The US Federal Reserve chair presides over a country in pretty good economic health. Unemployment is just 5.3 per cent. But even though the official interest rate is zero (technically 0 to 0.25 per cent), there is huge pressure to not raise that official interest rate.

Commentators are right to be cautious. There is plenty of evidence supporting being very cautious about raising rates.

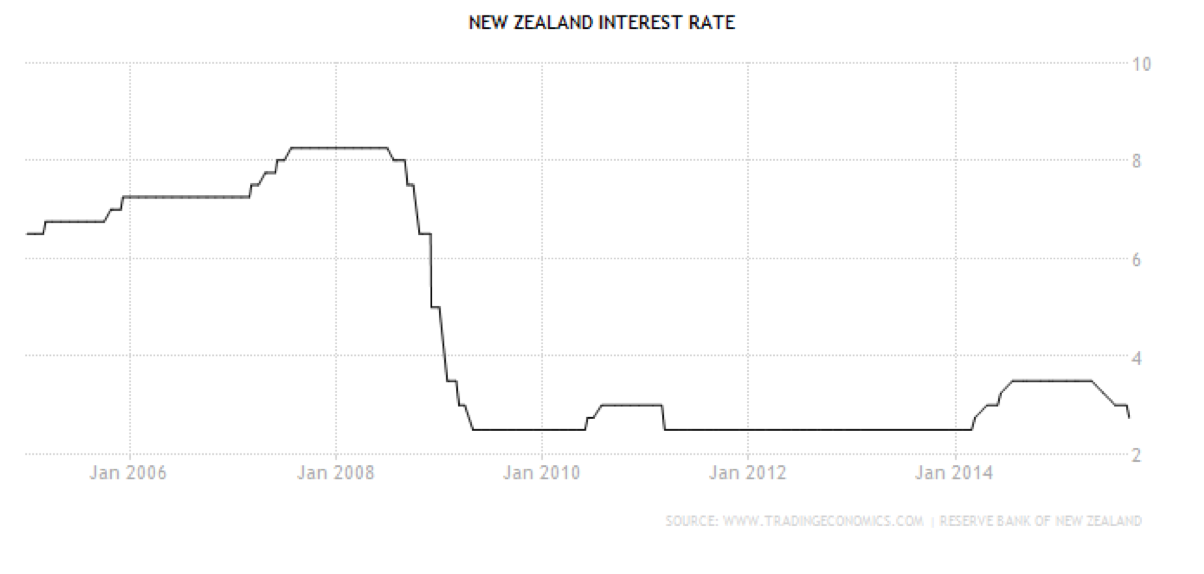

Both Australia and New Zealand lifted interest rates from their GFC lows swiftly. Australia did so in 2009, NZ twice in 2011 and 2014. Both countries dropped rates again soon afterwards, as these graphs show, .

Being hasty in raising rates is unwise. So Yellen’s cautious stance is probably appropriate.

But her position is especially difficult because her options are so limited. US rate changes, by convention, happen in lumps of 0.25 percentage points. Just like Australia’s and New Zealand’s.

She faces, by convention, a binary choice. Leave rates steady, or execute a 0.25 point hike that could frighten markets.

A quarter of a percentage point probably appeared vanishingly small back in those dimly remembered normal times, when interest rates were so much higher. But now a quarter of a percentage point looks like quite a hurdle.

The size of a standard rate move now raises questions.

A key one that nobody seems to be contemplating: Should rate rises be the same size as rate cuts? The obvious answer is no.

Economies tank hard. Recoveries are slower and more tentative. Unemployment rises steeply, but it falls slowly, as this next graph shows.

There is an implicit understanding that rate cuts can be bigger than hikes. The Australian government bundles groups of 0.25 together when things go bad particularly quickly. For example the RBA made a cut of 0.50 in 2012, and three cuts of 1.0 in late 2008 and early 2009.

But there is no explicit understanding that rate cuts could be smaller than 0.25 when they are rising.

Why? There is no apparent technical impediment to this.

