Janet Yellen is in a tough spot.

The US Federal Reserve chair presides over a country in pretty good economic health. Unemployment is just 5.3 per cent. But even though the official interest rate is zero (technically 0 to 0.25 per cent), there is huge pressure to not raise that official interest rate.

Commentators are right to be cautious. There is plenty of evidence supporting being very cautious about raising rates.

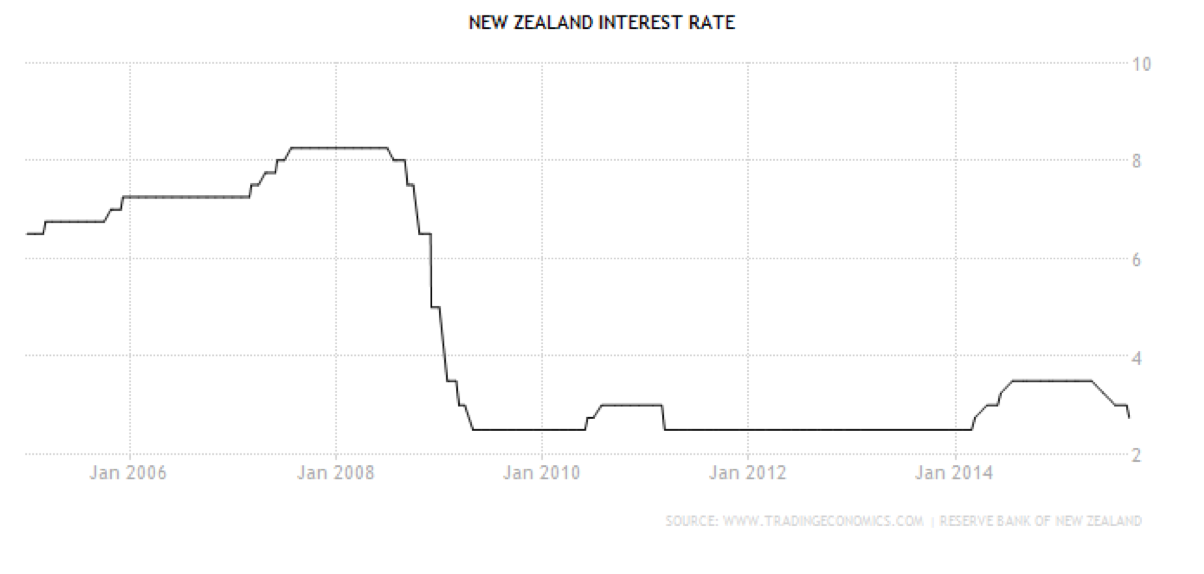

Both Australia and New Zealand lifted interest rates from their GFC lows swiftly. Australia did so in 2009, NZ twice in 2011 and 2014. Both countries dropped rates again soon afterwards, as these graphs show, .

Being hasty in raising rates is unwise. So Yellen’s cautious stance is probably appropriate.

Being hasty in raising rates is unwise. So Yellen’s cautious stance is probably appropriate.

But her position is especially difficult because her options are so limited. US rate changes, by convention, happen in lumps of 0.25 percentage points. Just like Australia’s and New Zealand’s.

She faces, by convention, a binary choice. Leave rates steady, or execute a 0.25 point hike that could frighten markets.

A quarter of a percentage point probably appeared vanishingly small back in those dimly remembered normal times, when interest rates were so much higher. But now a quarter of a percentage point looks like quite a hurdle.

The size of a standard rate move now raises questions.

A key one that nobody seems to be contemplating: Should rate rises be the same size as rate cuts? The obvious answer is no.

Economies tank hard. Recoveries are slower and more tentative. Unemployment rises steeply, but it falls slowly, as this next graph shows.

There is an implicit understanding that rate cuts can be bigger than hikes. The Australian government bundles groups of 0.25 together when things go bad particularly quickly. For example the RBA made a cut of 0.50 in 2012, and three cuts of 1.0 in late 2008 and early 2009.

But there is no explicit understanding that rate cuts could be smaller than 0.25 when they are rising.

Why? There is no apparent technical impediment to this.

