Roundabouts are good way to control traffic. But they are land-hungry. In certain places getting that land back should be a priority.

Land use is a topic that excites a lot of economists. We are obsessed with efficient use of inputs, and land is one of the trickiest ones to manage. Once some land is used in a certain way it can be used like that for years, or even centuries. This is path dependency in its original form – street patterns in some big cities were laid down thousands of years ago. Land use is growing even more important because we’re not making any more of it and density is growing

I believe I’ve got an idea for winning back some vital bits of land. To introduce the idea I want to show you a particular roundabout not so far from my house. It’s on a lightly trafficked road, it is very big and it’s on very desirable land.

What they need to do is join the land that is inside that roundabout to the waterfront. As it is, that land is cut off. It’s nice for birds maybe. But people can’t easily use it.

The view from there is amazing. it’d be a perfect picnic spot. There’s yachts in the foreground and the city skyline in the background. Highly Instagrammable!

Seems crazy to pave this spot

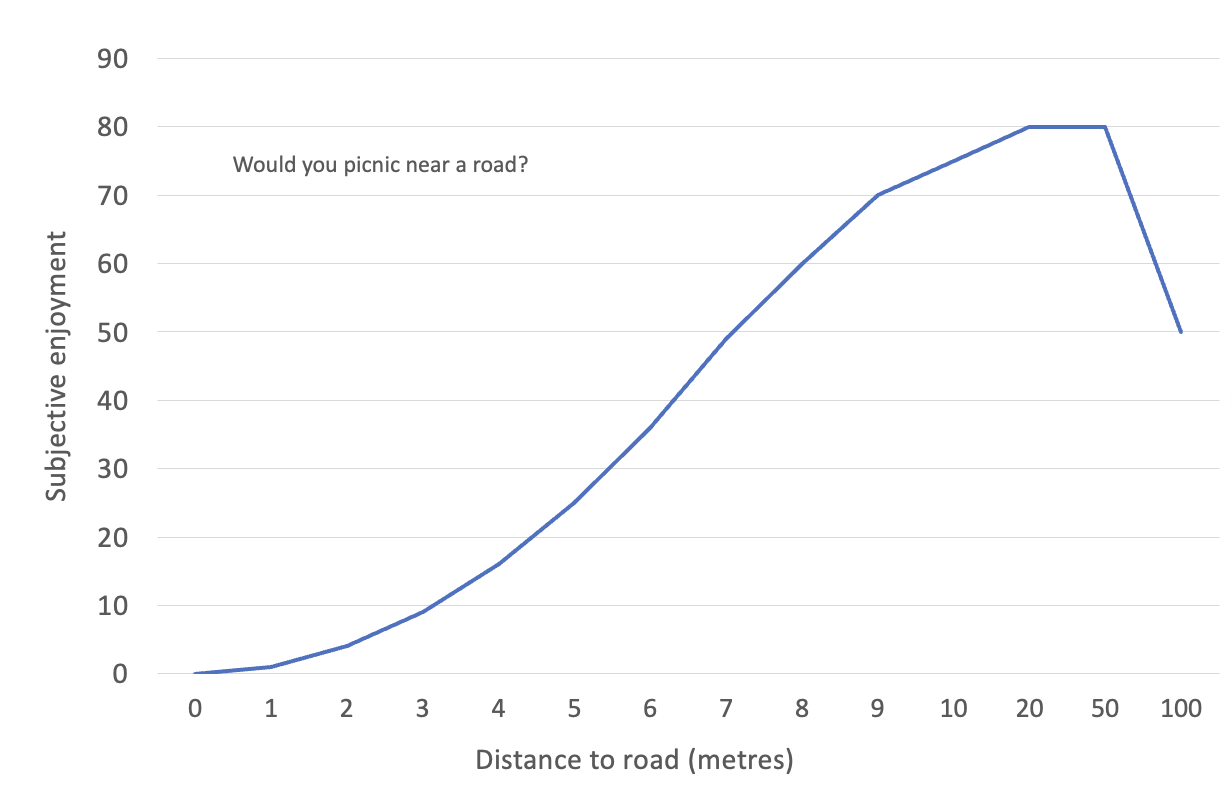

This idea flows from the principle that public space needs to be a certain size to be valuable to people. Little strips of grass or footpath next to a road are fine as buffers but not no good to sit in. a park or plaza needs to be a certain size to be nice to use. Pocket parks are nice ideas but they are often too pokey to be genuinely useful.

Here’s a graph showing what I mean. It has distance from the road on the x-axis and pleasantness on the y-axis. Note the horizontal axis is non-linear and I argue that a park can be too big in an urban setting – once you’re too far from a road the amount of passing pedestrians falls and a park can become empty and eerie.

This is just a model of how people enjoy public space. For different people and different types of road, the shape of the curve is different Still, if the idea embodied here is true it implies that by joining together bits of public space we can make them more valuable.

Here’s how I imagine the solution looking in Willliamstown. The new roads are outlined in red. The land in the roundabout is connected to the park. You could put in a micro roundabout at the new intersection or a stop sign. The road to the south side is just a driveway into the yacht club so it won’t be too busy (the busier the road the further you’d need to be from it to enjoy your surroundings)

To get value out of this idea it makes sense to move that carpark too, turn it into parkland

People would picnic at the feet of the cenotaph and it wold be beautiful.

Creating one big chunk of park out of two little bits of park could let us wring more value from the precious limited amount of land around. Back in the day such an idea may not have been valuable because the city was less crowded and land was less precious. You could seal off a big chunk of land inside a roundabout and it didn’t matter. Now that’s no longer true. We need to treat land like we treat water and stop letting it go to waste.

There’s another roundabout I would like to point out as well where this principle could help inspire better land use. It’s much smaller and in a less idyllic setting, but it is a crowded pedestrian area with very small footpaths. There’s a cafe there with outside tables that would benefit from much more footpath space. The site on the other side was a pub and could become an even more succesful one if there was space for a few outside tables.

Clifton Hill, about 50 metres east of the train station.

This is an extremely low traffic area and it wouldn’t risk creating a traffic jam if this roundabout became a narrow tricky thing drivers had to slow dramatically for. They could close off one of the exits or entries or perhaps create a hybrid roundabout / one-way slow point.

These are just two sites where land is at a premium and a legacy roundabout is gobbling up land that could be better used. I bet there are hundreds more like it across Melbourne and many thousands worldwide. And it’s part of the larger principle that we allocate a lot of land to roads that, in some areas, could be available for pedestrians and public use, and we should be fighting to win that back.

Everyone’s excited about this chart. It shows official interest rates racing up to over 2.5 per cent by the end of the year. That would be one of the fastest interest rate rise cycles in history and would make a lot of people with mortgages rather unhappy.