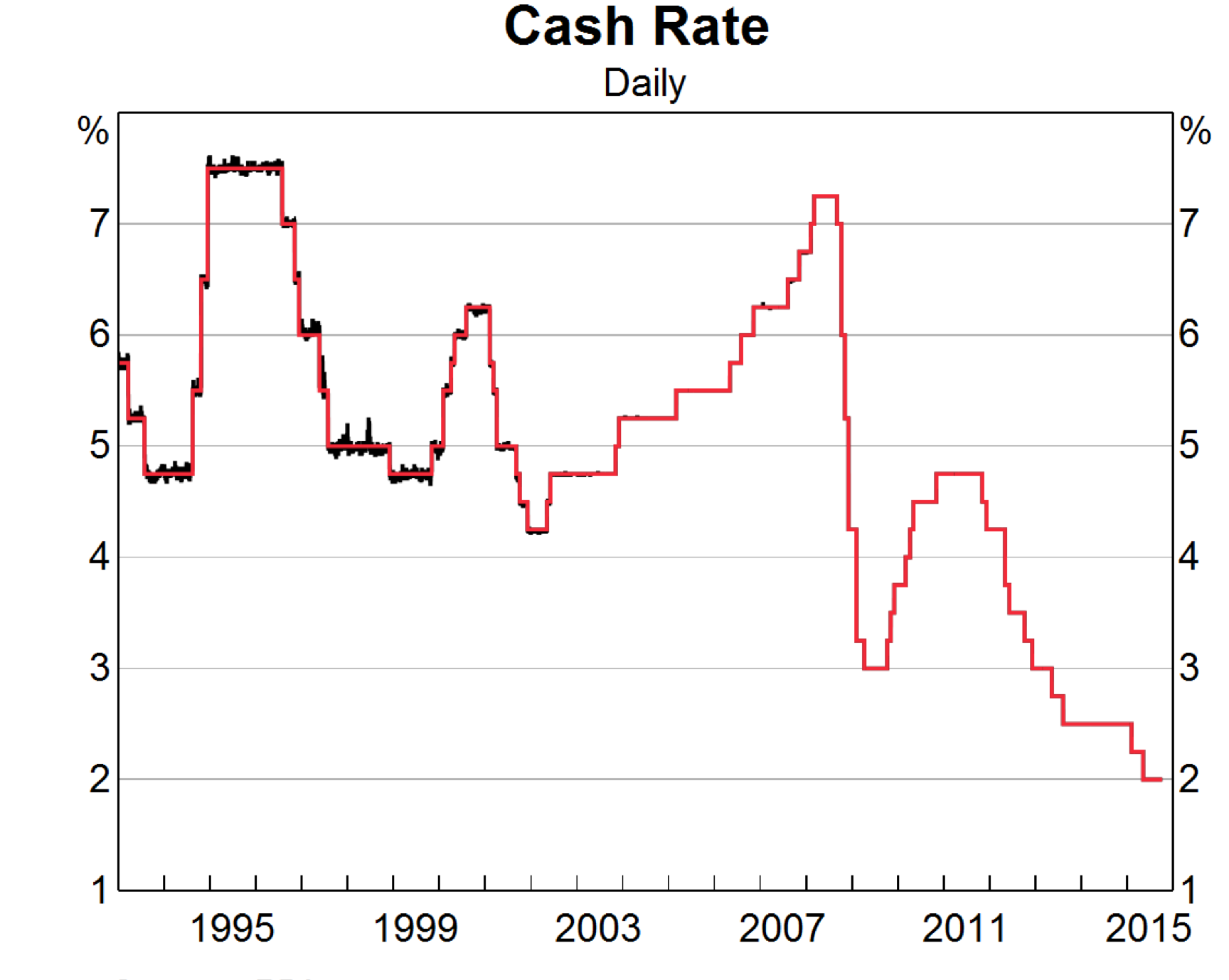

Australia is now perfectly capable at holding rates at levels more tightly defined than 0.25 per cent intervals, as this graph of the target (red) and actual (black) rate shows:

Whether Yellen should raise rates is a divisive issue. She can counter that political division with a bit of arithmetic division.

Splitting her first hike into several small pieces is the answer. Rises of 0.1 per cent – or even smaller – could be just the trick at difficult times like this.

Written by respected economics journalist Peter Martin, it makes some very bold claims without any sourcing. For example:

“Concern about a deteriorating economic outlook and a resurgent Australian dollar will force the Reserve Bank to cut interest rates on Tuesday, taking the official cash rate to an all-time low of 2 per cent and discounted mortgage rates to just 4.55 per cent.”

