Sample size requirements are totally counter intuitive. I remember my statistics professor mathematically demonstrating to us the relationship between sample size and population size. Our minds were boggled.

For your personal enbogglement, I’ve charted that relationship here. It shows the sample size needed to get a 1 per cent confidence interval with a 99 per cent confidence. The salient point is the flattening out at the top.

It is intuitive that if you’re enquiring about a big population, you need a big sample. Intuitive, but wrong.

Once you’re surveying a population of more than 500,000, there’s scarcely any need to increase your sample size. Sampling more than 16,000 people out of a large population means adding very little value. This is good news. It means our society’s reliance on survey data – for everything from who should be PM to how peanut butter should taste – is efficient.

So why do we run censuses? Partly because the Census Act 1905 compels us to, every five years. Partly because we always have, and partly because the UN encourages us to.

But does the census get localised data effectively?

If you’re interested in small, remote, unusual communities that you will never otherwise survey, do you really want to ask them the same few questions that are appropriate for everyone else? Or is that a missed opportunity?

Instead of the census, we could ask small communities specific and relevant questions. In remote aboriginal communities, it might not make sense to ask people about their journey to work, but it might make more sense to ask for example about what they eat, which the census does not do.

I love the ABS, and I cherish this mug I got on the day of the release of the 2011 census.

I do not – DO NOT – support cutting the budget of the ABS to do their important day to day work. But I can see why running a census every five years might seem like a waste of resources that would be better used supporting that work.

The best reason to axe the census would be that it adds little empirical exactitude when obtaining estimates of the great homogenous mass of us, and is too blunt to ask the questions that matter of the smaller communities it covers.

Sachs – who made history by becoming a Harvard Professor at age 28 – is a heavyweight in the field of economic development, so it’s worth listening when he writes “technological progress can be immiserating.”

The paper acknowledges that such predictions have been made before, and proved wrong. There were some details in the history of Ludditism that I didn’t know, particularly the role of the state in defending novel production methods.

“Concern about the downside to new technology dates at least to Ned Ludd’s destruction of two stocking frames in 1779 near Leichester, England. Ludd, a weaver, was whipped for indolence before taking revenge on the machines. Popular myth has Ludd escaping to Sherwood Forest to organize secret raids on industrial machinery, albeit with no Maid Marian. More than three decades later – in 1812, 150 armed workers – self-named Luddites – marched on a textile mill in Huddersfield, England to smash equipment. The British army promptly killed or executed 19 of their number. Later that year the British Parliament passed The Destruction of Stocking Frames, etc. Act, authorizing death for vandalizing machines. Nonetheless, Luddite rioting continued for several years, eventuating in 70 hangings.”

The model constructed by Sachs and his co-authors has no role for hangings. It simplifies the economy into a technology sector producing “goods” and a residual sector staffed by humans, producing “services.”

The model tries to answer the question:

“Will the reduction in the cost of goods produced by more advanced robots compensate workers for the lower wages?”

The team runs the models several times and gets a range of different answers depending on assumptions. But the news is certainly not all good.

“A second prediction of our model is a decline, over time, in labor’s share of national income.”

The model has ‘retention of code’ as a central feature. They argue that over time, useful code builds up so that new code is less and less necessary, leaving less and less work for people engaged in its production.

Code is defined as “not just software but, more generally, rules and instructions for generating output from capital.”

It assumes over time code becomes more durable, driving unwanted “high tech workers” to go and work in the services space, where they drive down wages.

“The price of services peaks and then declines thanks to the return of high-tech workers to the sector. This puts downward pressure on low-tech workers’ wages and, depending on the complementarity of the two inputs in producing services, low-tech workers may also see their wages fall”

The ‘retention of code’ is a key feature of the model. When the researchers ramp up the coefficient on that, the model has gloomier and gloomier predictions.

The mechanism by which this works is because each more poorly compensated generation can add less and less to the economy’s capital stock:

“The long run in such cases is no techno-utopia. Yes, code is abundant. But capital is dear. And yes, everyone is fully employed. But no one is earning very much. Consequently, there is too little capacity to buy one of the two things, in addition to current consumption, that today’s smart machines (our model’s non-human dependent good production process) produce, namely next period’s capital stock. In short, when smart machines replace people, they eventually bite the hands of those that finance them.”

But is code different to any stock of knowledge? Humans have invented designs for thousands of perfectly functional cars, yet there’s work being done on inventing new and better ones at a fantastic rate. Computer code may accumulate, but “rules and instructions for generating output from capital” sounds like management. I don’t see managers being replaced by computers soon.

Nevertheless, the paper adds to the rich debate over what might happen in an economy where humans are not directly engaged in the tasks most important for their survival.

I’ll leave you with the working paper’s dystopian predictions:

“Will smart machines, which are rapidly replacing workers in a wide range of jobs, produce economic misery or prosperity? Our two-period, OLG model admits both outcomes. But it does firmly predict three things – a long-run decline in labor share of income (which appears underway in OECD members), techbooms followed by tech-busts, and a growing dependency of current output on past software investment.”

“Our simple model illustrates the range of things that smart machines can do for us and to us. Its central message is disturbing. Absent appropriate fiscal policy that redistributes from winners to losers, smart machines can mean long-term misery for all.”

When countries go into debt, they don’ reach for the credit card. They reach for bonds. By selling bonds, a country gets a stack of cash it can spend, and all it has to do is pay back those bonds in the future.

A lot of countries have a lot of debt, the global bond market is active. People don’t just hang onto the bonds they bought from governments. They’re traded. The price of the bit of paper goes up and down even though the amount it entitles you to stays the same.

“Treasury notes (or T-notes) mature in two to ten years, have a coupon payment every six months, and have denominations of $1,000. In the basic transaction, one buys a $1,000 T-Note for $950, collects interest of 3% per year over 10 years, which comes to $30 yearly, and at the end of the 10 years cashes it in for $1000. So, $950 over the course of 10 years becomes $1300.”