Each blue column corresponds to one of the next 18 months. The height of the blue column is how high official interest rates are expected to be in that month. (You can also see that value at the bottom of the chart in the row labelled “Implied Yield”)

The chart is not one person’s prediction. Instead it uses the wisdom of crowds: the values are derived from market prices in the Interbank Cash Rate Futures market. This market has a very good recent history of prediction. Back in 2021, It was insisting rate rises were coming in 2022 when the RBA was insisting the opposite and reassuring us they wouldn’t arrive until 2023-2024. But how accurate are these predictions more generally? Where do they come from? What assumptions do they make? I did some digging.

First I contacted the ASX, who publish the above chart each afternoon. I asked them: Who trades this market? The market for Interbank Cash Rate Futures, they told me, is on the ASX24 platform, which is traded around the clock by a small number of big name brokers and investment banks – Goldman Sachs, and their ilk – who have to register. The registered users provide access to their clients, being super funds, hedge funds, etc.

Plenty of people told me they thought rates would never get as high as the predictions above and would like to bet against them by trading in this market. Inquiring minds wanted to know: Can retail traders get involved in the market for Interbank cash rate futures? The answer is there could well be retail traders – the identity of who is trading through the big brokers and banks is anonymous. Minimum contract size for interbank futures is $3 million, but on closer inspection that seems to be the face value of the arbitrary contract – when trading it you’re only up for the interest on a contract of that size: A few thousand dollars. So it seems anyone can play if they have a broker.

The ASX also told me you can see prices here with a 20 minute delay.

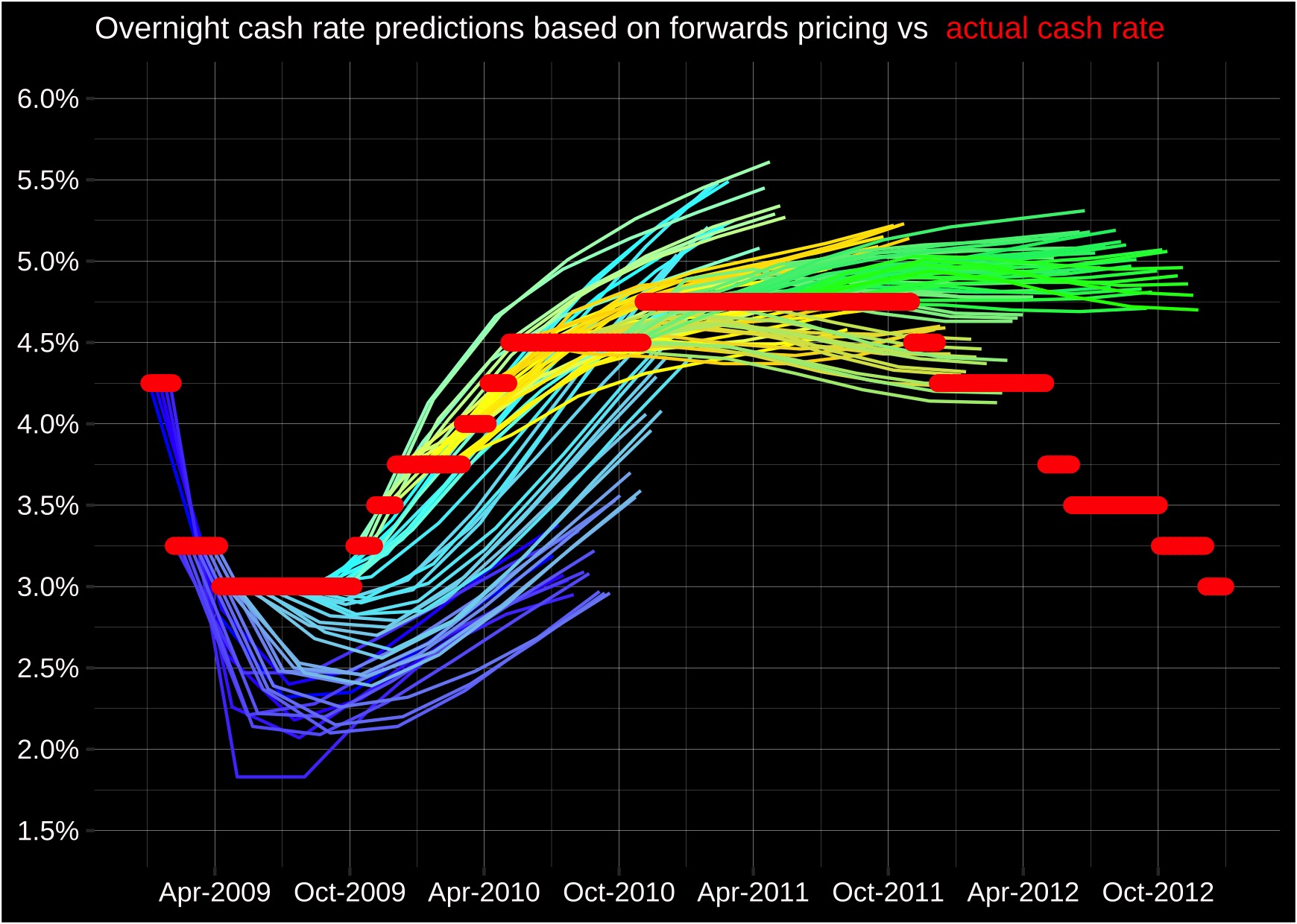

The big question: Does this market really give us the best guess of the cash rate? This chart, from ANZ, seems to show the interbank futures generating a systemic overestimate of the eventual cash rate. There is much more grey line above the orange line than below, especially for the predictions made about later months in each forecast (each grey line is 17 or 18 months long and they almost all seem to bend back up). Is that for some technical reason? Or just because in the 12-year period depicted nobody could quite believe interest rates would not turn around and “normalise”?

Obviously predictions of the later future are more affected by random error. But even when the grey lines slope down at the start, they slope up at the end. Hmm. I found a 2012 RBA paper by Olivan and Finlay – Extracting Information from Financial Market Instruments – that made me worry later months are biased upwards:

“… the forward curve gives the interest rate agreed today for overnight borrowing at a date in the future. The forward curve can be used as an indicator of the path of expected future cash rates, but importantly it becomes less reliable as the tenor lengthens because of the existence of various risk premia, for example term premia. No attempt is made in this article to adjust for these risk premia and so they will affect the estimated zero-coupon curves.”

The RBA and I corresponded and Finlay confirmed there’s probably upward bias in the interbank futures market, but how much, you could never say.

…on average you would expect term premia to be positive (and so bias up the market rate relative to expectations) and to get bigger as the time horizon lengthens. BUT as said it is hard to be absolutely sure – term premia are unobservable and can in theory also be negative.

You can estimate models to separate term premia from expectations, but you need to make a lot of (possibly implausible) assumptions, so again need to take results with some caution.

Other futures traders assured me that over 18 months term premium is not worth worrying about. Does a possible bias in the later months matter a lot right now? No. If you glance back up at the first chart in this post, you will see that the steep part of the curve is in the next 7 months, not the following 11 months. It means this: the signal the market is sending could be wrong, but ignore it at your peril.

