whole economy is very interesting. Of course cutting it would help growth. But at what revenue cost? And why is it #1? Self interest lurks in any issue where facts are complex.

This post is a quick, simple game theory explanation of Australian politics. It’s not comprehensive. It cuts out a lot of detail. It simplifies radically. In doing so, it aims to shine a light on one interesting dynamic.

Please don’t get the impression I’m unaware other dynamics are running at the same time. This is just one strand in Australia’s politics – but an interesting one.

–

Tony Abbott learned a lot from John Howard. What he learned most apparently, was the lesson of the 2001 election – that an environment of negativity and fear and a focus on national security benefit the incumbent.

Abbott ran hard on national security. We have planes in the air over Syria because of those lessons – learned when Abbott was 43 and had been in parliament for seven years. Not to mention our new paramilitary Border Force. Even his elevation of the anti-methamphetamine campaign to a national level seemed to be part of a campaign to whip up fear.

Was he fundamentally wrong?

I say no. The reason Abbott couldn’t get an edge on national security was Bill Shorten stuck to him like sticky stuff to a blanket. Suffocatingly bipartisan on every issue, Shorten appeared to know that the slightest bit of space between him and the PM would be blown out of proportion.

Shorten refused to break his national security lock-step with Abbott even if it cost him. When “Border Farce” was announced Shorten was all for it. Shorten also supported boat turnbacks even though his party was very suspect of it.

National Security bipartisanship was not a rule of thumb for Labor under Shorten. It was iron law.

All this meant Abbott’s chosen strategy got no lift-off, and as he pushed it harder and harder (e.g. by begging the US to ask us to bomb Syria, and repeating the phrase Death Cult reflexively), he looked somewhat mad.

In essence, Shorten played the game of chess correctly, from a political perspective. Abbott’s fear and negativity strategy was absorbed perfectly and seen off.

Now the government is trying something different. Positivity. Malcolm Turnbull keeps repeating that it has never been a more exciting time to be Australian, and talking about opportunities. No more Death Cult.

I love it. This is the political discourse I crave.

But the person craving it even more might be Bill Shorten.

He’s been a strangled and ineffective communicator for the last two years. But that could be the result of being forced to play “small target” and match Abbott on the fear side.

Now the game is about offering competing positive visions? That’s Labor turf. They invented NDIS. They can offer a vision of Australia where we have not just wealth, but wealth with a bit of meaning and compassion.

Today even, Bill Shorten has been out announcing a policy. Labor will reverse the Government’s higher education cuts and offer tertiary education places to disadvantaged people.

People love to write Bill Shorten off. But if you look past the zingers to the chess game being played beneath the surface, you can understand why the Labor Party chose him.

I read an article in the Guardian the other day calling for an end to online comments.

“On most sites – from YouTube to local newspapers – comments are a place where the most noxious thoughts rise to the top and smart conversations are lost in a sea of garbage.”

Prima facie, there’s something to this argument. There are a lot of downright scary comments online. YouTube is about the worst place for it. I figure that’s because videos are the main intellectual sustenance for people who can’t read well, so when it’s time for comment you get the blatherings of the intellectually incapable.

(Here, by contrast, the readers are shining beacons of erudition and compassion and the comments section is a delight. ;) )

So partly, the problem is that different sites have different readers and not everyone’s worth listening to.

But think about The Guardian. In theory it’s a thinking-person’s paper. But the comments section is a disaster. What’s the explanation?

(Nobody is going to die of surprise in the next paragraph as the economist reaches for the folder marked I for Incentives.)

The problem with online comments is the incentive structures! For some idiot with anti-social views, this is his one chance to get his views amplified. The pay-off here is high. Normally he can’t get anyone to listen. But if he quickly writes something inflammatory, he can spend a happy afternoon jousting with people he made angry.

The intelligent person looks at the animals head-butting each other in the comments section and can see no reason to get involved.

For the Guardian writer up above, there’s no solution to comments beyond chucking the whole system out. I know different because I spend a lot of time on Reddit. There’s a site with a wide variety of people on it, from all over the world, from all over the political spectrum, of all ages and of all levels of education. And the comments over there often genuinely brim with wit and intelligence.

Reddit is nominally a link-sharing site. But the value of it is actually in the comments. How do they do it?

Reddit’s comment section is ruled by two main incentive features. Upvotes and Downvotes. Users can upvote or downvote any link or any comment.

Upvoted comments rise to the top. Vile idiocy exists on Reddit, of course. But it sinks into the murky depths where it is little seen. And any comment that gets more than 5 net downvotes disappears from view.