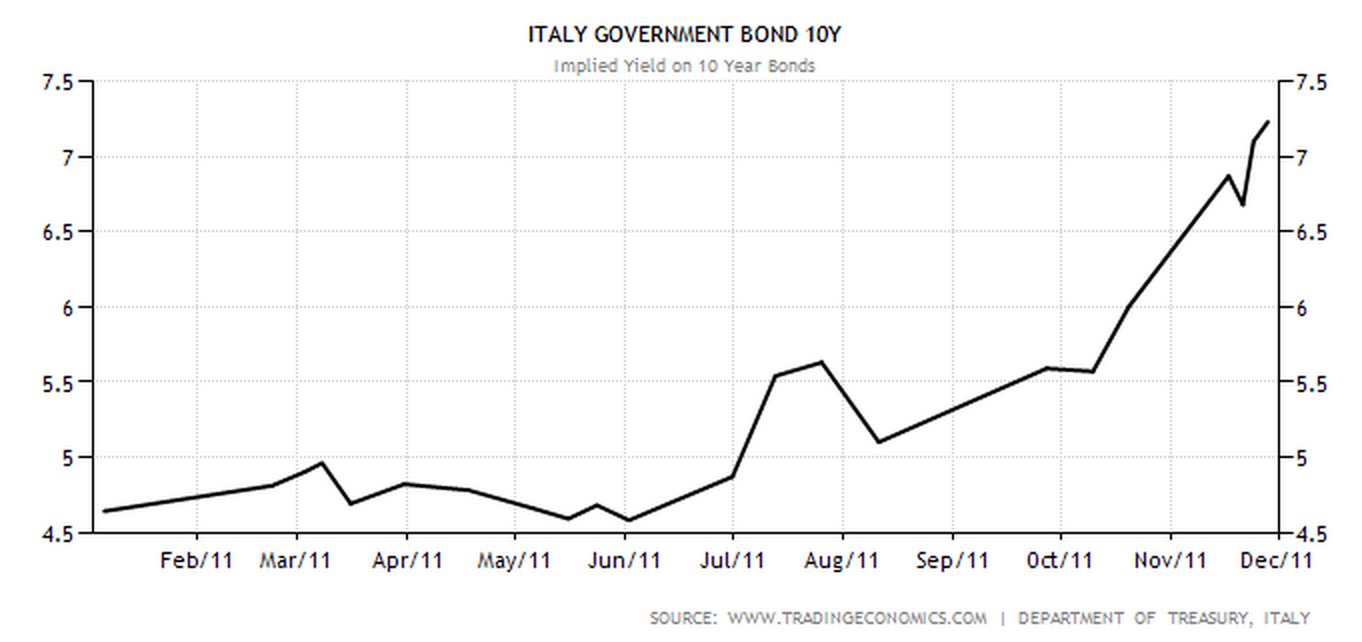

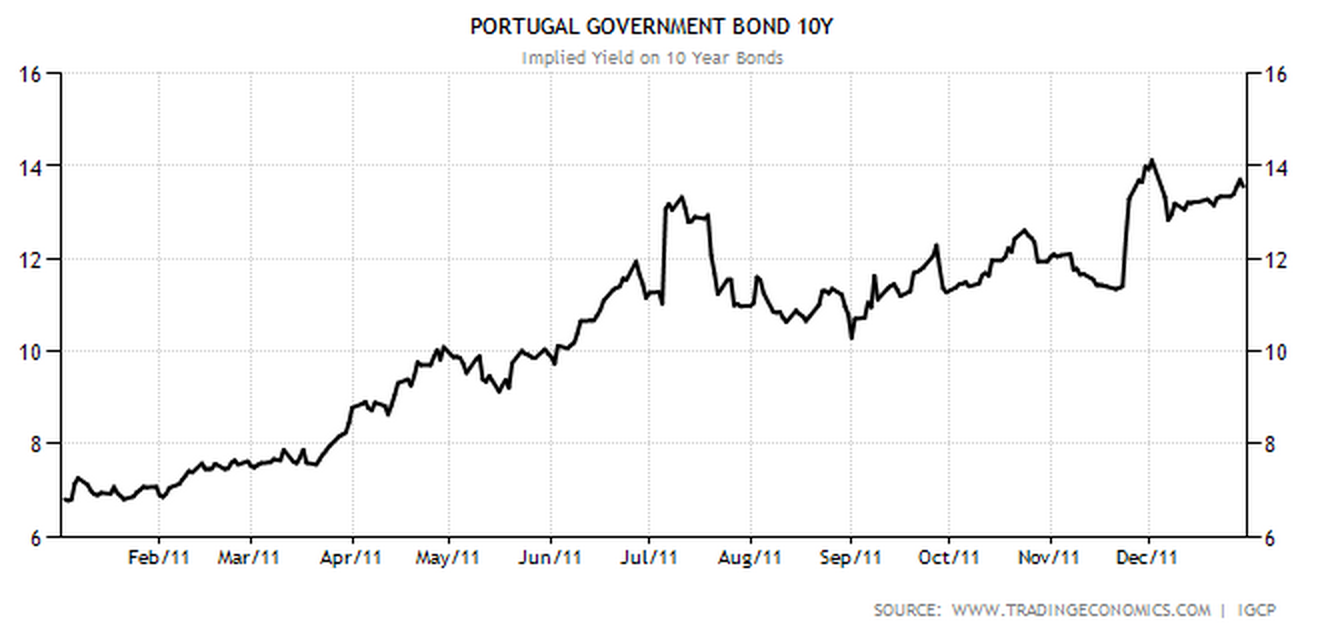

Some people find bonds to be a very good investment and they are also closely watched as markers of trouble. When it looked like Greece was going to be kicked out of the eurozone, its bond yields shot through the roof. (Bond yields are the inverse of the market price. If you pay $1000 for the bond described above, your yield is zero (assuming inflation of 3 per cent).) In 2011, everyone was selling Greek bonds and buyers were few.

In late 2011 if you bought a Greek government bond you were brave or crazy. Its yield was 40 per cent, implying people were worried the government would not honour it. Source: Trading Economics

Those high yields said nobody wanted to buy Greek bonds. Or Portuguese, or Italian.

Bonds work a bit like a stock. There’s always something to worry about.

When yields are up and price is down, it’s because people think that entity is going to go broke. When yields are down and prices are up, people start to worry that the price has overshot and might suffer a damaging correction.

Overall, riskier countries have lower bond prices and higher yields. For example, Japan’s bonds cost a lot, and yield just 0.4 per cent, because that nation is believed to be trustworthy and reputable.

But suddenly, the whole bond market is looking more Japanese, and that should rouse suspicion.

Bonds are a hot topic because of plunging yields in the last few years.

Does anybody really believe all the risk has gone out of these countries? Does it really make sense that Spain can borrow money at under 2 per cent? I think I’m less of a credit risk than Spain (unemployment 24 per cent) and my credit card company charges 10.99%.

What we may be looking at here is a bubble. All these bonds are in hot demand. But what happens if the bubble pops? The people that hold them lose money. That includes central banks, hedge funds, private investors, superannuation funds and banks. Any of whom could upset financial stability.

The reason this topic is hot is that a sharp object has come over the horizon that could burst the bubble. A rise in US official interest rates.

It seems likely that the US will start raising interest rates in the next few months, given their strong recent economic performance. (This is the view of the RBA Governor, at least). If outlooks for the US economy and global economy are better, a rate rise could coincide with investors deciding they’ve had enough of boring safe bonds, and getting back into stocks. That would see bonds being sold off.

The Governor of the Reserve Bank is expecting such an event, he has just revealed in testimony this morning to the House of Representative Economics Committee.

Stevens on whether we’re in a bond bubble; “It’s a very strange world in which we live…at some point one would expect this would reverse.”

The size of the global bond market is big enough that a sharp crash would hurt the financial system. And we’ve all learned that crashes in the financial system hurt the real economy soon enough.

It got me thinking about how I used to attend the Defence Property Interdepartmental Committee back in 2005 and 2006 and all the arguments that used to rage about shutting down the Australian Defence Force’s many under-utilised golf courses. (link for context)

But it made me think about the efficiency of golf as a sport. It’s not easy to understand how golf courses make money in cities. Golf seems extremely land-intensive.

I wondered how it compared to other sports.

Golf is by far the worst of the lot. I calculated this by assuming four players per hole on an 18 hole course, and applying US golf association rules on the recommended minimum area for a golf course, of 60 hectares.

The question of the land-intensity of sports is – perhaps surprisingly – something I have thought about often. But never before had I bothered to graph it. The reason I’ve pondered it is because of some tennis courts near my house that are used as netball courts on weeknights. As tennis courts, they are lightly used, but when it’s netball night they are brimming with noise and excitement and there are cars parked for miles around.

In the courts at right, you can see the netball court (yellow lines) encompassing the tennis court (white lines)

Even though the courts are used for netball only a few hours a week, these courts probably mean netball to more people than tennis.

The land intensity of sports is a pretty important question for governments trying to make participation in sports accessible, cheap and convenient as the density of our cities rises. When you have to rent space to play on, it makes sense for that space to be minimal.

Here’s another chart, with a truncated vertical axis to show the most efficient sports in more detail. Tennis has a few different entries, because I first measured it on tennis court area, but then, after I added table tennis, I realised I needed to count the recommended area for playing, not just the court area. This means the numbers are not perfectly comparable (I haven’t added areas outside the boundary lines for rugby or cricket or soccer)

Seemingly, the most efficient sport on the graph is table tennis, counting two players and a table of 4.18 square metres. But that’s not realistic. Players don’t stand on the table. The most realistic actual entry is pool, which two players can enjoy in 18 square metres, assuming a standard 8-foot table. (I guess that’s why there’s pool tables in pubs, not basketball courts.)