I did more digging around in the Interbank Cash Rate futures market, and found something probably more concerning than term premium: the later months are not traded very much at all. But their price appears to update even on days when none changed hands. Quite how this works is not clear to me yet.

There’s another problem with it too: Data on the Interbank cash rate futures market is hard to find. There is no publicly available repository of historical data that I know of (ANZ obviously has it, to make that chart above, but they are not sharing!) The ASX publishes a .pdf of one day’s data every day but when the pdf updates the previous day’s data is lost forever. They also go to the trouble of making it a low-resolution image so it’s hard to collect. Ctrl+c, Ctrl+v is out of the question. You’re either transcribing it manually or using optical character recognition. Thanks, guys.

WHAT ELSE IS THERE?

Interbank futures are not the only kind of futures product you can use to predict the future of interest rates. Another is called overnight indexed swaps (OIS) (aka overnight index swaps, both terms seem to be in use.) These are a bigger and more liquid market. They can trade differently to the interbank futures, directly between parties, rather than on an exchange. That would mean we don’t have data on them. However ever since the 2008 global financial crisis, governments like to keep an eye on derivatives like OIS, so (at least some of) the trades clear through a clearing house which collects data and provides it to government.

Historical OIS data is free from the RBA so long as you want to look only 6 months in the future. (But longer data must be out there somewhere- the big London clearing house LCH will clear Australian OIS with maturities of up to 31 years!) The following chart shows two different OIS prices, which contain information on predictions of the official cash rate in one and six months time. The data shows an expectation for six months in the future (i.e November) of rates at 1.42%. That’s gone dramatically higher in the last month or two as expected, but it is also a dramatically lower prediction than the Interbank Futures market’s prediction of 2.77 per cent! Why? This confused me for a while

The reason it is lower than the other chart turns out to be that the OIS pricing is an average of the cash rate over the future period, rather than the value of the cash rate at the end of the period. You can, however, do some maths on the value and derive the value at the end of the period, called the “forward” rate. The RBA helpfully provides this in table F17. You can see the OIS forwards compared to the Interbank futures in the next chart. They’re similar but not identical!

OIS forwards are the market pricing the RBA “typically” uses as an input to their forecasts. Does their use of it suggest the OIS forwards might be more reliable? Have we finally found the one optimal prediction we should rely on? Here’s an interesting wrinkle: The RBA governor recently said they now blend this series with economists predictions.

I can confirm that we’ve used the same assumption as last time, an average of the market path and the economists’ path. And just to be specific about that, we’re assuming in preparing these forecasts that the interest rate by the end of the year is between 1½ and 1¾ per cent. And then by the end of next year at 2½ per cent. So that’s a technical forecasting assumption.

That is new!

The RBA started averaging market data with economist predictions only recently. That approach has been used in the last two Statements on Monetary Policy. They previously used pure market pricing in their forecasts. Why the change?

My first instinct is the change came because the path of interest rates predicted by the market is now terrifyingly steep and when they feed that into the models we are a good chance of going into recession. Is that possible? The next chart shows the OIS-derived forecasts published by the RBA in May 2022. It tells us, yep, the RBA’s assumptions (e.g 2.5% at end-2023) are now well below the market predictions (3.5% at end-2023).

So most likely they were forced to abandon market pricing as an input to their forecasts because it made the forecasts look terrible!

Should we be worried about the sudden desire to dilute strong market forecasts with watery economist forecasts? Maybe. The economists are likely using similar methods to the RBA – and many bank economists are ex-RBA analysts – so the amount of truly independent information feeding into the RBA’s forecast is now much lower. Two downsides for transparency in all this:

These economist predictions are not easily available. I believe they are available on the Bloomberg terminal – I remember seeing them when I used to have access to that. However it costs US$24,000 per year to subscribe (this is why Michael Bloomberg is a multi-billionaire.)

The RBA hasn’t explained why they suddenly changed methodology (or at least I have not seen an explanation) opening up space for the type of speculation seen above.

Here’s an important question: Are the OIS forecasts usually an overestimate? Could that that justify the RBA’s choice? It’s a hard question, as the next chart shows. Mostly they overshoot, sometimes they undershoot, it is possible they have a bias to predicting a return to the status quo.

If we zoom in on the last hike cycle though we see that some of the predictions made at the start of that hiking cycle (the palest blue ones) were pretty accurate, at least for the first 12 months or so. Given this, maybe skepticism of the RBA’s changed approach is warranted? Maybe rates are going to shoot up more than they think?

Of course the RBA is not at the mercy of the futures market. Official rates don’t move by themselves: the RBA makes the decisions to lift them. The central bank’s choice to not use pure market pricing in its forecasts tells us it doesn’t expect to follow that path. So what we might infer from the steepness of the cash rate futures curve and the RBA’s desire to tread a less steep path?

Perhaps that the market is wrong about what it will take to control inflation? That would be good news. Or perhaps that the RBA realises it will have to let inflation run high for quite a while to avoid recession? That would be very bad news indeed. It’s worth watching these forecasts very closely, keeping an eye on inflation both here and overseas, and watching the RBA to see which way this tension resolves.

There’s one remaining mystery in all this: Why the difference in price between the two markets for cash rate futures, Interbank and OIS? And is the difference big enough for a clever blog reader to make money by aribtraging it? Let me know!

Thanks for reading this series. Your reward for getting this far is a juicy post full of fun stuff you can use to get an edge in the lottery. I didn’t expect it was possible to play the lottery strategically, but I was wrong.

I’m excited by what I found. Some numbers will give you an edge. I’ve never seen this analysis done before and I’m not sure why. I guess anyone else who does it keeps it to themselves!

My first post explained how we fail to recognise that other people will share our lottery win, and how that ruins everything. In that post I made a simplifying assumption that the numbers people choose were all random. If we all chose random numbers, then the risk of sharing the lottery win is affected only by the number of people who enter the lottery.

But that’s not the case. Yes, the numbers drawn by the system during the Powerball draw are random. But the numbers chosen by players when they buy their tickets? They may not be random. In fact, with online purchasing, choosing your own numbers is easier than before. No need for a pencil. All our superstitions and dumb heuristics are in play here, we just need to get the data to find how they affect our number choices.

Without further ado, let’s get to the good stuff!

Note that in the title of this post I say “edge”, not “chances”. That’s deliberate. I’m not able to change your odds. Your odds of winning are given by the number of balls in the system. But I can help you change something else that matters – the amount you win if your number is drawn.

As we explained in Post One,expected value is your odds multiplied by the amount you can win. This post is about how to improve your expected value. You do so by choosing a Powerball number that other people aren’t choosing. Ones on the left of the graph above. Unpopular numbers. That means you share the prize pool with fewer other winners and take home more lucre. You can’t improve expected value by much, mind you, but you might as well lift it as high as you can!

Think of this like harm minimisation for your lottery addiction. Most of the time, playing the lottery is the financial equivalent of shooting crack cocaine into your eyeball. It’s not financially healthy. In this metaphor, this post is like making sure you’ve got a clean syringe. If I can’t stop you doing it, maybe I can help you find a way to reduce the worst of the harm.

