The US consumer price inflation rate in August was -0.2 per cent. Negative inflation in the month and up just 1.7 per cent in the year. Despite the US Federal Reserve moving heaven and earth to avoid such an outcome.

The Fed has cut interest rates to near zero and done over $3 trillion worth of “quantitative easing” in order to try to lift inflation up into positive territory. That’s “loose” monetary policy where the government pumps money into banks. Their ultimate goal is to get higher inflation to give the economy a boost.

But there is another school of thought. That maybe the reason they’ve failed to cause inflation is that quantitative easing actually causes deflation.

This idea is shocking. When I first saw it getting serious attention, I had to check to make sure I wasn’t on The Onion. Surely QE is an increase in money supply, and so should cause inflation.

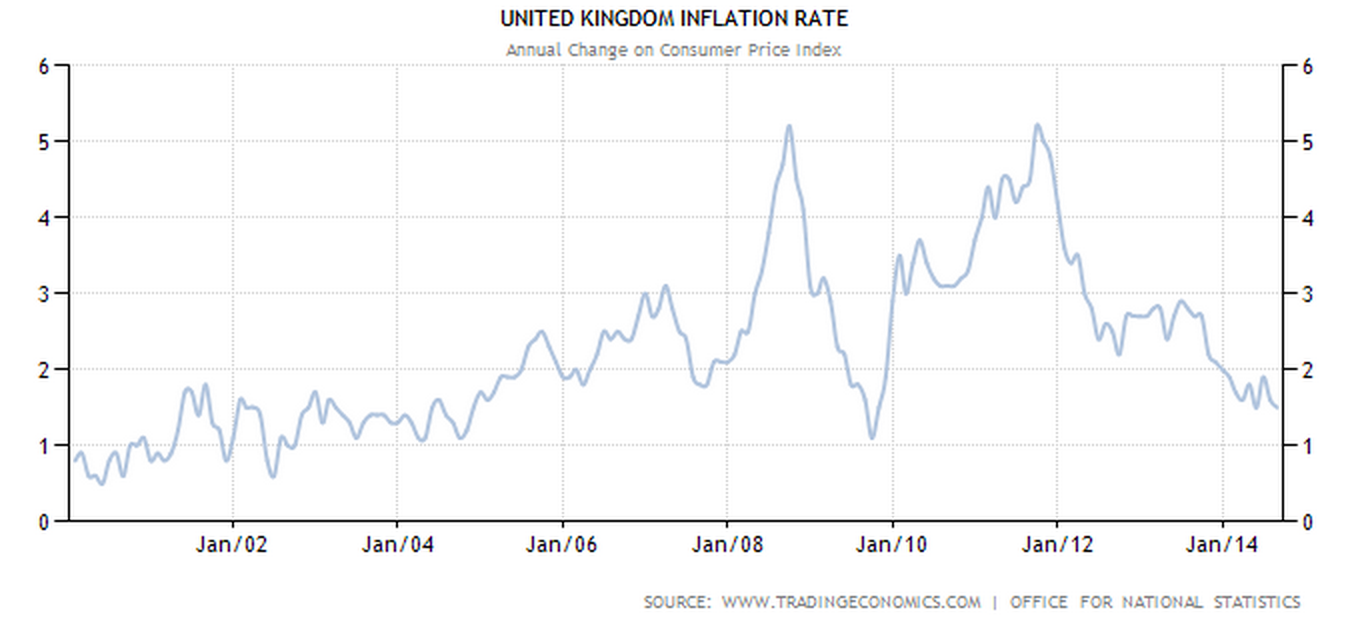

The list of governments engaging in QE includes the US, UK, and Japan. If it doesn’t work, then how in holy hell has the global economy not collapsed by now?

Here’s the data since 2000 on inflation in those countries

To me, these graphs look ambiguous. If QE causes deflation, how?

There are a few answers floating around, with the most often cited one being this (and it’s slippery):

“Quantitative Easing increases the total amount of money in circulation. That money has to belong to someone. It has to be in someone’s wallet or in some bank’s vault or somehow “held” by some person or institution. With the interest rate stuck at zero the only way that folks are going to agree to this if the inflation rate goes down. That’s because high rates of inflation make people want to hold less money and more tangible assets. This is what economists call an equilibrium condition.”

– Forbes summarising Stephen Williamson

If the causation in this seems to run a bit backwards, that’s because the logic started off in mathematical identities about the economy, not in a verbal argument. (“the only way folks are going to agree to this” seems to be the verbal version of taking a variable from one equation and substituting it into another).

It depends on something called the “liquidity premium” which has to do with how much compensation people want to hold their assets in cash. To me, the causation runs the other way. You control your cash holdings, not the inflation rate. The idea agents can hold down the inflation rate just because they currently have a lot of cash seems silly.

But my belief in mathematical economic proofs is at the zero lower bound anyway, and you can’t argue too hard with the data (at least until you make a fail-safe counterfactual generator). Some sensible people are giving this idea credence, others not.

The idea that QE causes deflation is controversial. But the idea that it does not do much to lift inflation is more widely accepted. And that makes some people angry, because QE is not exactly costless.

One side effect is lifting the amount of assets the US Fed holds. It doesn’t just give out the cash under QE. It swaps cash for assets. So now the Fed owns a lot of “mortgage backed securities” – the same things that sparked the GFC – and that has some people arguing its solvency is at risk.

Another side effect is exchange rates. US quantitative easing can shoulder the blame for the high Aussie dollar over the last few years. That killed a lot of Australian businesses.

The last side effect is a big rush on assets. All this loose money has pushed up asset price worldwide. The return on a 10-year Portuguese government bond has fallen to a comically low 3 per cent, from over 15 per cent. (Returns are the inverse of price).

Australian house prices have seen inflation too, although not to the same extent. These trends have the Bank of International Settlements – the central banks’ central bank – in a flap:

“By fostering risk-taking and the search for yield, accommodative monetary policies thus continued to contribute to an environment of elevated asset price valuations and exceptionally subdued volatility.”

But the US QE program is finally coming to an end in October. The program which once added $85 billion a month in liquidity to the global economy is nearly at an end. It seems doubtful we will get a clear picture of what the effect was on inflation from this one program.

We may need many more iterations of financial crisis and government response to figure it out, and that may be just what we are going to get.