The most land efficient sport in which you would plausibly break a sweat (or break an ankle) is squash. Squash I seem to remember being popular in the 1980s. My dad used to play when he was a lot younger. I’m not sure why it fell from favour, but perhaps Donald Rumsfeld’s enthusiasm for it has something to do with it. Anyway, on a squash court, two adults can do serious work on their heart health in just 62 square metres, making it a sport that is ripe for a comeback in the ever more crowded 21st century. (nb. this doesn’t calculate three dimensional area, and squash courts are tall).

Cricket, meanwhile, comes out of this looking rather bad. My calculations use 17,000 square metres as the size of the field, which is the approximate area of the SCG. Leaving half the players on the sideline is what really ruins cricket’s numbers, because at any time there are only 13 players actually playing. It’s almost as bad as golf. AFL, which uses the exact same fields as cricket, manages to put almost 3 times as many bodies into the same space.

Mr Hockey insisted the government would press on with a stringent Budget full of cuts. He bemoaned the total government debt and the legacy current generations are leaving behind. His catchphrase of choice with respect to cuts was this:

“We have no choice!”

But the loudest message was that he had not fully understood the events of recent weeks. He appears to think that the Government’s problems are all about Tony Abbott, because he insisted that all he needed to do was better explain his policy choices to the electorate.

Of the two – Abbott and Hockey – it is Abbott who got closest to the fire and Abbott who has learned the most. Abbott has spoken about listening more, to both the public and the party room. Mr Hockey may think that is yet more spin. But I doubt it is. The 2015 Budget is going to be designed with a lot less guidance from Hayek and a lot more from Roy Morgan. The problem is that Joe Hockey doesn’t realise that yet.

So Mr Hockey is going to have to adapt. Adapt or perish. If and when he adapts, in some small part of his being he may wish he’d been rolled as Treasurer on Monday.

But in his 730 Report interview he said several times “the customer is always right.” Let’s generously assume that motto means he can and will adapt.

So what will he do in this new, constrained environment where ideology is out and the Budget is worse than it has been for a long time?

If commodity export prices keep falling, Hockey could beat Wayne Swan’s record of highest Budget deficit ever ($54.5 billion in 2009-10.)

The new, chastened, post-realisation Mr Hockey will be faced with a set of unenviable choices. He can let the deficit blow out, he can cut spending, or he can raise more revenue.

The most unenviable part of his dilemma is that he will probably have to do all three. Suffer the ignominy of a great big budget deficit, trample all over his own principles by raising taxes, and risk the wrath of the electorate by making more cuts.

Mr Hockey’s task in the next few months is to make this something other than a political suicide note.

After surprising the hell out of the electorate with his first budget, he won’t be allowed make the same mistake again. You can be pretty sure that the key ideas in the document to be released on the second Tuesday in May will have been given a thorough airing.

Cuts will be thin on the ground. Reinforcing the message that the Coalition slashes and burns will not be welcome in the party room. That leaves a gaping hole of a deficit.

Unless he can somehow arrange to include tax increases. If he wants to stop the deficit increasing, Hockey’s best option is to look at tax expenditures. You can cut tax expenditures and simultaneously claim you are not levying new taxes. (A tax expenditure is just a big exemption to tax, so cutting a tax expenditure raises more revenue.)

As you can see, the numbers involved are real. Many many billions. GST and the family home are probably no go areas. But some of these tax expenditures – on superannuation and capital gains – overwhelmingly help the Coalition’s older, richer, higher marginal tax rate base.

Politically, removing or changing them may be the best option, because the Government has lost the centre, and needs to regain it. Tax hikes that hurt working families will be off the agenda in 2015.

The average price for a home in this country is now $571,500. We hear a lot about the homes at the top end of the distribution, places that cost 100 times as much as the mean, like this Mosman Park pile for $57.5 million.

We don’t hear so much about the other end. There must be houses in this country that cost a lot less than the mean. I went looking for them.

This place in outback NSW costs $40,000.

You could imagine living there, stepping out onto the verandah with a cup of Bushell’s tea as the sun rises through the eucalypts, thinking: I made a good choice.

This is a country of extremes – not just of drought and flooding rains, but of wealth and poverty. It’s easy sometimes to forget about the poverty. I’m somewhat ashamed to have started writing this post thinking only of the amusement value of a cheap house, and not at all about the conditions that explain it.

As well as getting excited by optimal stop spacing, one thing people in these circles agree on is that roads are bad. The most common argument made against roads goes like this:

“Essentially, if you widen roads to reduce congestion, people who were avoiding the road because of congestion will find it more convenient and take more trips, thus increasing traffic again.

So what do you have then? A big expensive project to eliminate traffic, and more traffic.” Streetsblog

“New roads will create new drivers, resulting in the intensity of traffic staying the same.

Mann explains how this counterintuitive reality can possibly be true: “As it turns out, we humans love moving around. And if you expand people’s ability to travel, they will do it more, living farther away from where they work and therefore being forced to drive into town. Making driving easier also means that people take more trips in the car than they otherwise would.” Planetizen

“Research indicates that generated traffic often fills a significant portion of capacity added to congested urban road. Generated traffic has three implications for transport planning. First, it reduces the congestion reduction benefits of road capacity expansion. Second, it increases many external costs. Third, it provides relatively small user benefits because it consists of vehicle travel that consumers are most willing to forego when their costs increase.” Victoria Transport Policy Institute

While I support many of the ideas this argument is rolled out to support, I find the argument itself utterly unconvincing. If you want to argue against investing in roads, you’ll need a better argument. Here’s why.

1. Public Transport will behave exactly the same.

If you widen a road, it will encourage more people to drive on it, bringing congestion to an equilibrium level* on that road, and spilling congestion into other parts of the network.

Likewise, if you increase the frequency with which a public transport service runs, it will attract more people to ride on it, bringing congestion to an equilibrium level and spilling congestion into other parts of the network.

This means that induced demand operates as an argument not to invest in any popular/crowded transport where crowding levels may be deterring travel. I’m not sure that’s what proponents of the induced demand argument intend.

*The equilibrium level is not necessarily the same amount of congestion as before, it’s the level where congestion deters travel.

2. Induced demand is good.

Induced demand means previously people had latent demand for travel, but they were unable to satisfy it. Now they are able to access jobs, get to shops that sell items that match their needs better, visit friends and family more. Any argument about transport investment that objects to people doing more travel should be treated with suspicion, if not contempt.

3. Focusing on congestion is the wrong way to look at transport policy.

If your approach to solving a city’s transport problem is to seek out choke points and jams and try to untangle them, you may end up fighting unwinnable battles against geometric problems. You will become frustrated, growing ever more sure that transport is a zero sum game with no easy answers.

But the answer is not necessarily eliminating every queue – there are planners who believe congestion is perfectly acceptable, a sign of popularity and even of success. (1, 2, 3,)

Forget congestion. If you make your yardstick access, you focus on what people want: What places can I get to?

A rational approach to transport planning in a city would be to measure access: From each address, a sum of all the jobs, services and other addresses that can be accessed, averaged across a time period encompassing peak and off-peak.

That number would be aggregated across the entire city to create a total score. Then, you would provide incentives for bureaucrats to improve that number. These bureaucrats must have more than just transport levers at their disposal.

They should also be able to make decisions on zoning and land-use, and road pricing. Improving access can as easily mean moving jobs to people as people to jobs. If a particular investment is expected to have spill over effects that worsen transport times in a far-flung part of the network, the access measure should pick this up and permit that effect to be compared to its positive local effect.

Build a new school, access improves. Add traffic light priority for buses, access improves for some at the expense of others. Price a road, access improves for high-value trips at the expense of lower value trips. Add a new lane on a freeway, access improves locally and probably diminishes elsewhere.

Focusing on access allows trade-offs and comparisons to be made. But often, improved access will involve turning latent demand for travel into real trips. We shouldn’t object too loudly to that.

The point of a city is that people want access to other people, and services. Let them at them.

The government of the state where this blog is produced is in a pickle.

Prior to an election last November the then Opposition promised to cancel or defeat in court a contract for a big controversial road tunnel. The tunnel, worth perhaps $6 to $10 billion dollars, has not been built yet. Nothing beyond planning has commenced

Now the former Opposition are in power, they are finding that the old government left them a poison pill.