Lucky for some…

Before we go any further, a little bit of terminology. This post is about the Powerball number. Powerball is the name of the lottery, but also the name of one of the eight balls drawn in the lottery. Seven balls are drawn from a set labelled 1 to 35, then the Powerball is drawn from a different set, numbered 1 to 20. I’m going to show you the right Powerball number to choose. It makes a difference! In a later post we will look at the other seven numbers.

CHANNEL YOUR INNER TODDLER: YOU DON’T WANT TO SHARE

Choosing lonely, unloved numbers matters. Consider this story: A friend of a friend won Division Two in the British lottery. They expected hundreds of thousands of pounds, but only won thousands. They’d chosen their lottery numbers by going diagonally across the slip. That strategy proved to be surprisingly popular, meaning when those numbers came up there were a surprisingly large number of winners, all surprisingly crestfallen.

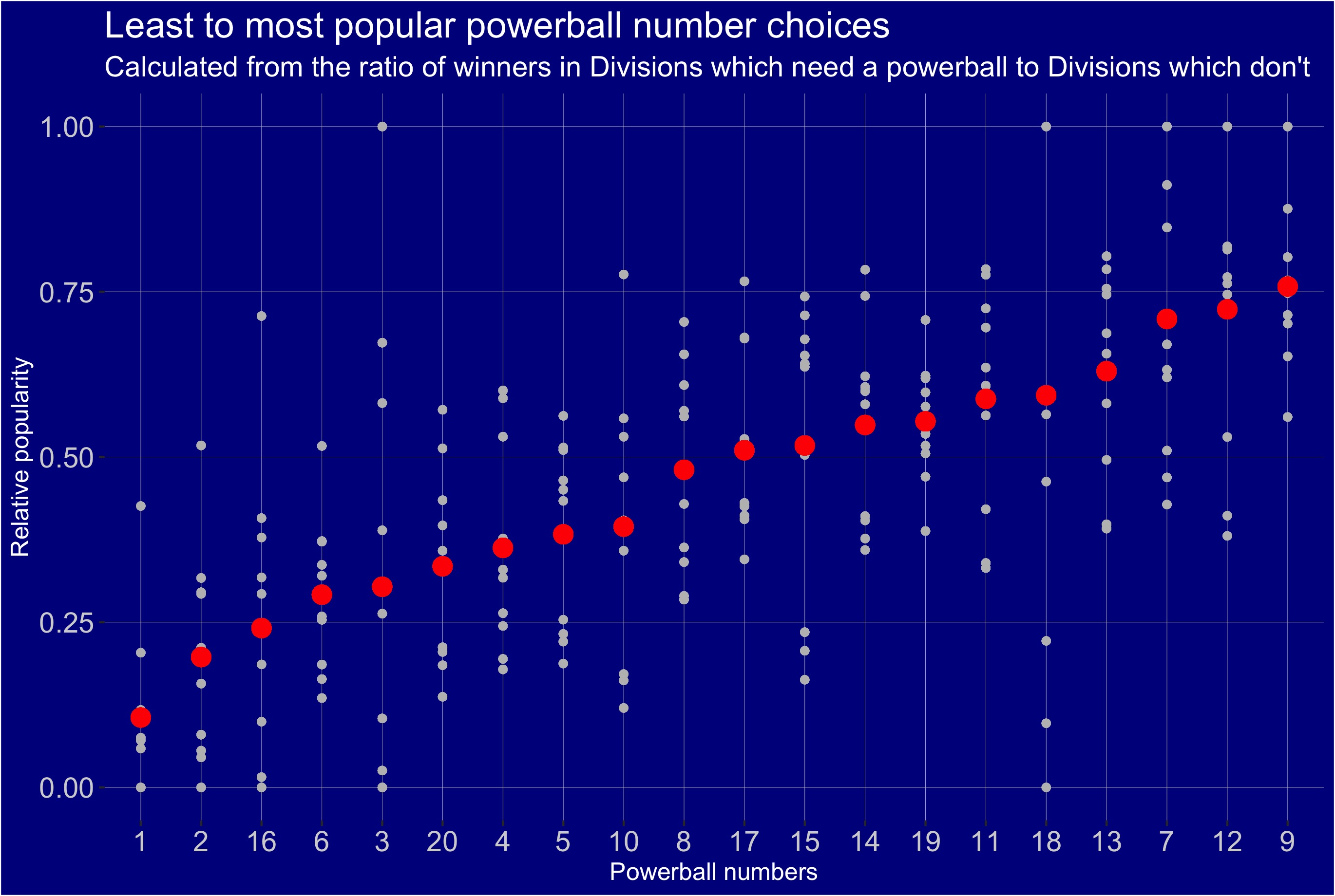

Let’s look at the key chart again, before we try to infer some lessons about what makes a number popular or unpopular.

WHAT IS SO SPECIAL ABOUT NINE? WHY ARE WE CHOOSING THESE NUMBERS?

Here are the numbers from least popular (1) to most popular (9). What does this says about the rules and biases people have when choosing lottery numbers?

I’m intrigued by the way the most popular four numbers are close to the middle of the range 1 to 20. It’s like people are using an understandable but silly heuristic – trying to minimise the size of their miss. They choose a number close to the middle. That way whether the Powerball is 5 or 15, they can say, Oooh, Close. (But not right in the middle, that doesn’t seem random enough! 10 is not popular.)

Small numbers are also out of favour relative to larger ones. The ten most popular numbers sum to 125 while the least popular ten sum to 75. Do larger numbers seem more “random” by virtue of being less familiar. And do we think more random-seeming numbers are more likely to be chosen by a random process? The human brain is a funny thing.

It’s also surprising to see 13 relatively popular and 8 lower down. This result makes me think people are actually already trying to use a version of this strategy – choosing unpopular numbers and avoiding popular ones. But absent data, Powerball players are all crowding into the same idea and negating its value!

The calculation is simple. Compare the number of winners in divisions that need the Powerball to the number of winners in divisions that don’t.

Divisions 2, 4 and 7 don’t require the Powerball to win. They provide our baseline. On any given week, if there are many winners in Divisions that don’t need the Powerball to win, but few winners in the Divisions that do need the Powerball, that might be a signal that the Powerball drawn that week was not a popular choice for players. And vice-versa.

Popular Powerballs create split prizes. For example, last week’s draw. The Powerball was Thirteen(13), a top-four popular choice. Despite a moderate number of entries, the $10 million Division One prize was split two ways, with each winner getting $5 million. Pretty crummy luck for the two winners!

There’s a lot of random variation in number choices (many people get a ticket type called a “quickpick” where the computer spits out random numbers) so we need a good sample size to have confidence in these estimates, but the maths here is not hard: No French polymaths required!

Technical note: Please consider the above graph as a ranking of popularity. I did some normalising and the y-axis does not represent absolute popularity of the numbers.