How could he know? Normally, such a story obsesses on the implied chance of a rate cut, quotes experts and goes out of its way to show where all the ideas in it come from. Take this Peter Martin story from January for example.

“Inflation is simply not a concern, the Bank’s decision in February need pay no heed to the consequences for prices,” said BT Financial Group economist Chris Caton…

But futures traders marked wound back their bets on a February interest rate cut, cutting the implied probability from 84 per cent to 66 per cent. “The underlying inflation figure came in just above the market’s expectations,’’ explained NAB currency strategist Emma Lawson. “That allowed some pricing of the expected cut to be taken out of the market.””

This new story lacks a single quote, but it isn’t marked as an opinion piece either.

It is hard to avoid the conclusion the RBA is briefing key journalists on what it will do next.

Two key questions occur to me.

1. This is a big new deviation in the RBA’s communications strategy, which until now had relied on officials making public speeches. Speeches have the advantage of being clearly attributable. If definitive information is being given out, why not give it out in a transparent way?

2. If the RBA can brief journalists on what it will do five days in advance of the board meeting, what exactly is the board meeting for?

The RBA board is stacked with high-flying people chosen for their ability to contribute to the making of monetary policy.

As well as the RBA Governor Glenn Stevens and his 2IC Philip Lowe, the board table has

John Akehurst, director of CSL

Roger Corbett, chairman of Fairfax

John Edwards, director of the Committee for the Economic Development of Australia

Kathryn Fagg, director of Boral

Heather Ridout, chair of the Australian Super Trustees Board

Catherine Tanna, managing director of Energy Australia.

John Fraser, Treasury Secretary

Are these great loci of business and economic acumen merely a rubber stamp for the calculations of the RBA?

I suppose it’s obvious that the RBA drives the meeting – it has the staff working on the question of rate cuts month in and month out. They provide the chair, set the agenda, and doubtless distribute packages of graphs to all present.

But now I wonder if the board meeting is really a discussion at all, or whether the gathered brains chew sandwiches while the RBA shows a power point presentation, concluding by presenting the next movement of the official cash rate as a fait accompli.

If that’s the case, ought we have a board and a board meeting at all?

“Overall, the Bank’s assessment is that output growth will probably remain a little below trend for somewhat longer, and the rate of unemployment peak a little higher, than earlier expected.”

So could option c) be the answer? They’ve found a way to contain housing risks?

It was only yesterday that Prime Minister Tony Abbott made a very public announcement about a crackdown on foreign investment in real estate.

“I am a friend of foreign investment but it has to come on our terms and for our benefit. The government will shortly put in place better scrutiny and reporting of foreign purchases of agricultural land and better enforcement of the rules against foreign purchases of existing homes so that young people are not priced out of the market.”

It was hard to process that announcement at the time, being bereft of context and detail. There had already been a crackdown announced. Was this new approach to have a louder crack, or push further down? It was a mystery.

Until the RBA rate cut.

I hadn’t though of a linkage here until I saw the question posed on Reddit. The person who asked the question in that forum sees causation running the other way, with an interest rate cut necessary to accommodate the deflationary effect of the crackdown.

But we know that the order in which things are revealed does not necessary accord with causation. Assuming so is to fall victim to the simplest kind of fallacy: post hoc ergo propter hoc.

The RBA may be betting that keeping Chinese money out of the market will help keep a lid on things.

Will that work? It might. Foreign investment represents only a tiny share of our market. But introductory economics textbooks tell you, economists think at the margin. A few extra bidders for a house can be what pushes the price of that house through the roof.

Think about it like this: if there 100 seat in lifeboats and the ship is sinking, the price of lifeboats will be zero if there are 99 passengers, and start to rise very rapidly if there are 101. The marginal bidder is important.

Last year, the RBA left rates on hold. Despite increasing unemployment and modest inflation, the bank decided that “a period of stability” was the best course for interest rates.

At the December meeting of the RBA board, they seemed calm. The statement released said

“…most data are consistent with moderate growth in the economy……. monetary policy is appropriately configured. … the most prudent course is likely to be a period of stability in interest rates.”