If the road is not built for any reason, the government must pay the company that would have built it $1.1 billion. This clause was added by the previous government. The companies might have done only $50 million of preparatory work – being generous here – but they get paid $1.1 billion simply for missing out on finishing the job.

Ignoring for a moment the morality of inserting such a clause into a contract (it’s vile, wasteful, ridiculous, and would in a better world result in a range of senior bureaucrats and politicians going to jail), we turn our minds to how the present government can deal with it.

There are three main options.

1. Avoid the payment and make the road. This would involve reneging on a major election promise, but you don’t waste the money.

2. Avoid the road and make the payment. This would gift a billion dollars from an indebted state government to a consortium of companies including Lend Lease Group, worth $9 billion, Acciona, worth €3.6 billion and Bouygues SA, worth €10 billion. It would probably be politically convenient too.

3. Avoid both the road and the payment. The government has one big advantage. It makes laws. It can write legislation that annuls the offending contract. But the big risk in such a course of action is that it establishes an extremely unwelcome precedent that promised payments can be cancelled at whim by the government, and valid questions being raised about sovereign risk.

I want to look more closely at option three. Is there a way a law could be drafted that gets a just result and avoids sovereign risk? I think there might be.

Any law to cancel the payment provisions in the east-west link should:

1. Make it clear that this is a once-off by raising the hurdle for ever cancelling this kind of contract again.

For example, the Government could include a clause requiring that in future passing legislation that annuls any contract above a multi-billion dollar value threshold requires a supermajority in parliament, e.g. two-thirds of votes. The requirement for a super-majority should not apply to contracts where the cancellation provisions are substantially greater than the cost of the work done.

Sovereign risk only applies if a company can genuinely fear its contract provisions may be changed by legislative fiat. If they fear risk, they will raise prices.

Reducing the risk of such legislative action should attenuate the real costs of sovereign risk (although it won’t prevent the political costs of big companies mouthing off about it.)

2. Legislate against any future government ever introducing “poison pill” contract clauses into infrastructure contracts. (Part of me wonders if this law could apply retrospectively?)

3. Legislate that any large contract signed during the “caretaker period” in the lead-up to an election should be agreed upon by the leader of the Opposition as well as the Government, in order to prevent sneaky surprises. Part of the problem with the east-west link project was that it was never an election pledge, was controversial for 3.5 years, and with weeks before the election it looked set to lose, the government signed a contract.

We’re in a tangled mess.

Now. Could the state government of Victoria pass such legislation? It has a lower house majority, so it could pass it there, no problem. In the Upper house it holds just 14 of 40 seats. But The Greens have five, and they are likely to support such a plan. Then the government needs just a couple more, drawn from The Democratic Labour Party, the Sex Party, Shooters and Fishers, and Vote 1 Local Jobs. It might require some side promises, but it may be possible.

I welcome your thoughts and comments on this idea. Please leave a comment below, or hit me up on Twitter.

“(12) Chevron have released a presentation for their investors … which indicates an expectation that 40% of the “new oil” will come from deepwater fields, 20% from U.S. shale, 10% from increased tar-sands production, 25% from OPEC growth (Venezuelan extra-heavy oil?), and around 5% each from shale outside of the U.S. (Russia?) and “onshore and shallow offshore”.

(13) Chevron also stress that production from these sources will not come cheap, and will probably be of the order of $100 a barrel (“Breakeven price” or “marginal cost”).

(14) Hence at under $50 a barrel selling price, these projects will not go ahead, or they will be money-losers (cost more to produce the oil than it sells for). This year, $150 billion worth of new projects may face the axe, which are mainly from heavy-oil, deepwater, tar-sands and shale-oil.”

I think this analysis looks sound as far as it goes, but it doesn’t address two big issues.

1. What OPEC might do next.

Although oil prices had fallen around 30 percent before the seismic November meeting in Vienna, the cartel is the reason behind much of the oil price crash. Will they regroup? Or is this the end of any and all caps on production, and might the oil price sink further.

2. Demand.

Talking about a market from only one side, as though demand was limitless, is as silly as assuming supply is limitless.

Peak oil appeals as a theory because it is self-evidently true. Oil really is non-renewable, and we use a lot of it. There will be a single day on which more non-renewable hydrocarbons are extracted from the earth than any day before or after. That day is the peak of production.

But – Peak oil is a hot topic, and despite debates about the accuracy of reserve estimation techniques, it’s not because of the physics of reserves. Peak oil matters because of the assumption it is going to be a problem.

Really, peak oil is not about oil. It’s about whether we can adapt. It’s about how we manage demand. That’s a question about the operation of markets, about the functioning of governments, about technology. About action guided by markets and action guided by collective planning. And that, in my opinion, is far more interesting.

The main assumption regarding demand is that oil consumption rises as the world grows richer.

This is the unstated fact behind the implication that peak oil is a catastrophe. Rising demand has been true for a long time. But need it always be true? Sometimes long-standing trends defy extrapolation.

There may be a few reasons to start thinking about peak oil from a demand perspective. Here are three.

But the relationship is not simple across countries, with very poor countries using very little energy and some rich countries using a lot

It’s possible to see the above curve as a Kuznets curve lying on its side. (I’ve written about Kuznets curves before in a very different context). Very poor countries and very advanced ones are more efficient. Middle income countries (and freezing cold Canada) are worst. If the most populous countries continue to develop, oil demand could shift.

2. Technology is crucial. Obviously, high prices drive the adoption of energy efficient practices, which is one reason why the Toyota Prius sold so well in the last ten years of high oil prices, and cars that get 13.3L/100km, like the one below, did not.

If oil prices stay low, that will be because those technologies – electric cars, solar power, biofuels – are having their effect. But oil prices will probably go back up ( in fact they already have bounced a little). If that happens, households and companies will regain motivation to adopt technologies to conserve usage, and we will probably be having these debates about when peak oil will occur in another hundred years.

3. Climate change. We may see peak oil happen long before we’ve used up half the world’s known reserves. Moving carbon from beneath the earth’s crust to its atmosphere produces externalities that could, any moment now, become so obvious that they drive a political consensus to leave the carbon beneath the surface, where it is relatively safe.

I was wandering up to the entrance at Melbourne airport late last year when three members of the Rebels motorcycle gang arrived at the terminal.

Approaching the sliding doors at the exact same time as these three large, black-clad, sunburned men, I realised I would either have to slow down or speed up to avoid bumping shoulders.

I went to speed up, then, remembering the news about bikies killing someone at an airport a couple of years ago, I suddenly reversed my decision. I might just keep my eye on this lot, I thought, and let them through first.

What happened next?

They passed through security and I later saw them sitting near the gate. Like any other Australian, a bikie sometimes needs to travel by air.

Flying is a regular part of life for most of us. I doubt there is anyone reading this blog who hasn’t held a boarding pass in their hand in the last year. It’s a convenience, but it’s also a pain. All that waiting, the tiny seats, the way food tray is so crowded with things and hard to manage. It’s easy to forget that most people in the world have still never flown in a plane.

That fact made me wondered if I could quantify Australia’s tendency to fly.

It turns out Australia is in the top 10 countries globally for passenger movement, according to World Bank data. (The World Bank uses domestic and international aircraft passengers of air carriers registered in the country, which is a fair proxy in the case of some nations, and not for some others).

When you look at the data, you could easily conclude that Australians fly more than the citizens of any other country.

This chart uses that World Bank data to show domestic and international flights for the most flying-oriented countries, plus a few others for comparison. Nine countries score higher than Australia on this metric

When you look at the chart, it makes sense. The countries with the most flights per capita are islands. They are also often small countries where there’s nowhere else to go except to fly out. Several of them are tourist destinations or aviation hubs. (nb. Ireland and Antigua probably top the list because of their tax status (and RyanAir), not their proclivity for flying. The Irish statistical office claims only 22 million international flights) .