THE WHOLE NINE YARDS

The chart above is nice because solves a nagging mystery for me: back in 2019, the biggest Powerball Division One prize in history was split three ways. My calculations in Post One argued that week was the only Powerball draw in history with positive expected value, based on the number of entries. The chances of splitting the $150 million Division One prize were modest, I thought, but it was actually split three ways. Three people had the same winning numbers. Perhaps the Powerball that Thursday made a difference? It was Nine(9), the top choice.

If that week the Powerball drawn had been One(1), perhaps Division One would have jackpotted to an even bigger record!

WILL USING THIS STRATEGY PAY OFF?

I got the above numbers by maths. The real-world test is if they are associated with higher prizes. So I checked to see if the bottom three least popular numbers were associated with bigger wins.

The answer appears to be yes! The next graph shows a juicy bonus in Division 9 from choosing the least popular numbers (1,2,16) compared to the most popular ones (7,12,9).

Remember from post one that Division Nine gives you a huge chunk of your expected value. Increasing your prize by even a little bit helps.

Division 9 results 2018-2022. Vertical line is mean of prizes awarded

The same kind of result is seen for the other Divisions that require the Powerball (with the exception of Division One, because when there are fewer winners in Division One that usually means the number of winners goes to zero and the prize goes down to zero too.)

PARTITIONING

However, here we run into a question of good statistical practice. I formed the hypothesis by exploiting a dataset of Powerball draws between 2018 and now. If I test the hypothesis on the same dataset, there’s a risk I am fooling myself – random variation could be presenting itself in a way that looks like proof!

I need to test the theory on another dataset. Lucky for us, I have all the results from the old Powerball draws between 2013 and 2018. What sort of results do we see if we test the same popular and unpopular numbers?

The result is pleasing. Again the numbers that were unpopular in 2018-2022 are associated with higher prizes.

Does that mean the exact same numbers were popular and unpopular back then? If we run the same analysis of most and least unpopular numbers on that old dataset we can answer the question.

The answer is: not exactly. Some numbers appear more popular in the older dataset, some appear less popular. Nine(9) is a big mover, going from top to bottom half of the popularity charts. Perhaps people change strategy over time? I think a more likely scenario is statistical noise. But importantly there is one consistency between the two lists, and it is the most important fact: The least popular number to choose as Powerball is One (1).

That matters because the least popular option for everyone else is your best option. You want to choose the Powerball the fewest other people have chosen, and the data makes it crystal clear what the best choice is. Choose One(1). Every time.

The next graph shows the size of the increase in prize you can expect if you choose One(1) as your Powerball. (Ignore Division One, it is confounded by the prize not going off. Division Two is also not relevant as you don’t need a Powerball to win it – the result there is statistical noise.) Look at Divisions Three, Five, Six, Eight and Nine. You can expect a higher prize if you chose One (1) as your Powerball. Fewer other winners are in the mix sharing your prize.

The result in Division Nine has the least statistical nose in it and so a 7 per cent uplift is our best estimate of the upside of choosing One(1) instead of Nine(9).

Let’s assume you choose to play Powerball next week. (You should NOT ! the prize has gone back down to a miserable $3 million and the expected value is so negative it makes the Russian Stock market look like a good idea.) If you must play, choose One (1) as your Powerball. Few other people will do so, and if it is drawn your winnings will be higher.

But what about in a year’s time? How long will this edge last? Possibly, just possibly, the word will get out. If you share this post with one other person, and they share it with one other person, then over time, it might become common knowledge that the best choice for the Powerball is One (1). And when that happens, everyone will be doing it! And if so the best response will be to change. This is the literal definition of a strategic game – your best move depends on what everyone else is doing!

But remember this: if most people were smart about playing Powerball, there would be no Powerball. The opportunity to get an edge should last for a while yet!

This is post three in my Powerball series. Post One is here, on Naivety. Post Two is here, on Profit. Post Four is coming soon. In that I will look into what numbers are best to choose for the other seven numbers, excluding the Powerball.

Last week Powerball rose to a very rare $120 million Division One jackpot, and I wrote a post about why such jackpots seem so tempting but turn out so frustrating. It turned into one of the most popular posts in the 13-year history of this blog and readers told me they loved it. I was delighted.

If you would like to read it the link is here. The spoiler is big jackpots are not so great because so many people buy tickets. Even if you win, you’ve got a bigger and bigger chance of sharing the jackpot with others.

I published my post on Tuesday and the draw was on Thursday night. It might have been a popular post but it had absolutely zero effect in dissuading ticket sales! In fact, Powerball managed to sell more tickets for last Thursday’s draw than they had ever sold for any draw before. I had a model that said they would sell 175 million tickets. Instead they sold 250 million tickets. The next graph shows how far out of the usual pattern it was.

We had very little data on how many tickets would be sold for such a large jackpot. Last week I was cautious about saying there might be a non-linear relationship between ticket sales and the jackpot size. Today I can say for sure. There is one. Imagine a straight line through those yellow dots – it would go nowhere near the red one. People go absolutely bananas for a big prize.

Because so many people bought tickets (far more tickets than there are unique combinations), two people held the same winning numbers. The prize was split with the two winners each taking home over $60 million. The prize pool was greater than the advertised $120 million because so many people bought tickets and Powerball is obliged by law to give back 60 per cent of takings, so they bumped up the Division One Prize Pool to $126 million.

The amount of revenue from the most recent draw is a record: $300 million. But as you can see in the next chart, the most recent draw was not the most profitable. It is usually the penultimate draw before the jackpot that makes the lottery company the most money.

You can also see from this chart that they do sometimes lose money on the big jackpots. In particular, four consecutive big jackpots in 2020 were money-losers. Ticket sales were no doubt disrupted at that point thanks to the pandemic and national lockdown. However, no draws since early 2020 have been money-losers. We will explain why in a second, but first lets talk about where the profits go.

The profits of Powerball look too good to be true, right? In a way that’s right. Tabcorp does not keep all the money. The government benefits in several ways. For example, state lottery taxes in the state of Victoria take 90 per cent of what is lost (tax is slightly lower if tickets attract GST). That leaves the lottery company with the sliver between the red and green lines . One reason not to feel bad about buying Powerball and losing is you help fund our health system!

The real money-making weeks for Lottery companies (and their regulators!) are the ones just before a jackpot goes off. When the Division One jackpot does not go off, profits rise in a simple, predictable and very steep line, as shown by the triangles in the next graph. Weeks when the Division One Prize goes off are much less profitable.

This is probably why Tabcorp is eager to make lotteries harder to win. The data I’m using for Powerball goes back to 2018. The reason I haven’t gone back further is because prior to that, Powerball had fewer balls to choose and fewer divisions to win. They changed the rules of the game in 2018, creating Division Nine – which was easier to win – while Division One became much harder to win. The intent was creating fewer Division One wins and more jackpots.