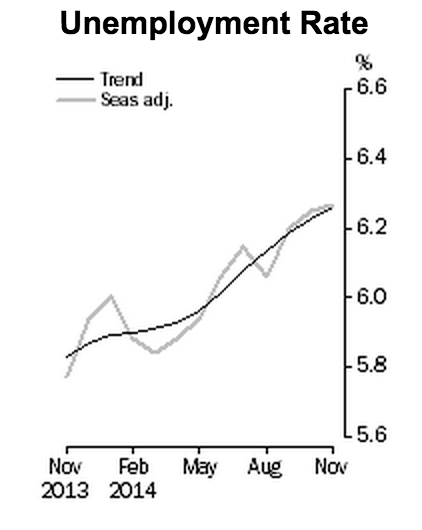

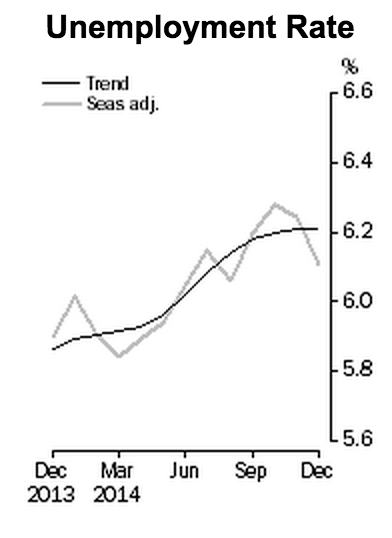

But the meeting was followed the very next day by the release of the National Accounts which showed “dreadful” growth in the quarter, of 0.3 per cent. And shortly thereafter, unemployment figures came out looking like a horror show. Trend and seasonally adjusted measures converged on 6.3 per cent. A record high.

The bank suddenly seemed perturbed. In an interview published by the AFR on 12 December, the Governor said:

“…if at some point we can be more helpful for confidence by doing something different, then obviously that will be on the table, and we will take a fresh look at all these things in the new year”

In the minutes of the meeting, released two weeks after the meeting and four days after publication of that interview, the labour market was singled out:

“…members noted that subdued labour market conditions were likely to weigh on consumption growth and consumer confidence more generally.”

So perhaps Glenn Stevens spent the long summer fretting he’d left the interest rate unchanged for too long. Perhaps he sipped light beer by the pool and bored his bbq guests by extemporising on how a two-month break between the December and February meetings was inappropriate for a modern economy. Perhaps his long summer nights were filled of dreams of a rate cut.

But then the New Year began and with it came more positive news on the economy.

Unemployment, when the December figures were released in mid-January, was suddenly much better.

November figures released in December.December figures released in January. (note, for all the fans of the trend line, how it moves in several periods on the release of new data. The seeming predictive power of the trend line is achieved via retrofitting!)

At the same time, the Aussie dollar went into freefall. It has gone from US85c at the time of the December meeting to just under US78c today. (under seventy-eight?! oh my god this upcoming American trip is going to kill me.) The speed at which the economy can expand is affected not only by interest rates but also the exchange rate, which are lumped together under the terminology “monetary conditions.”

The lower exchange rate boosts the economy in several ways. Both by making imports less competitive, and by making it easier to export. It should also reverse the enormous disparity between the number of Aussies who go offshore and the number of tourists who arrive. (A lower exchange rate is not without costs, of course, as many goods, especially capital equipment, is imported).

In all these ways, a lower exchange rate does the same work as a rate cut, all without Mr Stevens lifting a finger. Best of all, the lower exchange rate should not lead to higher house prices, which is very welcome as bubbles remain a topic of great importance to the RBA.

Last but probably not least, the falling oil price is going to put stacks of cash in consumer pockets. I filled up the car with glee the other day. Unlike falling interest rates, which rob from savers to give to borrowers, lower oil prices are pure upside for consumer buying power, and therefore a more powerful spur to consumer confidence.

That same PDF, authored by Westpac, predicts two rate cuts this year. But is that really going to happen? For that to come about, the bank would need to have changed.

Inflation was not a major concern and probably won’t be so long as the falling dollar is pushing average prices up, cancelling out the falling oil price.

The bank’s two big worries have been the housing market and the unemployment rate. With house prices still rising at the end of last year, it must surely be frightened of a 2015 full of headlines featuring a median house price nearing $1 million in Sydney. And unemployment looks like easing.