The countries above may also top the flights per capita listing because they are small. Australia is more than double the size of any country above it on the list (UAE, home to Emirates airlines, has 9 million inhabitants.)

Given all this, I am prepared to say Australians probably fly more than citizens of any other nation.

(The data from our own statistical agencies show the World Bank figures may underestimate the amount of flying. According to BITRE, Australia has 57 million domestic passengers a year and 23 million people, making 2.5 domestic flights per capita per year. Add in 33 million international passenger movements and the data suggest more than three flights per person per year – closer to 3.5. New Zealand may also be a contender for the flying-est nation, but its numbers are swollen by high inbound tourism, while Australia sees more departures than arrivals and a higher share of domestic travel.)

So Australians probably fly the most! We head to the airport as often as every three months. Woo-hoo?

I didn’t think so.

Meanwhile, at the other end of the scale, Indian nationals rack up on average one flight every 20 years. That’s less than Kenyans, but slightly more than the Cambodians.

What would happen if Indians started flying more? Such a densely populated country will probably never fly as much as Aussies do, but what if they flew at the same rate as the Americans, 2.35 trips a year?

Those extra planes are going to need somewhere to land as well. What cities in the world have space for more runways?

China has already increased its appetite for flying tenfold. From 35 million flights a year in 1994, it has increased to 350 million by 2014. The lesson is this – economic growth sends people to the airports, for business and for leisure.

India’s economy grew at 5 per cent per year. At that rate it won’t be a “rich” nation for perhaps a century. But in 2010 it grew at 10 per cent, and if – like China – its growth rate can be held high, then it can become very rich very fast.

If everybody in India can afford to fly – even the bikies – its worth asking the question of whether the world is ready for the consequences.

“Overall, the Bank’s assessment is that output growth will probably remain a little below trend for somewhat longer, and the rate of unemployment peak a little higher, than earlier expected.”

So could option c) be the answer? They’ve found a way to contain housing risks?

It was only yesterday that Prime Minister Tony Abbott made a very public announcement about a crackdown on foreign investment in real estate.

“I am a friend of foreign investment but it has to come on our terms and for our benefit. The government will shortly put in place better scrutiny and reporting of foreign purchases of agricultural land and better enforcement of the rules against foreign purchases of existing homes so that young people are not priced out of the market.”

It was hard to process that announcement at the time, being bereft of context and detail. There had already been a crackdown announced. Was this new approach to have a louder crack, or push further down? It was a mystery.

Until the RBA rate cut.

I hadn’t though of a linkage here until I saw the question posed on Reddit. The person who asked the question in that forum sees causation running the other way, with an interest rate cut necessary to accommodate the deflationary effect of the crackdown.

But we know that the order in which things are revealed does not necessary accord with causation. Assuming so is to fall victim to the simplest kind of fallacy: post hoc ergo propter hoc.

The RBA may be betting that keeping Chinese money out of the market will help keep a lid on things.

Will that work? It might. Foreign investment represents only a tiny share of our market. But introductory economics textbooks tell you, economists think at the margin. A few extra bidders for a house can be what pushes the price of that house through the roof.

Think about it like this: if there 100 seat in lifeboats and the ship is sinking, the price of lifeboats will be zero if there are 99 passengers, and start to rise very rapidly if there are 101. The marginal bidder is important.

Last year, the RBA left rates on hold. Despite increasing unemployment and modest inflation, the bank decided that “a period of stability” was the best course for interest rates.

At the December meeting of the RBA board, they seemed calm. The statement released said

“…most data are consistent with moderate growth in the economy……. monetary policy is appropriately configured. … the most prudent course is likely to be a period of stability in interest rates.”

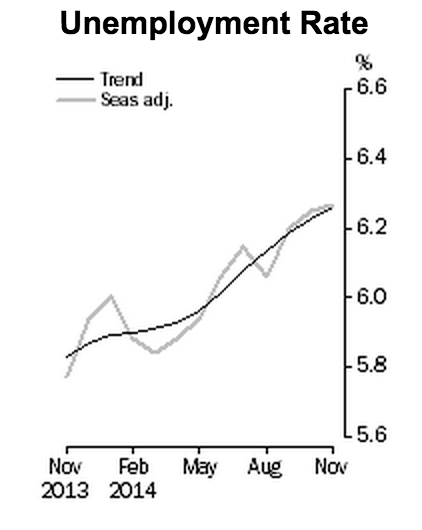

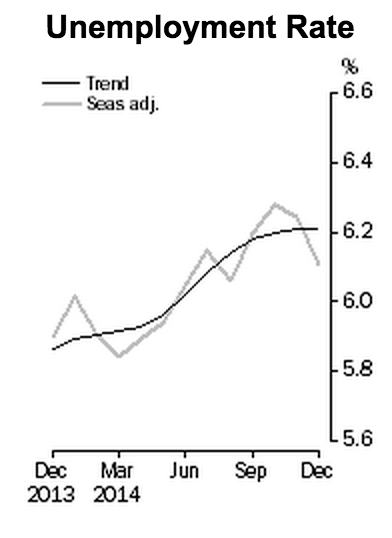

But the meeting was followed the very next day by the release of the National Accounts which showed “dreadful” growth in the quarter, of 0.3 per cent. And shortly thereafter, unemployment figures came out looking like a horror show. Trend and seasonally adjusted measures converged on 6.3 per cent. A record high.

The bank suddenly seemed perturbed. In an interview published by the AFR on 12 December, the Governor said:

“…if at some point we can be more helpful for confidence by doing something different, then obviously that will be on the table, and we will take a fresh look at all these things in the new year”

In the minutes of the meeting, released two weeks after the meeting and four days after publication of that interview, the labour market was singled out:

“…members noted that subdued labour market conditions were likely to weigh on consumption growth and consumer confidence more generally.”

So perhaps Glenn Stevens spent the long summer fretting he’d left the interest rate unchanged for too long. Perhaps he sipped light beer by the pool and bored his bbq guests by extemporising on how a two-month break between the December and February meetings was inappropriate for a modern economy. Perhaps his long summer nights were filled of dreams of a rate cut.

But then the New Year began and with it came more positive news on the economy.

Unemployment, when the December figures were released in mid-January, was suddenly much better.

November figures released in December.December figures released in January. (note, for all the fans of the trend line, how it moves in several periods on the release of new data. The seeming predictive power of the trend line is achieved via retrofitting!)

At the same time, the Aussie dollar went into freefall. It has gone from US85c at the time of the December meeting to just under US78c today. (under seventy-eight?! oh my god this upcoming American trip is going to kill me.) The speed at which the economy can expand is affected not only by interest rates but also the exchange rate, which are lumped together under the terminology “monetary conditions.”

The lower exchange rate boosts the economy in several ways. Both by making imports less competitive, and by making it easier to export. It should also reverse the enormous disparity between the number of Aussies who go offshore and the number of tourists who arrive. (A lower exchange rate is not without costs, of course, as many goods, especially capital equipment, is imported).

In all these ways, a lower exchange rate does the same work as a rate cut, all without Mr Stevens lifting a finger. Best of all, the lower exchange rate should not lead to higher house prices, which is very welcome as bubbles remain a topic of great importance to the RBA.

Last but probably not least, the falling oil price is going to put stacks of cash in consumer pockets. I filled up the car with glee the other day. Unlike falling interest rates, which rob from savers to give to borrowers, lower oil prices are pure upside for consumer buying power, and therefore a more powerful spur to consumer confidence.

That same PDF, authored by Westpac, predicts two rate cuts this year. But is that really going to happen? For that to come about, the bank would need to have changed.

Inflation was not a major concern and probably won’t be so long as the falling dollar is pushing average prices up, cancelling out the falling oil price.

The bank’s two big worries have been the housing market and the unemployment rate. With house prices still rising at the end of last year, it must surely be frightened of a 2015 full of headlines featuring a median house price nearing $1 million in Sydney. And unemployment looks like easing.

I bet the RBA will leave rates on hold again.

