This series started yesterday when I started wondering about the exact reason we needed economic growth to keep the unemployment rate down.

I wrote an introductory post then, explaining I was going to do some learning in public. (The risk of embarrassing myself is real). Now I want to dive into this a bit more.

It’s true we need economic growth to prevent the unemployment rate rising. I checked and important people believe it.

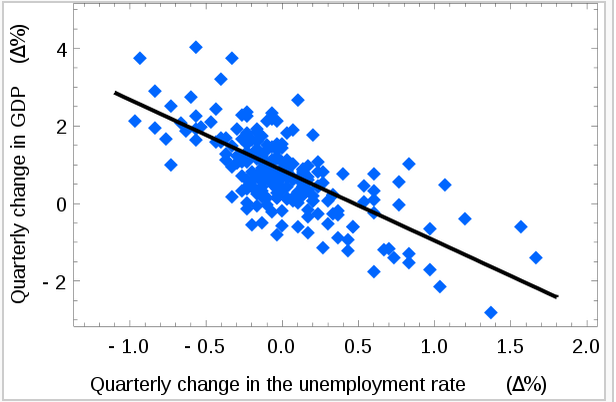

RBA Assistant Governor Chris Kent has specifically linked changes unemployment to trend growth. “Since about mid 2012, Australia’s GDP growth has been a bit below trend and so the unemployment rate has been rising gradually.”

And he has given us this excellent graph:

Phew! That’s one thing I got right.

The link between economic growth and changes in unemployment is real and it has been formalised in a relationship called Okun’s Law.

I put the word out on Twitter for an explanation and I was swamped with awesome economists offering helpful explanations. Thanks to everybody.

I put the word out on Twitter for an explanation and I was swamped with awesome economists offering helpful explanations. Thanks to everybody.

@RHTGreen@jasemurphy Arithmetically, you’ll need enough to keep up with growth in the labour force and technological progress.

— Jim Savage (@khakieconomist) September 9, 2015

This was the main thing I heard. Basically:

- Because of population growth you need growth in output to have jobs for the new people.

- Because of labour productivity changes (people getting more efficient) you need more output or else you’ll employ fewer people.

This is a nice neat story. If you have 2 per cent labour force growth and 1 per cent productivity gains, you need 3 per cent growth. It’s mathematically sound. I learned something.

So is that it? Are we wrapped up? All silent?

I still find myself with questions. I want to understand things in more than just mathematical terms.

Productivity causes growth. It allows us to produce more, using the same. But we also need growth to compensate for it? This sends me into something of a chicken and egg loop.

I’m aware that chicken/egg scenario is why economics uses maths so much. Supply and demand need to be solved simultaneously. You can’t think through a market equilibrium slowly because you need an answer on both sides at once.

So I could stop here. But I have other questions.

If rising labour productivity is both cause and cure for unemployment, why is it spoken of in exclusively glowing terms? Would we not be as well off, in unemployment terms, without it?

And population growth causes economic growth too. This is what I believe, a belief reflected in articles like these:

Fewer people want to live in Australia in growth risk for RBA

RBA’s Glenn Stevens: Australia may need to rethink growth

If we did not have the population growth, would we still have stable unemployment? This remains my sticking point – my reason for wondering about the deeper reasons and implications of why we need 3 per cent growth.

Seems to me an important part of the existing population is employed creating space for the new population to live in.

While the productivity angle makes sense to me, the population one still gives me pause. Establishing the new capital stock to accommodate the lives of new babies and new migrants is a huge cause of economic activity. More roads, more shops for them to shop in, more buildings for them to live in, more pipes going to their houses, more hospitals for them to be sick in, etc.

New population consumes and works the same as the existing population; but also requires extra spending. I intuitively believe population growth causes a rise in employment so I can’t quite grasp that it’s a wash, unemployment wise.

Whenever I think about this question I think about Japan, where capital is being abandoned as the population shrinks, and (while unemployment is low) secure employment is a problem.

Perhaps I need to think about this differently? Perhaps I need some more empirical evidence? I’ll dive deeper and present what I find tomorrow.

If you have any thoughts on this topic or want to suggest some reading, please feel free to make a comment below.