Tabcorp is now planning to do the same to Oz Lotto, which is, like Powerball, a jackpotting lottery. Unlike Powerball, Oz Lotto is drawn on Tuesday nights and has a yellow colour scheme instead of purple. They are very different.

“We will also introduce a change to Oz Lotto that is expected to create larger and more frequent jackpots in line with its promise to deliver ‘Big Aussie Fun’,”

Tabcorp boss David Attenborough, speaking last week. (No, not that David Attenborough!)

The changes will make Division 1 “more likely to jackpot (c.40% more combinations)” Tabcorp say in their recent investor presentation. (pdf at link).

Powerball is Tabcorp’s most popular lottery, so attempts to make Oz Lotto more similar make sense for them.

In fact, the popularity of Powerball has been surging over time. This may explain why draws have been so profitable recently – and also why so many people bought tickets last week. There are more powerball players now than previously. Tickets sold each week have risen a lot, and they rose especially during 2020. People were stuck home and bored and had, thanks to the various fiscal supports, money to burn.

If you buy Powerball tickets when the Jackpot is $3 million you are incinerating your money. Stop it!

The yellow lines go up, but then they seem to stall a bit. Hot demand for low levels of Powerball may have cooled in 2021-22, which is a tantalising explanation for why the jackpot rose so high recently. A climate with fewer ticket buyers lets the jackpot rise.

It’s a paradox that the more people pile in to the low levels of Powerball, (e.g. selling 45,000 tickets for a $20 million Division One prize pool instead of a mere 25,000 tickets) the lower the chance of the prize rising to a level where Powerball might sell 250 million tickets. And make no mistake, they like those long sequences of jackpots. Once they’ve made OzLotto harder to win, Tabcorp might be tempted to come back to Powerball and do the same thing to it.

Part Three is about Strategy. It is coming soon and concerns the burning question of whether you can do better by choosing numbers other people aren’t choosing (yes you can, and I will demonstrate a way to work out what those numbers are. )

POST STATUS: Lot of calculations below. Still early days in the checking process. Could be errors. Caveat emptor!

—

This Thursday’s Powerball has a $120 million Division 1 prize pool. It’s huge – the second biggest Division One prize in history. Over 175 million tickets will be sold, at a total cost of $213 million, equivalent to seven tickets for each living Australian.

But should we play? The answer might surprise you. There are three main levels of Powerball naivety, and then one bonus level.

DADS AND ODDS

I care about Powerball mostly because my dad plays it now and then. He’s an educated man with a successful career behind him, but likes the idea of a big prize.

The first thing to know is the odds of winning Division One with a single entry are small. Really really small, as the next chart shows. Division Nine, by contrast, is up for grabs.

Powerball is owned by Tabcorp and each week they lavish a lot of attention on the Division One prize, but it is not given away each week. Far from it.

DIVISION ONE DROUGHT

The last six draws have all gone by without a Division One winner. Such streaks are not uncommon. Around three-in-four draws end without anyone winning Division One and so the big prize is won roughly once a month:

Division One was won:

10 times in 2019,

14 times in 2020, and

13 times since the start of 2021.

The next chart shows grey lines when the Division One prize was not won, and jackpotted to the next week.

This matters, because the prizes underneath Division 1 are nothing to write home about. Division 9, which you have a one-in-66 chance of winning, averages just a smidge over $10. As the next chart shows, even Division 2, which you have just one chance in seven million of winning, regularly pays out a middling $100,000. Often even less. Most of these other prizes are simply not worth getting excited about.

It’s all about Division One.

The jackpot structure of Powerball makes each week different. Which got me thinking. Maybe, just maybe, Powerball could sometimes have positive expected value. Right? They do a bunch of draws where the Division 1 prize doesn’t go off. Those must have been very profitable. Perhaps that’s how they make their money? And if the prize builds up high enough, to a high jackpot, those weeks could have positive expected value for a player. Maybe, if you played only in certain circumstances, you can expect to come out ahead, on average?

EASY VICTORIES: KNOW YOUR EV.

We need here a very brief introduction to the concept of Expected Value, which I will call EV. It’s a tremendously useful concept, and a simple one: Your expected payoff is the chance of winning multiplied by the payoff. And the expected value is the expected payoff minus the cost.

For example, if you give me a $2 prize for calling a coin toss correctly my expected payoff is $1. If you charge me $1 a try, my expected value is zero. If you lift the prize to $2.10 , my expected value turns positive.

Knowing EVs is really powerful: They tell you what to do. If an EV is positive, you should play that game or do that thing as much as possible. If they are negative, you should run away.

You have a negative EV if you play roulette at the casino. At Roulette, the combination of the chance of winning and the prizes are designed to give the player a negative EV and the casino a positive EV. It’s a great game for them, in the long run, and a terrible game for us. If you repeatedly play games with negative EVs you will end up losing big.

The EV concept is applicable to real-life situations too, not just games. Investing well depends on estimating EVs, for example, and different postgraduate degrees might have different EVs too. You can extend expected value to any domain where chance or uncertainty is present.

For us, the EV is the main thing we need to know to decide whether to play Powerball. (Assuming, for now, you don’t just love the anticipation of holding a ticket in your hand and setting your mind free to dream).

GETTING RICH ON THE LOTTERY?

How do we figure out the expected payoff of a Powerball draw? Let’s look at the smallest draw this year, with a $3 million Division One prize. For a rough estimate we can simply multiply the odds of winning each division by the prize. The next chart shows the results of that calculation.

As you can see, Division 9 is doing most of the heavy lifting here. Your one-in-66 chance of getting back around $10.20 is worth a little over 15 cents. The one-in-134 million chance of winning $3 million is worth only 2.2 cents!

After you subtract the $1.21 cost of entry the EV is very very negative. You definitely shouldn’t play for such a small jackpot.

WHAT ABOUT THE BIG PRIZES?

With a bigger Division 1 Prize, maybe your EV goes up? Sure does. Once again we use a simplified technique – multiplying the chance of winning by the advertised prize. Lo and behold, the higher the prize the bigger the expected payoff.

This is a potentially exciting graph if you’re not careful.

Because the next draw, this Thursday, has a Division One prize of $120 million. That would seem to change things. A one-in-134-million chance of winning $120 million is worth 89.5 cents for Division One alone. The lower divisions are consistently worth about 40 cents of expected payoff. Add those to the 89.5 cents and you have an expected payoff of $1.30 – higher than the cost of the ticket! The EV looks to be positive.

“IS IT WORTH PLAYING THIS WEEK?!”

A few years ago I found myself asking this exact question about a Powerball draw with a big Division One prize. My back of the envelope calculation told me the EV was positive and I should play.

What I soon learned is if multiple people win Division 1, they split the prize. Your odds of getting a winning ticket are the same, but if you share it, your payoff is split. As the next chart shows, Division One has gone off 34 times in the last few years, and it has been shared between multiple winners on 4 occasions.

Here’s the problem:

The number of tickets sold rises as the Division One jackpot rises. And the higher the number of tickets sold, the more chance of multiple division one winners.