But the one thing that sticks in my mind is this article in the Herald Sun. Business Editor Terry McCrann has a long report on why the RBA will cut interest rates. It is specific enough and well-researched enough to appear to be a leak rather than (like this piece) the author’s own ideas.

McCrann writes:

“The RBA will be reducing both its growth and inflation forecasts in this statement [a report to be released after the board meeting]….

Critically, on (underlying) inflation, the RBA will also make its first point-forecast for June. It is likely to be 2.25 per cent, it could be as low as 2 per cent — either way, significantly, very significantly,below the 2.5 per cent midpoint of its 2-3 per cent target range.

Almost as significantly, it will cut its December forecast inflation range to 2-3 per cent and do the same for at least the first half of 2016.

In short it will be forecasting weakish growth and inflation below target. It quite simply could not release those figures on the Friday and have left its official rate unchanged on the preceding Tuesday. Or at least signalled a pending rate cut.”

If he is right and the forces pushing down on inflation are far greater than those lifting up, then you can’t help but expect a rate cut. It’s an inflation-targeting bank, after all. Tuesday will tell.

At the Australian Open, first round losers take home enough money to buy three (3) of the automobiles on offer from major sponsors Kia. They can stand on an outside court, not even touch a ball with their racquet, and still take home $34,500.

Even those who fail to qualify for the tournament itself are richly rewarded. 64 men and boys and 48 women and girls have their dreams crushed in the first round of qualifying each year. To compensate them, they get $4000 in prizes. Losing in the second round of qualifying garners you $8000 and losing in the third round nets $16,000. Not bad.

Since I found out the total prize pool at the Australian Open, I’ve been asking people to guess it. Guesses have ranged from $4 million to $12 million. None have come near the true total: $40 million.

The organisers give out prizes left and right. Every player gets something. The Aussie Nick Kygrios takes home $340,000 for making it to the quarterfinals of the men’s singles draw. But he also gets $7400 as his share of a team that lost in the first round of the doubles. (Nick is ranked 1207th in the world for doubles, suggesting that entering the doubles draw might have been about the cash, not his passion for the game.)

The prizes in the singles are greatest.

Winners’ loot.

The most expensive match of the tournament is the final, of course where the loser gets $1.55 million and the winner $3.1 million. But it is also the only round where the winner collects a cheque. In each other round the winner goes on to a chance of bigger and better things. Excluding the final, the most expensive round for organisers, at $2.1 million, is round one, where 64 losers get $34,000.

The prizes are rich enough to cover airfares and accommodation – even for the players who lose at qualifying. Research suggests 150 pros are making enough money to break even in each of the men’s and women’s game. At the same time, some up and comers are probably losing money now in the hope of gaining the experience to make it big later, and others are losing money in the twilights of their career, hanging on in hope of one more glory. (Hi Mr Hewitt!).

So, where is that money coming from?

Tennis Australia’s Annual Report shows it made $193 million last year from “events and operations.” While there’s not much detail, one can imagine that the vast bulk of that is broadcast rights to that highly rare prize, the Australian Open. Channel Seven in Australia pays $20 million a year. The rights globally are doubtless severalfold higher.

Having a grand slam is quite a feat for a country of Australia’s tennis stature. Government supports it, but the support is less direct and therefore less controversial than that provided to the Grand Prix. They prop up the Melbourne and Olympic Park trusts which run the stadiums and have put in hundreds of millions of dollars for their development and re-building. Those stadiums are used for other purposes too, many of which attract tourists from around the world, contributing to the local economy.

Sales of iPads are falling, sales of iPods are a footnote. App store sales growth is remarkably low (13%) given how fast the phone market is booming. Macs are selling steadily but in small numbers.

But the iPhone keeps on giving. In 2014 it sold 169 million units, up from 150 million in 2013. This is quite amazing. And in the first quarter of 2015 it sold a record-beating 74.5 million units. My earlier prognostications that Apple was over-priced look a bit silly now. But there are signs my enthusiasm to call an end to Apple’s rise were just a bit early.

Most of Apples 2014 revenue growth was in China, where prices are falling and entry-level iPhones are popular:

Here in the first world, I feel like the iPhone has lost its lustre. Sure enough, sales for “rest of Asia Pacific” were down by 7 per cent. Sales in the Americas rose just 4 per cent. I see my friends buying Android Phones, because they’re cheaper and just as good. Apple’s iPhone is old news.

So can Apple make itself last?

In some product categories, early market leadership can create decades of dominance. Gillette was the top brand for shaving goods 100 years ago and is still today. Ford similarly for cars. Apple first rose to prominence 30 years ago and is still going strong.

Apple’s share price (USD)

Apple is the biggest public company in the world by market value, especially since the recent oil price fall has hit its main competitor Exxon Mobil. But so much of that value rests on the iPhone.

After a certain point, a product can’t be improved much more technically, and become commoditised. Think of your flat screen TV. That product now competes on price, not features.

And Apple’s next big product launch is the watch, which I believe will bomb horribly. Apple has a big pile of cash, but as its burns through that that in pursuit of the next big thing, its share price must fall.

It suggests Mr Hockey’s insistence that Australians spend six months working for the government is a deliberate ploy to turn us against income tax, which will dovetail with an idea from the Commission of Audit:

“providing the States with access to part of the Commonwealth’s personal income tax base.”

The Commission expands on that idea like this:

“A further option to increase State source income is a combined Commonwealth-State personal income tax, which could include providing the States with a designated share of personal income tax raised, or allowing the States to levy a State income tax surcharge (with the Commonwealth ‘making room’ so that overall income tax rate need not rise).”

The first issues paper of the Federation White Paper was released just prior to Christmas (and I mean just, it came out on the 23rd of December). The amount of coverage it got was slightly less than the NORAD Santa tracking radar. Is the idea that the Abbott government going to reform our whole federation as fictional as the man in the red suit?

Maybe it’s the best idea this government has left. States spend all the money, but can’t raise enough. This is bad from an accountability perspective, and also because it diverts effort to rent-seeking. States spend time scrapping over the GST shares and the conditions on Specific Purpose Payments.

States don’t appear set to introduce a land tax, which I reckon is the only other solution. So giving them the power to raise their own income taxes is a potentially sensible move. This is a classic small-l liberal solution, allowing each state to set the income tax that best suits its needs, and also encouraging competition between jurisdictions. Vertical Fiscal Imbalance could be over!

(I’ve always thought Vertical Fiscal Imbalance was a terrible bit of terminology and it should be known as something more catchy. I quite like calling it the Federal-State Tax Mismatch.)

This could be the high-minded idea that the Coalition need to administer a shock to the electorate, to make people realise they are actually full of ideas, not just a team of cutters. If done right it could deliver positive media alongside well-liked (probably Labor) state premiers.

The only problem now is that the narrative is all but set. Mr Hockey is seen as a hardline right-wing ideologue, so even a rather sensible plan to optimise subsidiarity will likely be seen through that lens. Will Mr Hockey gamble and introduce this idea – doubtless new to many voters and potentially confused with a tax hike – in these conditions?

The man who tweeted them, Brent Toderian, is a big name in urbanism, based in Vancouver. Of course he is horrified by the way roads and cars dominate the skylines.

But I saw something in these pictures that redeemed them. I think they are possibly quite smart.

The use of apartment buildings as props for very high freeways was the main aspect that caught my eye. It would not be feasible to drop a road on top of existing buildings. But it may work where you take an existing road, build apartment buildings in its space, and then put the road on top of them.

In talking about this plan, I’m especially thinking of Hoddle Street, which is Melbourne’s Achille’s heel. A north-south road near the city that is choked with traffic almost all the time, it has been the subject of countless studies into how to improve it, with little permanent improvement..

What might work is an idea from left-field, like that illustrated by Sir Charles above.

Here are the upsides I see.

1. Urban infill.

If you take Hoddle Street and fill it with high rises that support a freeway, you get a quick bump in inner city density. Furthermore, the land belongs to the government, so they ought to be able to actually make profit on the property development.