I bet the RBA will leave rates on hold again.

But the one thing that sticks in my mind is this article in the Herald Sun. Business Editor Terry McCrann has a long report on why the RBA will cut interest rates. It is specific enough and well-researched enough to appear to be a leak rather than (like this piece) the author’s own ideas.

McCrann writes:

“The RBA will be reducing both its growth and inflation forecasts in this statement [a report to be released after the board meeting]….

Critically, on (underlying) inflation, the RBA will also make its first point-forecast for June. It is likely to be 2.25 per cent, it could be as low as 2 per cent — either way, significantly, very significantly,below the 2.5 per cent midpoint of its 2-3 per cent target range.

Almost as significantly, it will cut its December forecast inflation range to 2-3 per cent and do the same for at least the first half of 2016.

In short it will be forecasting weakish growth and inflation below target. It quite simply could not release those figures on the Friday and have left its official rate unchanged on the preceding Tuesday. Or at least signalled a pending rate cut.”

If he is right and the forces pushing down on inflation are far greater than those lifting up, then you can’t help but expect a rate cut. It’s an inflation-targeting bank, after all. Tuesday will tell.

The US consumer price inflation rate in August was -0.2 per cent. Negative inflation in the month and up just 1.7 per cent in the year. Despite the US Federal Reserve moving heaven and earth to avoid such an outcome.

The Fed has cut interest rates to near zero and done over $3 trillion worth of “quantitative easing” in order to try to lift inflation up into positive territory. That’s “loose” monetary policy where the government pumps money into banks. Their ultimate goal is to get higher inflation to give the economy a boost.

But there is another school of thought. That maybe the reason they’ve failed to cause inflation is that quantitative easing actually causes deflation.

This idea is shocking. When I first saw it getting serious attention, I had to check to make sure I wasn’t on The Onion. Surely QE is an increase in money supply, and so should cause inflation.

The list of governments engaging in QE includes the US, UK, and Japan. If it doesn’t work, then how in holy hell has the global economy not collapsed by now?

Here’s the data since 2000 on inflation in those countries

US began QE in late 2008; really ramped up with unlimited QE3 in Sept 2012Japan was doing limited QE over a decade ago. It really ramped up its QE in 2013. That recent blip in the chart is mainly due to a rise in GST/VAT, however.UK did limited QE in 2009/10 and 2012.

To me, these graphs look ambiguous. If QE causes deflation, how?

There are a few answers floating around, with the most often cited one being this (and it’s slippery):

“Quantitative Easing increases the total amount of money in circulation. That money has to belong to someone. It has to be in someone’s wallet or in some bank’s vault or somehow “held” by some person or institution. With the interest rate stuck at zero the only way that folks are going to agree to this if the inflation rate goes down. That’s because high rates of inflation make people want to hold less money and more tangible assets. This is what economists call an equilibrium condition.”

If the causation in this seems to run a bit backwards, that’s because the logic started off in mathematical identities about the economy, not in a verbal argument. (“the only way folks are going to agree to this” seems to be the verbal version of taking a variable from one equation and substituting it into another).

It depends on something called the “liquidity premium” which has to do with how much compensation people want to hold their assets in cash. To me, the causation runs the other way. You control your cash holdings, not the inflation rate. The idea agents can hold down the inflation rate just because they currently have a lot of cash seems silly.

But my belief in mathematical economic proofs is at the zero lower bound anyway, and you can’t argue too hard with the data (at least until you make a fail-safe counterfactual generator). Some sensible people are giving this idea credence, others not.

The idea that QE causes deflation is controversial. But the idea that it does not do much to lift inflation is more widely accepted. And that makes some people angry, because QE is not exactly costless.

One side effect is lifting the amount of assets the US Fed holds. It doesn’t just give out the cash under QE. It swaps cash for assets. So now the Fed owns a lot of “mortgage backed securities” – the same things that sparked the GFC – and that has some people arguing its solvency is at risk.

Another side effect is exchange rates. US quantitative easing can shoulder the blame for the high Aussie dollar over the last few years. That killed a lot of Australian businesses.