You can see the effect in the chart above – three of the seven largest Division One prizes had multiple winners. So the simple calculation I was using above – chance of winning multiplied by advertised prize – is misleading. It’s wrong.

It doesn’t take into account the risk someone else out there has the same winning numbers, is there for your giant cheque ceremony, steals your limelight, splits your pot and rains on your parade.

Check out the $150 million prize in 2019. You think you’re playing for $150 million – the good people at Powerball HQ encourage you to think that – but as lightning strikes and the one-in-134-million chance you have the winning numbers becomes reality, you also discover your lusted-after prize is actually a mere $50 million. (Sure, $50 million is nice, but it’s no $150 million, is it?)

THE THRILL

This is the point that got me really excited: I wanted to quantify this. If there is a relationship between advertised Division One prize and the number of tickets sold, and a relationship between tickets sold and the odds of multiple winners, could we therefore calculate a more realistic EV for each draw? I wanted to do this ever since the $150 million jackpot back in 2019, but it was only this year – once I learned to use R – that doing so became possible.

I scraped data from the internet that let me calculate the number of entries in every Powerball draw in the last 20 years. Here’s data from the last four years, showing that entries rise dramatically when the Division 1 jackpot rises. The red line is a model of a linear relationship.

Is that red line satisfying? Not really. Might the relationship be non-linear? Maybe! The yellow line in the next graph is a smoothed version of the points.

Your chances of splitting Division One go up and up the more people enter. And that changes everything.

THE THREE LEVELS OF NAIVETE

There’s three main levels of Powerball naivety here.

One is not realising the pot can be split if multiple people have the winning numbers.

The second is not realising the positive relationship between tickets sold and Div 1 prize: Just because multiple winners are rare, doesn’t mean they won’t happen for the big prizes!

The third one is not recognising that the relationship is non-linear, so your chance of splitting the prize is rising most dramatically when the jackpot is highest .

This latter point is important. Powerball draws with Division One prizes below $110 million can’t possibly have a positive EV. The odds are too bad and the prizes are too low. But draws with high Division 1 prizes – such as this week – could in theory have positive EV. The bend in that yellow line may be helping prevent that theory from becoming reality.

DOING THE MATHS

The maths here were tricker than I first realised – I only solved it after cracking out the Poisson distribution. The odds of winning Division One are low. But enough Australians buy Powerball tickets that when the prize gets big, there’s a strong chance of multiple winners.

This graph shows exactly that. Pay attention to the falling white line – that’s the odds of nobody winning the jackpot, and it dips below 50% when the jackpot is around 80 million. When the Division One Prize is just over 100 million, the odds of there being one – and only one – winner peak. After that they are falling. Somewhere north of $150 million the odds of there being 2 winners will be greater than the odds of 1 winner.

This chart also reveals that the $150 million Division One prize pool from 2019 that was split by three people was actually a little unusual. The odds of there being three or more winners that day was only a little over 20 per cent. It was actually more likely to jackpot than be split by three people. Just a good reminder that the odds aren’t everything!

Just for fun, here’s the odds of multiple winners in Division 2. I include this graph because it shows even more clearly how the chance of a division having a small number of winners dissipates when the prize gets high. (And also because it looks cool and swoopy.)

Your odds of getting the winning number don’t change when there are multiple entries. But your expected payoff from getting the winning number does change.

As more people enter the lottery, your EV must fall. This is not the kind of lottery where you can trust your instinct (and this is perhaps the most important reason for this blog post – to help people overcome that instinct!).

FATAL INSTINCT

The way entries rise with the Div One prize pool suggests some people may be taking that instinctive, naïve view. The higher the jackpot, the more this matters – the more the naïve view takes you further and further from the reality. This week, for example, with the high prize, knowing you may split the pot is more important than ever. The expected number of winners is 1.3, meaning a hefty chance someone else will have their mitts on your novelty cheque.

I set out to calculate the true EVs given the odds of sharing the prize.

I spent ages hoping the highest EV would be for a Division 1 prize that was not a record high, rather than the highest one. I wondered if there was a tipping point where so many people entered the lottery that despite the higher jackpot you had extra reason to stay away. Perhaps the sweet spot with the least-negative EV would be $120m or so. That would have been a cool, counter-intuitive result!

But no, the dominant factor in the EV remains the Division One prize (at least at the prize levels we have seen offered so far). As you can see in the next graph, the $150 million prize back in 2019 (orange bar) is the one with the highest expected value.

Notice something? Even accounting for the chance of multiple winners, that $150 million draw had positive EV!

So here’s the final bonus level of Powerball naivete: scorning lotteries altogether. It’s a good reminder to keep an open mind. If this week’s Powerball jackpots (probability of there being no winner is ~ 27%) next week could (maybe, just, barely) be worth playing.

HOW MUCH DIFFERENCE DOES IT MAKE TO ACCOUNT FOR MULTIPLE WINNERS?

At the lower jackpot levels, not much. The gap between the naïve EV (simply multiplying the odds by the advertised prize) and the true EV is highest for the bigger jackpots. Which may be why many people respond so strongly to higher jackpots – they are using a naïve estimate of their EV, failing to realise – as I once did – that the prize can be split.

This next chart shows how the naive EV and true EV diverge:

For this Thursday’s draw, we can expect 175,000,000 entries, some of whom may naively suspect their EV is higher than the ticket price. But actually it is lower, because the expected number of Division One winners is 1.3. That eats away at the Division One prize you can expect to take home.

WHO WANTS A JACKPOT?

The lottery company really wants the prize to jackpot. Not just because their profit on this week’s Powerball draw is $120 million higher if the prize does not go off! After all, they do need to send that prize on to next week. What they crave is the free word of mouth that comes with an even bigger jackpot next week.

I guarantee there will be Powerball mania next week if this week’s draw jackpots and they can offer the biggest prize in history. It will be on the news, people will be whispering about it at the watercooler, and newsagents will have their first reason to smile in years.

I also hope this Thursday’s Powerball jackpots. Because then we can collect more data on the number of tickets sold when there is a $150 million+ prize! There has only been one in history and I’d like a bigger sample.

Could it jackpot twice more? The chance of a $150 million prize jackpotting is so low it hasn’t happened before. There have only ever been three draws with a Division One prize over $100 million and they have all been won. We don’t even know what the prize level above $150 million would be. $200 million? $180 million? Something else?!

WHAT YOU SHOULD DO NOW:

I remember one drunken night at a Chinese restaurant being cajoled to join a Powerball syndicate for a huge jackpot. The memories of the details are dim but the memory of the excitement is vivid. We didn’t win though. I think people get genuinely revved up when powerball ticks over $100m, and they go buy tickets.

If your mates are trying to convince you to join them in buying a ticket this week – and you don’t want to waste your money – please feel free to send them this post. “If we all hold off buying this week,” tell them, “the chance of a jackpot is higher! Let’s wait for next week…”

—

POSTSCRIPT. All this was done in R. R is the major source of my nightmares a free open-source coding language for doing statistics and making graphs (and a few other tricks).