2. Better street level traffic.

The street level near Hoddle Street is a horror story. It’s very unpleasant to walk on because of the traffic – noise, fumes, and on the occasional place where they can build up a bit of speed, the fear you’re going to be killed. The houses along Hoddle Street look cheap and poorly maintained – there is obviously a price discount for being on the road. There is very little retail and not a single cafe or shop with outdoor seating on its whole length.

If the roadway was way up in the air, (and a couple of the many many traffic lanes were retained for a more normal scale street), the street level might be a bit more comfortable for actual use. Cyclists could use Hoddle Street again. Shops might open up.

3. Better amenity because the elevation is so high.

The complaint about elevated roads is the same as the complaint about freeway overpasses. They leave dark empty spaces that are a blight on the urban environment. But if you put the road high enough up in the air, the sense of being closed in will disappear. Even better, if the supports for the freeway are not just concrete pillars but actual apartment buildings, the passive surveillance of these areas would be much better.

I would imagine that top-floor apartments, right under the roadway, would be less attractive as they would get less sun and more rumbles from above. But if they had balconies on the sides the road does not extend, there is no reason they could not be full of light.

The shadow from the entire structure will be vast over a wider area than a smaller freeway, but by having it so high, there will be no single space that is permanently shadowed and unattractive for licit activity.

The obvious downside is the ramping. The illustration shows a six storey building, which would be about 20 metres tall. To descend 20 vertical metres a car needs 120 metres of ramp,( the preferred gradient for public car park ramps is 1:6.)

That would probably have to circle around the building to descend, as per the pictures.. And I’m not convinced the value of the apartments encircled by those exits would be so high. Still, not every building would be an exit, and some exits could ramp away from the buildings.

A more complete set of things being proposed by Sir Charles Bressey 80 years ago can be found here. Nb. I do not agree with turning Trafalgar Square into a multi-storey parking garage.

According to a new working paper by economists at Stockholm University and the University of Chicago, a key factor making unskilled workers worse off is broadband internet.

That means the NBN (which may be the most popular infrastructure investment ever announced in Australia) won’t be good for everyone.

The study had access to amazing data on 80 per cent of firms and 70 per cent of employees in Norway in the period 2000-2008, during which time Broadband Internet was rolled out slowly in Norway, allowing meaningful comparisons.

“For every employee, we know his or her length of education, and annual labor income.”

If you have a university degree, you are considered to be “skilled labor.” The premium for skilled labor increased very neatly alongside broadband availability as it rolled out in Norway.

The result for unskilled workers is not so good:

“[T]he estimates imply that a 10 percentage point increase in broadband availability in a municipality raises wages of skilled workers in that local labor market by about 0.2 percent. By comparison, we find evidence of a decline in wages of low skilled individuals.”

The researchers constructed counter-factuals to measure what might have happened in the absence of high-speed internet. They show the gap between skilled and unskilled would have been lower if the optical fibres had never crossed the fjords..

The reason more educated people do better with the internet is that they tend to not be doing complex tasks

“The estimates suggest an important channel behind the skill bias of broadband internet is that it complements non-routine abstract tasks but substitutes for routine tasks…. the expansion of broadband internet re-enforced the wage premiums to workers performing abstract tasks. By comparison, the wages paid to jobs requiring routine tasks declined because of the broadband expansion”

Broadband internet is obviously putting the postman out of work, but it is apparently having a less obvious effect on a range of other routine but non-manual jobs. This is very much worth bearing in mind as the internet enriches and enlivens our lives in so many ways.

This is not an argument against the NBN. We need high-speed internet and we’re going to get it one way or another.

It’s an argument for being aware that some people get left behind. The smartest policy we can institute to deal with that is high quality, universal education. This should start with high quality earl childhood education (this is extremely important to ameliorate skill-gaps that can develop in disadvantaged populations even prior to starting school), extend through good quality public schooling (needs-based funding as per the Gonski Report is a good start), and culminate in excellent universities that remain highly accessible (this would probably preclude the deregulation currently being proposed by the federal government).

This could be the end of Australia as a right-wing country.

If the Coalition government loses office after a single term, that will be a lesson that will echo for generations. No government since 1929 has lasted just a single term.

The Budget of 2014-15 will go down in history as a masterclass of how to reverse an enormous lead. The government’s win in the 2013 election was enormous. The coalition won 53.5% to 46.5% – the strongest two-party preferred result since Howard beat Keating in 1996. Labor lost a whopping 17 seats.

But in the offices of Joe Hockey and Matthias Corman, this grand electoral advantage was soaked in petrol, and on the first Tuesday in May, they lit the spark.

The Budget was reviled as soon as the government started leaking its details. That sent them to their lowest poll number of 45% – a level to which they have sunk three times.

Some political events pass by, and others stick in the collective imagination and become a living part of our political reality. These events are political touchstones. The events aboard the MV Tampa, (Prime Minister Howard refused entry to Australia to a group of refugees) is a good example of a political touchstone. Howard’s poll standing shot up, saving an election that had looked very shaky.

That has never been forgotten – the existence of a range of harsh policies including detention centres in Nauru and PNG can be traced back to that election.

John Hewson’s explanation of GST on cake is another touchstone, guaranteeing that politicians give simple answers, not complex ones, to complex questions. (In trying to introduce a new tax, Mr Hewson got bogged down in the details on TV, and lost the election.)

When this Budget is remembered, the single biggest lesson will be about charging people to go to the doctor. This is a wildly unpopular policy. The memory of Gough is strong. Australians love Medicare. It doesn’t matter that the Government eventually dumped the policy. In fact it makes their situation worse almost, because they suffer all the reputational damage, gaining none of the budgetary advantages.

Should this Government lose next year’s election, Medicare will be very very safe for the next dozen electoral cycles. It will find champions on both sides of the political aisle. Indeed, politicians may clamber over each other to fund Medicare better.

The second grand lesson of the 2014-15 Budget will be about the deregulation of university. This is an issue I see coming up time and again. Do we want an Americanised higher education sector? The answer appears to be yes if you are a Vice-Chancellor and no if you are everyone else. If this government loses, centralised fee-setting and below market interest rates on HECS would appear to be safe for a long time.

The future is one where increased marketisation of public services is going to be very difficult to advocate for. The chance of policy proposals involving higher fees and less regulation ever making it out of cabinet meetings is going to be far far lower. All those MPs will know that their necks will be on the line.

The astute political operator might even see links from Australians’ apparent taste for government involvement with health and education to the enthusiasm for the NDIS and paid parental leave, and come up with a rather Scandianavian policy package to present to Australian voters.

Our future may be rather more Swedish than American, if the polls don’t tighten before the next election.

But that election won’t occur until the second half of 2016, leaving plenty of time for events to intercede. All the shortcomings of Mr Shorten may be yet to be fully known, a deus ex machina scenario involving terrorism or refugees could boost Mr Abbott’s standing at a crucial juncture, he could reform his ways after learning a very hard lesson in the first year of his term, or he could be replaced by Mr Turnbull. This last option would somewhat prove my point, because when the right-wing party is led by a centrist, it shifts the whole spectrum left.

I was walking down the street a few nights ago when two people zoomed past on bikes. I could hear them talking and one of them exclaimed, “A milk bar! Do they still have those? Who would ever go there?”

I looked over my shoulder at the shop I’d just gone past and sure enough, there was nobody inside.

It got me thinking.

I live in a suburb with three milk bars* within a few minutes walk of my house. (*a milk bar, for those unaware, is like a very small grocery shop selling the bare essentials with a focus on lollies, ice-cream and tinned goods. In parts of the world it may be called a general store, a corner store, a deli or a dairy.) Why is that? In my whole life, I’ve never been so near to so many milk bars.

2 minutes 40 walk to this one:

3 minutes walk to this one:

6 minutes 40 walk to this one:

Complete with core demographic of kids on holidays.

These are not sophisticated places. They have so little internet presence you can’t even find them on Google Maps. They don’t even have names. They exist principally for locals to pick up a few things.