So the incentive system is different. Instead of bad comments floating round riling people up, they disappear. That disincentivises trolls.

And good comments are rewarded.

Every user has a “karma” account that tallies their “karma” – simply the total upvotes they’ve ever received. This Karma is not exchangeable for gold, rubies or bitcoin. It has no value. But those status-seeking missiles we call human minds don’t give a damn. One of the problems on Reddit is actually people doing dumb stuff for karma.

While other sites do have incentives – e.g. the New York Times picks, the Reddit system is a more proven success.

Redditors can ask a stupid question on the site and see a dozen people go scurrying off to provide a well-written, well-researched answer provided with wit and goodwill. Reddit’s growth is extremely rapid. The site has seen 1.7 billion comments so far.

This system is actually the goldmine lying beneath the land investors in Reddit purchased. They may have thought they were buying a succesful domain name or a winning web brand, but what they’ve got is a killer comment system they need to patent, ASAP.

And then preferably license out. The comment threads of the world need it desperately.

I haven’t been updating the blog quite as often as I would have liked but I haven’t been totally idle either. Here’s a few pieces I’ve written in recent times for other outlets.

Crikey

With Silk Road iced, budding entrepreneurs bluntly selling drugs online* (Still paywalled for now)

If oil prices are tumbling, why is petrol so damn expensive?

Stocks: hold ‘em, fold ‘em, walk away or run?

CEOs trump MPs for profligacy, but at least they’re not wasting our money

Pollies will spend $506m on entitlements in 2015-16 — $2.2m per MP

Would the ALP’s ‘Buffett tax’ put an end to tax-rorting millionaires?

If Greece defaults, it will join an illustrious club of debt welshers (including Australia)

It’s the end of the euro as we know it (and I feel fine)

news.com.au

The truth about running a franchise

Blender wars: Why sellers of stuff are stuffed [If you only click one link on this page click this one. It’s my favourite]

Australia? Japan? Canada? What’s really the best value place to ski?

Masters is the screw up that could hammer Woolworths – and the rest of us

Are Amazon mad? Or mad geniuses?

Is it time to start panicking about China?

Four ways a lower Aussie dollar will make your life better

Why house prices don’t need to be a consistent multiple of income

The New Daily

Babycinos, boutiques impact house prices

Even poor AFL clubs can enjoy finals glory

Forget the big city. We find homes for $12,000

Rising cost of private schools may be driving parents away

Uber’s bait and switch: passengers taken for a ride

Duty free shopping not always the bargain it seems

And lastly, the view from my “desk”:

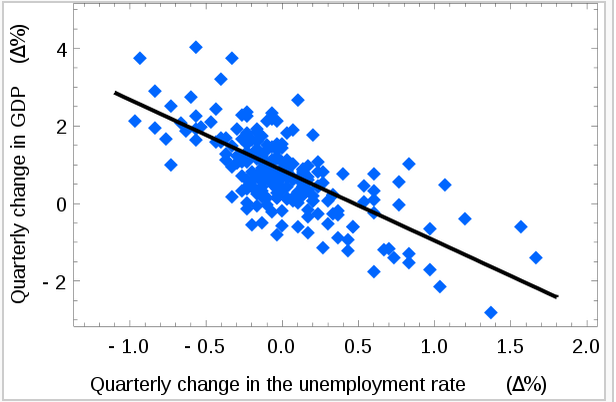

This series started yesterday when I started wondering about the exact reason we needed economic growth to keep the unemployment rate down.

I wrote an introductory post then, explaining I was going to do some learning in public. (The risk of embarrassing myself is real). Now I want to dive into this a bit more.

It’s true we need economic growth to prevent the unemployment rate rising. I checked and important people believe it.

RBA Assistant Governor Chris Kent has specifically linked changes unemployment to trend growth. “Since about mid 2012, Australia’s GDP growth has been a bit below trend and so the unemployment rate has been rising gradually.”

And he has given us this excellent graph:

Phew! That’s one thing I got right.

The link between economic growth and changes in unemployment is real and it has been formalised in a relationship called Okun’s Law.

I put the word out on Twitter for an explanation and I was swamped with awesome economists offering helpful explanations. Thanks to everybody.

I put the word out on Twitter for an explanation and I was swamped with awesome economists offering helpful explanations. Thanks to everybody.

@RHTGreen@jasemurphy Arithmetically, you’ll need enough to keep up with growth in the labour force and technological progress.

