The Governor of the Reserve Bank is a bit like Wile E Coyote.

He keeps buying more ACME house price growth dynamite and it keeps blowing up in his face.

After months of trying to talk down housing prices, Sydney house price growth has hit a new record pace. Meep meep!

At the RBA, this word would have been behind glass, marked “use only in case of emergency”. Exuberance, in financial circles, is a word that goes along with irrational.

Remember, the RBA Governor’s job is to be exceedingly sedate. Markets hang off his utterances. One unforseen word in a statement is enough to cause a front page story, and if he makes a joke, well, there’s trouble.

For him, using the word exuberance is a bit like anybody else going down to an auction in Marrickville and self-immolating as an excitable crowd bids a 2-bedroom flat up to $5.5 million. It means he’s serious.

But at the same time, he keeps cutting interest rates. That’s maybe necessary as the economy is so crappy at the moment.

But it drives up housing prices. There’s a bit of schism in property commentary, with a lot of chat about immigration and land availability, and less about how much people can borrow. We should never forget: the market for housing is as much credit as about land and structures.

While land is hard to get and housing construction has been more expensive during the mining construction boom, credit markets are loose as a goose.

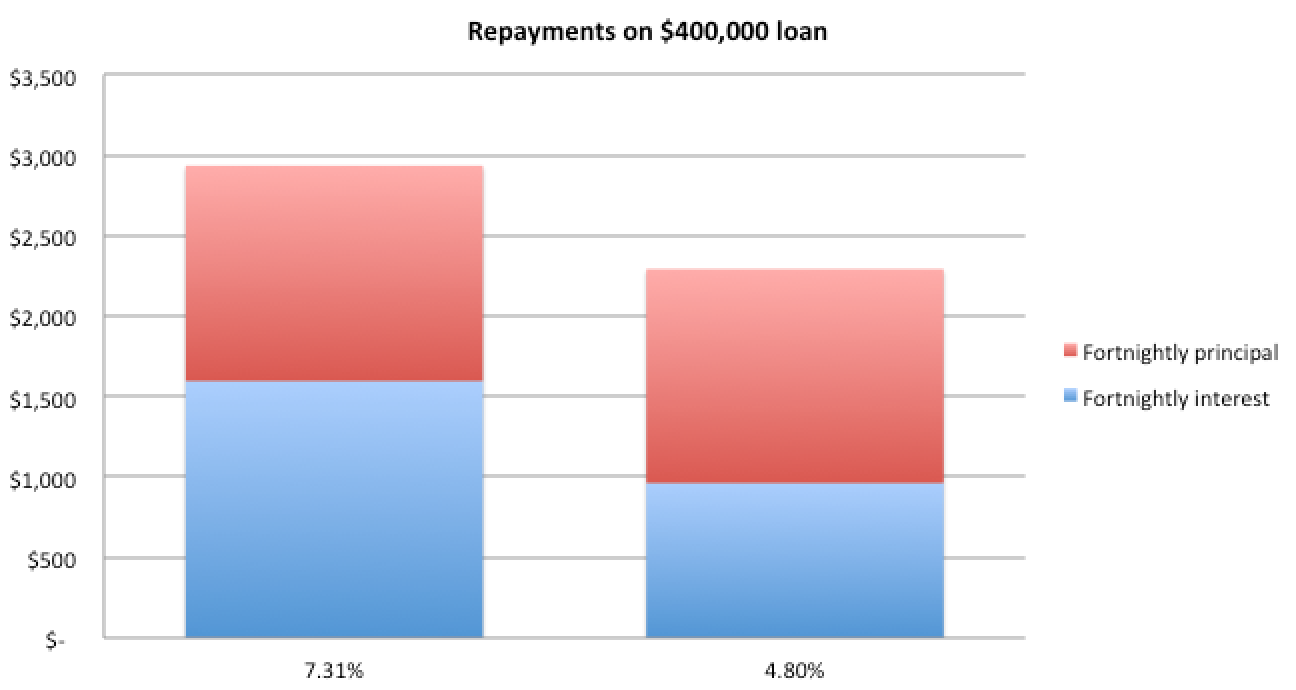

If you borrow $400,000 at the current standard discounted home loan rate of 4.8 per cent, you must pay back $687,597 to the bank over 25 years, in 300 payments of $2,292. That’s 42 per cent interest, 58 per cent principal.

If you borrow $400,000 at the average standard home loan rate of the last two decades (7.3 per cent) you must pay back $872,013 to the bank over 25 years, in 300 payments of $2,907. That’s 54 per cent interest, 46 per cent principal.

The repayment is 27 per cent bigger if and when rates go back up. You’re going to want to be richer to pay back that 400k loan then.

Do we see wages rising fast enough for that to happen?

Not really. Wages growth is a miserly 2.5 per cent annually, just one per cent above headline inflation.

It’s also worth noting many house purchases are not funded with wages alone, because they are investment properties. If mortgage repayments rise, will landlords be able to raise rents? Not if those renters aren’t also enjoying pay rises.

If investors start selling those homes, it could start a rush.

However, In New Zealand, the Reserve Bank has started raising interest rates, from 2.5 per cent to 3.5 per cent. And house prices are still rocketing in Auckland. So simply starting to raise interest rates won’t be enough to trim house price rises. Rates will need to hit a threshold where they start to sting.

That threshold may be some way away, but it surely exists.

This is a great article! Just to preface this with ‘I’m not an economist,’ so please tell me if I’m wrong. If somehow we managed to encourage people away from mortgages (eg. higher interest rates on/above the threshold, as the article suggests, and removing negative gearing) wouldn’t that mean people would have more disposable income, which would encourage spending and investment in areas other than property, which would create jobs for people, which would give others more disposable income, and so on? Wouldn’t this help consumer confidence and promote economic growth?

LikeLike

That’s a good argument – for the long run. In the short run, any sharp fall in house prices would have bad effects on consumer confidence. Also, perceived higher wealth is another driver of consumption. So falling house prices would trim spending in that way too.

But overall a n economy less tied up in housing seems very sensible to me!

LikeLiked by 1 person