I remember when I was a boy of about five, the milk bar near my family home closed. At that stage I’d only gone there to get lollies once or twice, but I sure was disappointed. I understood that as the end of an era. Retail was consolidating into a few big supermarkets and people didn’t need milk bars any more.

I subsequently moved to a house in North Fitzroy that had one milk bar nearby but I only used it once, when I was halfway through cooking and realised I needed another tin of tuna. It cost $7. So milk bars stopped figuring in my life. Until I moved to Clifton Hill. Then they were everywhere.

The three milk bars pictured above differ in their product offerings.

The closest one sells newspapers, has a coffee machine, sells Baklava and stocks a moderate range of groceries.

The second closest one does some deep-fried takeaway foods and stocks a minimal range of groceries.

The furthest one has DVDs, does dry-cleaning and stocks a minimal range of groceries.

There’s also, in this suburb, a continental supermarket, which I almost consider a milk bar. But since it calls itself a supermarket I will give it the benefit of the doubt. It is all of 40 metres away from one of the milk bars.

I was trying to explain to myself what it might be about the nature of this particular quiet, leafy, left-wing pocket of the inner north that made it so inclined to milk bars. Might the residents tend to be very forgetful and need to pop out for more cat food? Might they prefer not driving to the shops? Might they be opposed to big supermarkets? Any of these seemed unlikely given the rest of the inner north is demographically similar.

The reason, I eventually concluded, is the absence of big supermarkets. Clifton Hill is tucked into a bend of Merri Creek and that makes it probably uneconomical to put a big supermarket here. The above-mentioned Continental Supermarket does an okay job, and there’s a small FoodWorks around 15 minutes walk away too, (although it has earned the nickname ExpensiveWorks.)

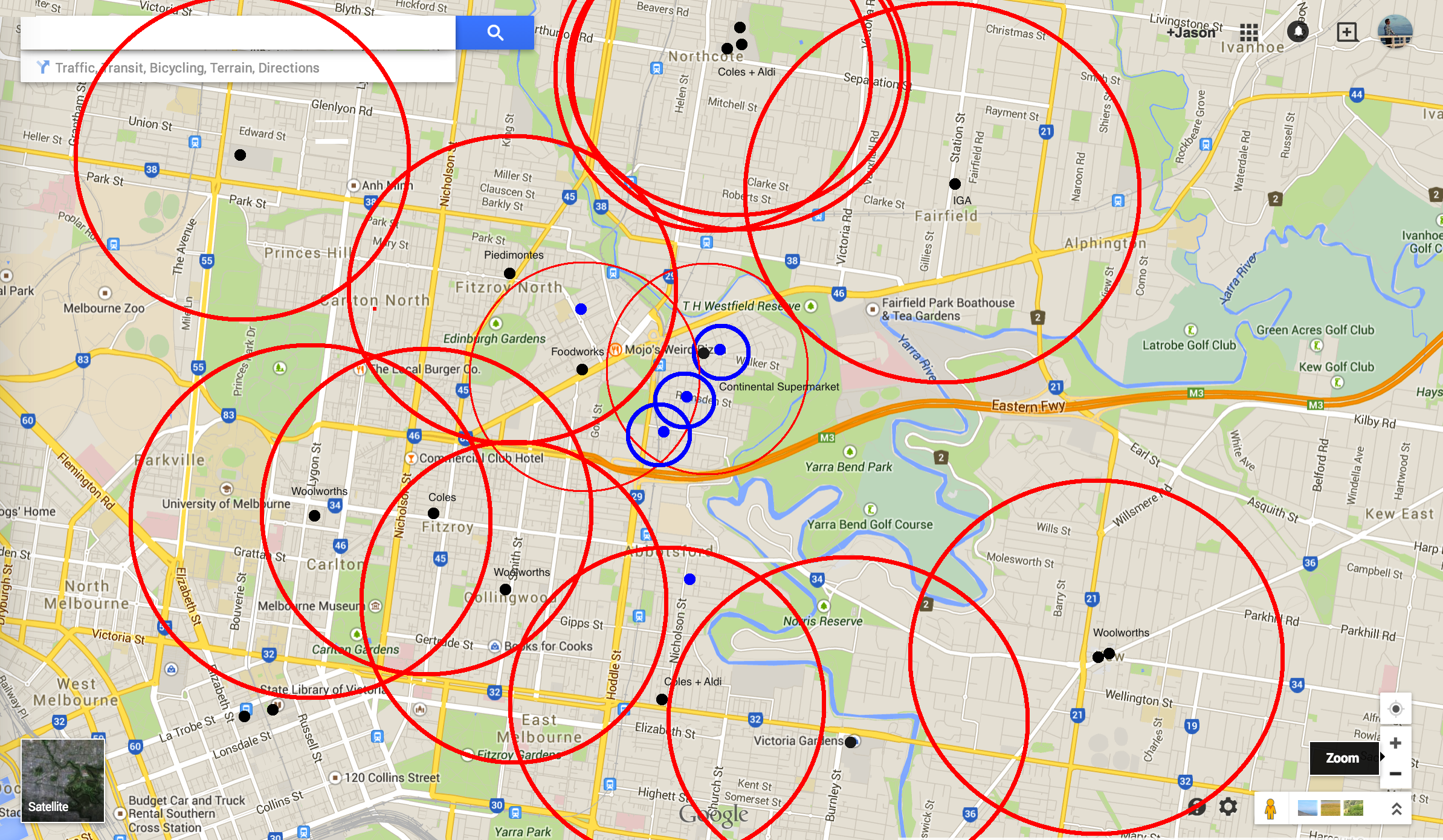

I mapped the supermarkets of the region and I can report that it is 2.3 km to the nearest major supermarket, Smith St Woolworths, 2.4 km to Piedimontes supermarket and 3.3 km to Northcote plaza. That is apparently the magic distance you need for milk bars to start clustering.

In the following map, Supermarkets are black dots and the local milk bars are blue dots. I’ve put rings around them to indicate their catchments, for purely illustrative purposes. There are smaller, lighter red rings around the two small “supermarkets” that serve Clifton Hill. What is most notable is Clifton Hill is rare in being so far from a major supermarket.

Click to open larger

In a lot of the inner north, the red circles overlap. This suggests higher population density, sterner competition, and perhaps lower willingness of residents to drive to the supermarket. I suspect in much of Melbourne, the red circles would be far apart, leaving gaps just like Clifton Hill, but the population density would not be enough to support such a density of milk bars.

I’d be very interested to hear about other regions that seem to support disproportionate numbers of milk bars. Do they also fall into the cracks, more than 2.4km from a major supermarket? Or are there other reasons you can think of for their continued existence?

Bitcoin has proven to be a shocker of an investment. I’d been considering buying some for about a year and in this case not acting has saved me a fortune.

Since I first mentioned Bitcoin on this blog, in November 2013, the currency has fallen 84 per cent in US dollar terms. At that time it was trading for $US1097. Now the value of a bitcoin is $179 and some bitcoins have changed hands for under $160 in the last few hours.

One way to look at the digital currency is as a proxy for distrust in mainstream currencies. With the US dollar and the US economy performing a lot better, bitcoin’s raison d’etre takes a hit.

There’s also the simple fact to remember that bitcoin is a currency – when the USD appreciates, the value of bitcoin falls. That may explain a fraction of the fall.

In Aussie dollar terms, a bitcoin investment has fallen less. With the Australian dollar falling from $US0.95 at the start of November 2013 to $US0.81 now, the value of a bitcoin has fallen only 81 per cent instead of 84 per cent. You can still buy a Bitcoin for over $200, in AUD.

With the falling value of Bitcoin, the bitcoin “miners” who run very expensive computers to obtain bitcoins are out of pocket and on the brink of going bust. (“Mining” is the clever idea at the core of Bitcoin. The very expensive computers do cryptographic work that allows the currency to be secure, and in return get Bitcoins from the system. The higher the value of Bitcoins, the more powerful computers that can be economically thrown at the task.)