— Jim Savage (@khakieconomist) September 9, 2015

This was the main thing I heard. Basically:

This is a nice neat story. If you have 2 per cent labour force growth and 1 per cent productivity gains, you need 3 per cent growth. It’s mathematically sound. I learned something.

So is that it? Are we wrapped up? All silent?

I still find myself with questions. I want to understand things in more than just mathematical terms.

Productivity causes growth. It allows us to produce more, using the same. But we also need growth to compensate for it? This sends me into something of a chicken and egg loop.

I’m aware that chicken/egg scenario is why economics uses maths so much. Supply and demand need to be solved simultaneously. You can’t think through a market equilibrium slowly because you need an answer on both sides at once.

So I could stop here. But I have other questions.

If rising labour productivity is both cause and cure for unemployment, why is it spoken of in exclusively glowing terms? Would we not be as well off, in unemployment terms, without it?

And population growth causes economic growth too. This is what I believe, a belief reflected in articles like these:

Fewer people want to live in Australia in growth risk for RBA

RBA’s Glenn Stevens: Australia may need to rethink growth

If we did not have the population growth, would we still have stable unemployment? This remains my sticking point – my reason for wondering about the deeper reasons and implications of why we need 3 per cent growth.

Seems to me an important part of the existing population is employed creating space for the new population to live in.

While the productivity angle makes sense to me, the population one still gives me pause. Establishing the new capital stock to accommodate the lives of new babies and new migrants is a huge cause of economic activity. More roads, more shops for them to shop in, more buildings for them to live in, more pipes going to their houses, more hospitals for them to be sick in, etc.

New population consumes and works the same as the existing population; but also requires extra spending. I intuitively believe population growth causes a rise in employment so I can’t quite grasp that it’s a wash, unemployment wise.

Whenever I think about this question I think about Japan, where capital is being abandoned as the population shrinks, and (while unemployment is low) secure employment is a problem.

Perhaps I need to think about this differently? Perhaps I need some more empirical evidence? I’ll dive deeper and present what I find tomorrow.

If you have any thoughts on this topic or want to suggest some reading, please feel free to make a comment below.

I like to think of myself as not too stupid. When I don’t understand something, I like to dive into that.

Searching out areas where I feel confused or uncertain is a useful way to figure out how to move forward. I try to shield from public view when these areas of uncertainty are to do with economics. But no more.

I believe we need high growth to keep unemployment stable. But I’ve never really understood why.

My economics education was a good one. But I never did honours – let alone a PhD – and it was a long time ago. They didn’t teach us everything, and I’ve forgotten plenty.

This is my way of saying I don’t know everything about economics. (Despite how obvious it is this is weirdly hard for me to type.)

What I’m doing here then, is going on a learning expedition. Trekking deep into territory that has been explored, but not by me. Maybe along the way I’ll learn something. Maybe even have some insights that are new to me. Maybe even have some insights that are new!? Most likely I will discover everyone else already knew something I didn’t.

This is part 1. I’m expecting to be able to put together a few more parts over coming days as I learn a bit on this topic. But for now, I’m going to write about a few of the preconceptions I have that give me the idea this is an important question to pursue.

At the least this will be a quick two part series where I explain the answer in part 2 and am forced to revise the first thing I said in this post. ;)

Please leave any helpful comments or suggested reading for me in the section below. I’ll write more soon.

I like Gittins and I’m always interested in a smack-down of a new religion, so I started reading eagerly.

But Gittins was unable to deliver a smackdown. Unable to deliver much at all.

See if you can spot the fallacy here:

“Simple statistical theory should be telling economists that a protracted period of below-average growth is most likely to be followed by a period of above-average growth.”

The nicest thing I can think of to say about it is there are economic models suggesting poorer countries grow faster than richer ones. They imply a degree of catch-up – perhaps those were the theories Mr Gittins was fumbling for?

But the problems with the article go beyond just one dodgy paragraph. His whole case against “reform” depends on the idea that the economy will grow just fine without it.

That’s certainly possible. I actually think the economy might well be about to bounce back a bit. But that doesn’t make a case against reform.

Economists know you get growth from adding more people and machines, and then you get extra growth for free via productivity gains. Productivity gains are the really good gains because they come without real trade-offs. You don’t need more ingredients, just a better recipe.

Productivity gains can come from two main sources.

Why do we obsess over the latter one? It’s where we have our hands on the lever. Governments can’t really control innovation at the firm level. Not in the short-term at least. They do control market regulation.

So “reform,” that buzzword that’s as popular as a buzzard, refers to this latter issue. Making markets work better.

Sometimes they work better with less regulation (economists arguing against the taxi cartel, for example) sometimes they need more regulation (economists arguing for a carbon tax or higher capital requirements for banks.)