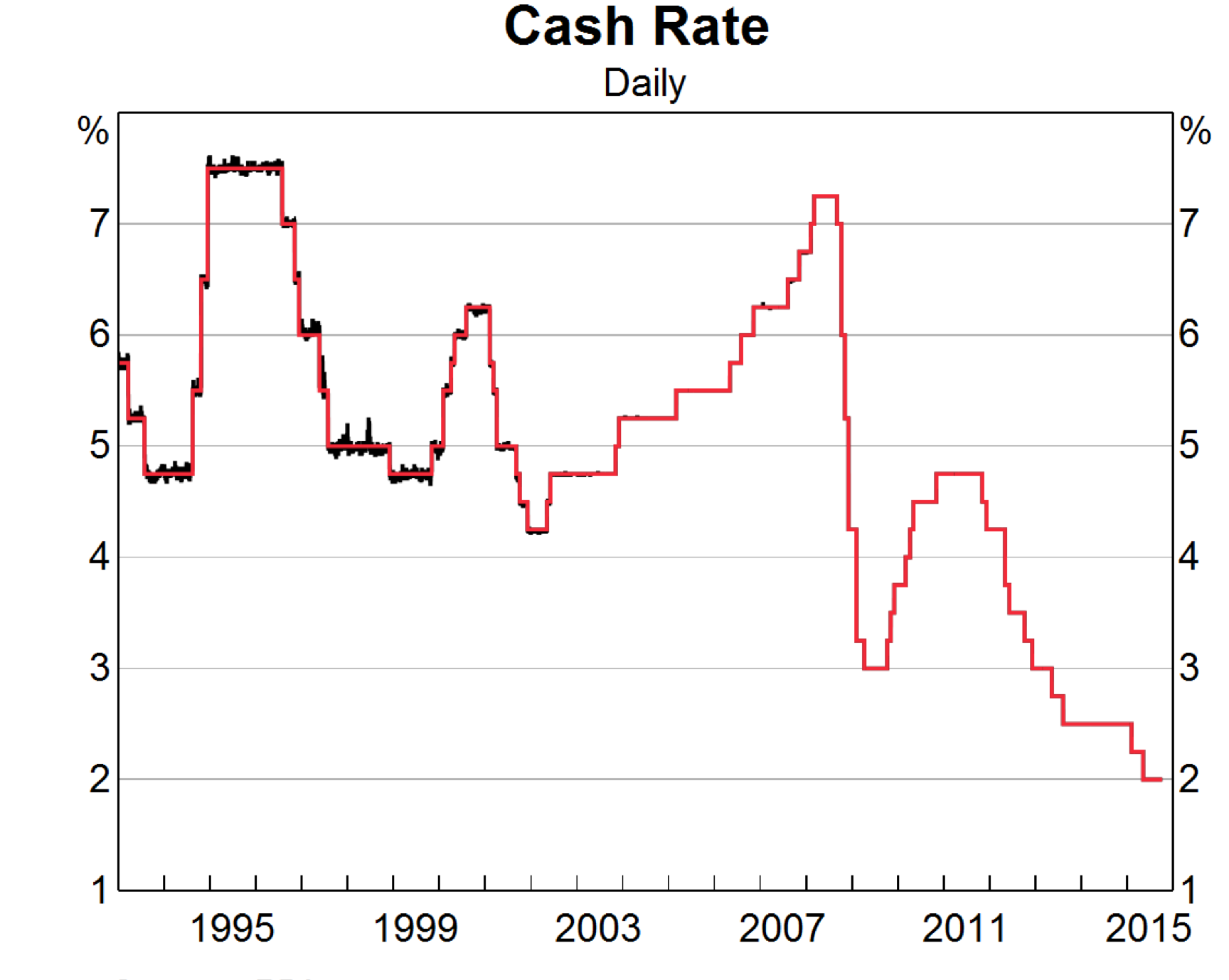

Australia is now perfectly capable at holding rates at levels more tightly defined than 0.25 per cent intervals, as this graph of the target (red) and actual (black) rate shows:

Whether Yellen should raise rates is a divisive issue. She can counter that political division with a bit of arithmetic division.

Splitting her first hike into several small pieces is the answer. Rises of 0.1 per cent – or even smaller – could be just the trick at difficult times like this.

Re Bunnings Vs Masters

Loved the article. but spare a thought for the struggling family businesses getting smashed by both these groups and price squeezed by suppliers who are trying to top up dropping margins as they get squeezed by Coles and Woolworths

How the hell can these Business survive ? don’t worry about masters if all these small businesses die you will have a duopoly that will agree on set prices and we will all pay more

Support small business

LikeLike

RE Rate rises – makes total sense. Sticking to increments like .25 off such a low base just because of convention is crazy.

LikeLiked by 1 person

Re: rate rises

I do agree with your assessment that there is the potential for less than a 25 point increase in interest rates, however I would suggest that any kind of interest rate rise at this point in the US would be less about controlling inflation and more to do with stimulating investor confidence. If there is a lower than normal rate rise, perhaps the actions would have less of an impact on the precautionary demand for money.

LikeLiked by 1 person

Right now, with global markets in meltdown, even a .01% hike is looking pretty unlikely!

LikeLike