Land tax is a great tax.

Just today, Treasury released a report that shows how much more efficient Land Tax is than all the alternatives.

I’ve previously argued that to promote land tax, we should emphasise that it is unavoidable. But I’ve gone cold on that idea.

It is true, but not a great argument when the government is going soft on tax dodgers. It simply encourages people to say we should enforce our existing taxes. [They’re right, we should. But we should have land tax too.]

Today the SMH economics guru Jess Irvine wrote a long and very welcome piece about land tax. But it conflated the hard-to-grasp concept of a low distortion tax with the easier-to-grasp concept of a tax that’s hard to “dodge.”

“Land tax is one of the most efficient taxes for precisely the reason it is unpopular: it is hard to dodge. They know where you live. You can hire as many accountants as you want, but it is difficult to hide that mansion in Point Piper.”

I found myself wondering why land tax is not on the agenda. And I think I’ve figured out why. The conceptual framework you need to grasp its benefits is not commonly shared. And you can see that by flicking to the hundreds of comments that followed the article.

The comments on the article were almost exclusively focused on fairness. Fairness is just one of the keys to good tax policy. Efficiency is the other. And there is a gulf of understanding between economists and the general public on tax efficiency, with economists to blame.

To get land tax out there you need to teach people why distortion is bad.

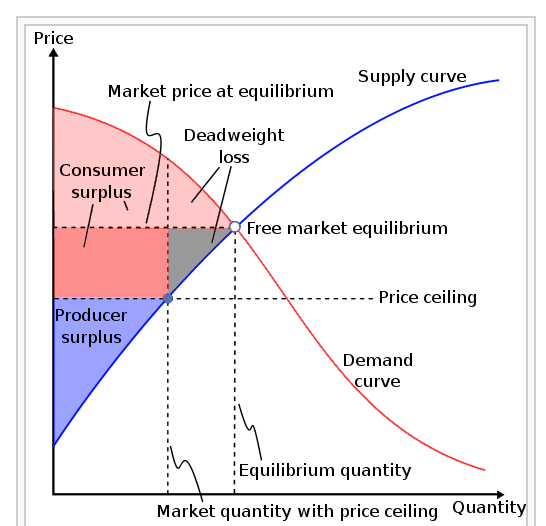

Economics students learn about a model of the economy like this: Trade is mutually beneficial. Taxes prevent trade. Therefore taxes prevent that mutual benefit. The amount of prevention (aka the distortion) is called deadweight loss.

The distorting effect of taxes is one of the great insights of microeconomics. It is counter-intuitive and hard to see, because deadweight loss is always a counter-factual. But can we transmit this flash of inspiration and insight from economics to the general public without messing around drawing supply and demand curves, or measuring utility?

A stumbling block is that the purpose of current taxation is so muddled.

We use taxes on “good things” to raise revenue. And we use taxes on “bad things” to change behaviour.

From observing the tax system, it may be unclear why smoking and working are both taxed. Does the government hate work?

The progressivity of the tax system – which I emphasise I support – doubtless contributes to this confusion. Being a low-wage worker, buying healthy fresh food and education attracts lower rates of tax. Being rich, buying luxury cars, eating at restaurants and making capital gains in shares attracts higher rates of tax.

It would be easy for some to see the tax system as a kind of moral agent, punishing bad behaviour and rewarding good. In this scenario, land tax makes no sense.

Explaining that taxes distort behaviour – but we want to minimise that! – is going to be a hard sell when the public sees we use taxes to distort behaviour all the time.

We tax all these things, and you want me to believe that’s because you want to stop some of these things, but you don’t want to stop others?

Fixing this will be hard. The terminology is a good place to start.

It cannot be helpful to use one word – “tax” – for both imposts on activities we actually want to encourage, like work, buying goods and services, making profits and owning land; and for things we actually want to discourage.

I’ll accept suggestions for how we could rename these taxes – Maybe they could be divided into Detrimental but Oh Well, it’s Necessary Taxes and Useful Pricing Taxes (DOWN and UP)?

This distinction would help plant the seed that some – but not all – taxes should be designed in a way that minimises distortion.

The journey to give land tax a fighting chance will be a very long one. The first steps in that journey will be to help give people the capacity to grasp why land tax might be desirable.