Whether or not you get the first kind of productivity improvement, there’s a chance you can bring growth into existence by focusing on the latter.

Growth matters.

The desire for growth is not about the hope of self-enrichment. The sad fact is growth remains the only way we know to ensure full employment. Unemployment is horrible. It hurts people and ruins lives long-term. Meanwhile higher growth can bring better standards of medical care, lower infant mortality, safer foods, more opportunities to work in satisfying jobs. So the hunt for growth is a humanist pursuit. Obsessing over it is a risk-averse social scientist’s way of trying to maximise human happiness.

Gittins seems to think gambling on future growth is a great idea.

When you convince yourself, as many economists have, that the only way we’ll see faster growth and further productivity improvement is for governments to engage in extensive reform, you’ve convinced yourself our economy is deeply dysfunctional.

Optimism is an endearing quality in a friend, not an economic policy-maker.

The great thing about market reform is it should work whether or not we’re getting the other kind of productivity inside firms. It’s additive. If Mr Gittins’ optimism is rewarded and we see a great surge of firm-level productivity unleashed, it won’t be a mistake to have unleashed market-level reform too.

There are strong arguments against reform. Arguments about the extent of economic encroachment into our lives. About materialism and reification. About market power. About whether we can shape economic growth in ways that brings us more of the good and less of the bad. These are good arguments we should all be engaging in.

It’s a shame those column inches didn’t attempt such an engagement.

Things look bad.

Today, economic growth figures are coming out (at 11.30am) and for the first time in ages, people are predicting negatives.

Recession talk is in the air. I have my doubts about that. But the talk alone is very suggestive, and there are lots of reasons for it.

Chinese markets are falling, our own stock-market is in a sustained slide, and with all that bubble talk our housing construction sector looks weaker.

Is Australia about to get a surge of growth, or a slump?

Is Australia about to get a surge of growth, or a slump?

One way to answer that is to look at what business is up to. In May, we checked in with business spending plans and they gave me intestinal cramps. Things have changed, sort of…

Capital expenditure is what makes your business bigger, lets you employ more people, etc. It’s one of the big signals of future economic growth. And it’s going backwards.

The mining sector is in such a funk that it won’t bring us any growth. This next graph shows the plans the mining industry has for capital expenditure.

The grey bars show actual expenditure. The last one for 2014-15 is the lowest in four years. The white ones are plans for next year. The latest white bar (3rd estimate for 2015-16) is the lowest 3rd estimate in five years. That is having a seriously negative effect on Australia’s total capital expenditure. Check out the increasing steepness of that slope at the end.

That is having a seriously negative effect on Australia’s total capital expenditure. Check out the increasing steepness of that slope at the end. Manufacturing won’t save us.

Manufacturing won’t save us. But there’s other parts to the economy. Other selected industries are investing more than ever.

But there’s other parts to the economy. Other selected industries are investing more than ever.

Other selected industries sounds like a miscellaneous grab-bag. But check out the labels on the vertical axes. This is a massive part of our economy. Not only that, it just invested more than it expected, which is more than ever. Plans for 2105-16 are more modest, but increasing fast. Other selected industries* includes:

Other selected industries* includes:

Electricity, Gas, Water and Waste Services

Construction

Wholesale Trade

Retail Trade

Transport, Postal and Warehousing

Information Media and Telecommunications

Finance and Insurance

Rental, Hiring and Real Estate Services

Professional, Scientific and Technical Services

Accommodation and Food Services

Administrative and Support Services

Arts and Recreation Services

In other words, a whole lot of important parts of our economy that we can actually believe in.

And there’s one simple reason why they might grow. Our falling dollar.

The fall in our currency is a bit like being a lobster in a boiling pot of water. Unlike stock market fluctuations it happens slowly and we don’t pay it so much mind. But it matters a lot.

The fall in our currency is a bit like being a lobster in a boiling pot of water. Unlike stock market fluctuations it happens slowly and we don’t pay it so much mind. But it matters a lot.

The slow growth of non-mining industries in the last few years can be attributed to our high dollar. America’s incredible recovery from its recession in the same time period can be explained by its low currency.

A falling dollar could flip slow growth on its head. And we’d be too busy worrying about mining to notice.

The current mood of widespread gloom may prove to have been peak fear.

*This whole private capital expenditure data-set excludes healthcare and social assistance, which as we know, is one of the fastest growing sectors of the economy. In Melbourne, a billion dollar new cancer hospital is being built, for example. That’s not in the stats. Further reason to hope.