Australian house prices have seen inflation too, although not to the same extent. These trends have the Bank of International Settlements – the central banks’ central bank – in a flap:

“By fostering risk-taking and the search for yield, accommodative monetary policies thus continued to contribute to an environment of elevated asset price valuations and exceptionally subdued volatility.”

But the US QE program is finally coming to an end in October. The program which once added $85 billion a month in liquidity to the global economy is nearly at an end. It seems doubtful we will get a clear picture of what the effect was on inflation from this one program.

We may need many more iterations of financial crisis and government response to figure it out, and that may be just what we are going to get.

“I know the RBA sets interest rates but I’m embarrassed to ask why.”

Someone said this to me at a party recently. In trying to explain interest rate policy by shouting over Daft Punk I achieved simultaneous pedagogical and social failure.

This setting, I hope, is a more appropriate place to provide the answer.

The Really Simple Version:

Interest rates are the brakes on inflation (price rises). When the RBA changes interest rates, they are trying to control inflation.

Higher interest rates slow inflation down.

If you notice the price of a sandwich keeps going up, the Reserve Bank is probably getting worried about high inflation. The RBA watches price rises by looking at the consumer price inflation data. If inflation is getting too high they will raise interest rates.

Lower interest rates speed inflation up.

On the other hand, if shops are having big sales that suggests prices are falling. The RBA is probably worried about low inflation. It might cut interest rates.

The RBA’s job is to keep consumer price inflation between 2 per cent and 3 per cent, annually. If price rises are above 3 per cent, they will raise interest rates. If price rises are below 2 per cent they will cut interest rates.

How does that work?

High interest rates slow down spending.

For people: If interest rates go up, it makes sense to put more money in the bank, not spend it.

For companies: If interest rates go up, you won’t borrow money to build a new factory. You’ll try to pay back your loans.

Low interest rates do the opposite.

For people: If interest rates go down, it makes sense to take your deposits out of the bank and spend them.

For companies: If interest rates go down, you can borrow to build a new factory.

Spending matters because the rate of spending affects the way companies set prices. If items are not selling, companies will put them on discount. If they are selling out, they may even put up prices.

This is the basic lesson. The RBA is controlling interest rates, to affect spending, to affect inflation.

The fairly simple reason we care about inflation:

Too much inflation can be bad – it means the money you have saved buys less and less.

But we don’t aim for no more price rises ever – because price rises can be good. Inflation can be good because it CAUSES spending. I know we just said spending causes inflation. But it works both ways. Think about this:

If inflation is high, your money is losing value, so it makes sense to spend it. If $100,000 will buy you a Mercedes today, but it will cost $105,000 next year, it makes sense to spend the money now. That spending will pump up the economy.

If inflation is low, however, it makes more sense to save your money. Of course, if everyone saves, the economy suffers.

i.e. The way people react to inflation (spending/saving) is important to economic growth.

The RBA tries to balance the speed of the economy so we get the right amount of spending and saving to keep the economy growing. Inflation is kept between 2 and 3 per cent, because we’ve decided that is a good range to keep spending and saving in balance.

Why do we care about growth? Growth affects unemployment, and thereby people’s health and happiness. That’s why the newspapers pay so much attention to it.

Advanced class: How does the RBA control interest rates?

The RBA doesn’t set your bank account interest. And it doesn’t set your home loan rate. So what is it controlling?

The one market that rules them all.

The overnight cash market is the shortest-term loan in the market. Big banks borrow in there for just a few hours.

Because you can make a year-long loan out of 365 overnight loans, targeting the overnight loan market affects all other loan markets.

“…allow the Reserve Bank Board to focus on price (currency) stability, which is a crucial precondition for long-term economic growth and employment, while taking account of the implications of monetary policy for activity and levels of employment in the short term.”

You get a short term bump in employment under high inflation because the wages are not actually worth as much as the workers thought they would be. Workers aren’t dumb though, so once they re-calibrate their inflation expectations, they stop being willing to work for those crappy wages.

That means solely focusing on inflation is the surest way to promote low unemployment.

That’s the end of the lesson on interest rates! I hope it was helpful. Now you can nod wisely when Alan Kohler does the finance news.

Being hasty in raising rates is unwise. So Yellen’s cautious stance is probably appropriate.

Being hasty in raising rates is unwise. So Yellen’s cautious stance is probably appropriate.