In Europe, something wild and new and kind of dangerous is happening. They’ve put negative interest rates on deposits.

Imagine putting your money in the bank, and getting a negative interest rate. You’d want to get it out again as soon as possible, right? That’s the point.

Interest rates are used to control activity in the economy. I wrote about this a few months ago: “I know the RBA sets interest rates but I’m embarrassed to ask why. An explainer.“

If the interest rate is negative, the central bank is goading you into using your money, not just sitting on it. That should mean more spending. More spending makes more jobs. And like this they hope to get Europe out of the quicksand of high unemployment.

So, if this works, how come it’s never been tried before?

The thing is, interest rates don’t just work on their own. You’ve got to consider inflation. If you get 2 per cent interest on your deposit but inflation is 3 per cent, then really you are losing the purchasing power of your money. (in the business this is called “negative real interest rates” where the word “real” means inflation is taken into account).

You can make “negative real interest rates” by setting the interest rate below inflation. That’s easy. The problem in Europe is there’s so little activity that inflation is very, very low. They have to make the advertised interest rate negative to get the “real” interest rate negative.

Now, it’s worth noting that the negative interest rates don’t apply to the average punter. They are for the deposits that banks have with the central bank. (Millions and billions of euros every night).

The reason for that is simple. If you or I see that the $11.50 we have in the bank is attracting a negative interest rate (here I am ignoring the “real” interest rate), there’s a simple trick we can use – take it out of the bank and turn it into cash. Cash gets an interest rate of zero, so that’s a lot better than leaving your money in the bank.

But guess what? There’s talk in some economic circles about getting rid of cash so negative interest rates can apply to normal people too. It’s not coming from freaky fringe dwellers either, but mainstream people with Nobel Prizes and a lot of clout.

If you only have your money in electronic form, there’s no way to avoid keeping it in a bank account. You can’t put 1s and 0s in a shoebox under your bed.

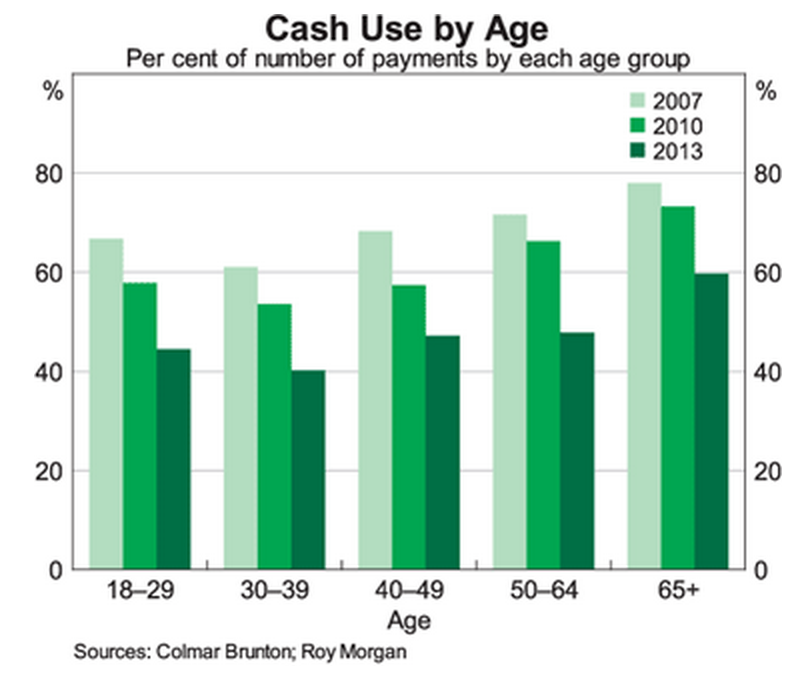

Negative interest rates would not necessarily cause a riot. Bank fees already work in such a way that we’re used to seeing our bank balances retreat when left alone. A cash free future is plausible. People are using cash less and less.

While the rise of Paypass could end up stranding us in a future where we actually pay banks to hang onto our money instead of the other way around, there are other innovations that make a cashless society with negative interest rates unlikely.

I am talking about Bitcoin. The rise of a kind of cash that is beyond the control of central banks means attempts to control rates on government-issued cash are more futile than in the past.

For now, here’s hoping that rates of -0.1 per cent can help reduce joblessness in Europe, where youth unemployment is a very frightening 23 per cent.

So the picture seems to be that mainstream economics once again fails to engage with reality. Haven’t we been hearing that runaway inflation is the main threat and burgeoning debt is going to swamp us? Enough of bogus problems, lets start acknowledging the real ones involving unsustainable degradation to eco-system services, reduced food output, rising insurance costs driven by climate change, increasing risk exposures of the poor and middle class, growing disparities in wealth and an alarming complacency about the effectiveness and value of democracy and the interesting effects of ageing population. What’s your take on the secular stagnation theory?

LikeLike