I’m what they call “self-taught.” That term may sound cool but what it means is a huge number of people taught me, rather than just one. I owe massive debts to generous people whose advice and counsel I found on Stack Overflow, Twitter, Runapp, Youtube channels and blogs. Thank you. Errors are mine.

Code is posted on my Github. I’m still in beginner mode and very open to feedback on the code – please feel free to take a look and add yourself to the huge group of people who’ve helped me learn .

This entire series of posts rests on the claim we did. Yet memories of the Spanish Flu – also known as the Great Flu – exist. Obviously they do. The disease has a Wikipedia page. Science is still studying it – in 2018 a special Spanish Flu edition of the American Journal of Public Health came out, in honour of its 100-year anniversary. It even has a couple of references in pop culture. The book Pale Horse, Pale Rider, is about the ravages of the 1918 flu.

So how can we say that the flu – which killed as many as 50 million – was forgotten?

To answer this question, I got on Zoom with Professor Guy Beiner, historian and the pre-eminent global expert on forgetting. The conversation was a delight and I can tell you Beiner is an absolute treasure. Employed by the Ben-Gurion University of the Negev in Tel Aviv, (and perhaps the only owner-operator of an Irish accent in the neighbourhood) his specialties are three-fold: Irish history, memory, and the Spanish Flu.

Professor Beiner and his very nice Zoom background.

Northern Ireland turns out to be an excellent place to study forgetting, because a lot of protestant residents were part of a big rebellion against the British in 1798, but that aspect of their history is now not publicly mentioned.

But Beiner’s big focus when it comes to forgetting is the Spanish Flu. He is no recent devotee to the question. He tells a great story of meeting a publisher for drinks in New York in December 2019, and pitching a book on his life’s passion, the memory of the Spanish Flu.

“It sounds promising but will there be a readership for this?”, he recalls the publisher asking. “Three months later I get an email, ‘Why isn’t this book here already?!’”

Beiner likes to find the exceptions and the nuance. To make things complicated. This is how he started our chat:

“On the one hand it’s an easy case to make the case for the amnesia of the great flu. You’re in Australia, you’re in Melbourne, you have that massive ANZAC monument, pyramid-like structure [he means the Shrine!] … The huge culture of remembering ANZAC in Australia, compare that with the great flu, there’s nothing. You won’t find one monument to the great flu – or you look around you’ll find a couple, but you wont find any major monument… You won’t find any museums, you won’t find any remembrance day, you won’t even find the most banal thing! You won’t find one stamp commemorating the dead of the flu, right!? So if there’s collective memory, this is collective amnesia.”

The Shrine, Melbourne.

But then he complicates the narrative.

“I don’t like the term collective amnesia, it’s too easy… Memories had been there but they didn’t have the chance to surface.”

After wrestling with the way in which society deals with aspects of history, Beiner invented the concept of “social forgetting.” And social forgetting is not the same as private forgetting. Memories don’t die immediately, and that’s very good news.

Professor Beiner told me about a historian who puts ads in newspapers asking for stories of Spanish Flu, and laboriously visited people in their homes and recorded their stories one at a time.

“People remembered, they just needed to be asked,” Beiner said. In other words, the memories were there, like a great aquifer beneath the surface, but without public remembrance they lacked a well-spring, lacked a way out.

Incidentally, it occurred to me the historian mentioned would have saved a lot of time if he had the internet at his disposal. One could attempt a project of eliciting memories online at a fraction the effort. I gave it a go. My first shot looked like this.

Eleven thousand upvotes and over one thousand comments!

(Yes the two posts are basically identical in content – but not in form. Never underestimate the importance of re-writing to make an idea catch on!)

The volume of memories elicited by one Reddit post is impressive. The other notable thing is their level of detail. Primarily, these stories are bare outlines. One sentence or two. For example, “My great grandmother died of it, and my great grandfather remarried to her identical twin.”

Imagine the intensity and richness of that series of events. The scorching emotion and the familial repercussions. Yet what remains of the memory is skeletal. That’s how memory looks when it has decayed substantially. If we had asked for war stories, by contrast, it is likely far more richness of detail would be on offer.

There’s a lot of public war history out there to tap into. The Australian government, for example, maintains an enormous website to help people find the war records of their family members: https://discoveringanzacs.naa.gov.au/ It is an extremely impressive bit of infrastructure and well worth digging into if you’ve got ancestors who went to war.

No such system exists, it goes without saying, for archiving and preserving Spanish flu memories. The absence of flu memorials is not just an Australian oddity, it is systemic and global. Despite the millions of lives lost – more than were lost in world war one – it is not something we’ve set about remembering. At our great cost.

War memorials – they are everywhere.

WHAT IS COLLECTIVE MEMORY?

Memories are personal. They sit in the brain. But memory is not just about the endurance of sparks in the old grey matter.

The godfather of the concept of collective memory is a Frenchman named Maurice Halbwachs. One of those polymaths who seemed to crop up in Europe 100 years ago or so, Halbwachs had big contributions in statistics and philosophy but his most enduring intellectual legacy is the idea of collective memory.

Halbwachs followed Emile Durkheim in rejecting overly individualised accounts of how society works. His favourite hobby was to stir up the psychologists.

“ …one is rather astonished when reading psychological treatises that deal with memory to find that people are considered there as isolated beings,” writes Halbwachs.

His ground-breaking ability in statistics gave him unique insight into how social context affected individual outcomes. He could see the patterns in the numbers and took a great interest in the collective. When he began applying this collective approach to questions of memory, he was alert to the way society affects memory:

It is absolutely the case – even the psychologists agree these days – that memories must be retrieved to be refreshed. The more opportunities there are for retrieving memory, the longer the memory endures. ANZAC day and Armistice day and the thousands of war memorials around Australia help us keep the war(s) alive in our memories.

The past is partly buried, but it holds up the future

The lack of public memorialisation is vital to the forgetting of the Spanish Flu. Forgetting is baked in by a public realm that has until recently acted as if the Spanish Flu never happened. Our collective memory of it has for the last century been a pale and sickly thing.

(Halbwachs, by the way, was sent by the Nazis to Buchenwald concentration camp in 1944, at age 68, and died in there. We will come back to his legacy in a future post on memory and war.)

GOING PUBLIC

There’s an important caveat on the above discussion about private memory and social forgetting. Private memories can become public. The Reddit thread above is, it occurs to me now, an example. A thousand flu stories were just transformed from private to public.

It is absolutely no coincidence this is happening now, as covid viruses are tearing into lung tissue around the world.

Recurrence is major way old disasters are remembered. When a cyclone hits Mauritius, that’s when previous cyclones are discussed, for example. When a flood hits Brisbane, conversation turns to previous floods, and the TV channels show old footage, etc. Another example: According to Google Scholar, a disproportionate 17 per cent of all papers written about the Spanish Flu were authored in the last two years

One big thing that stopped Spanish Flu from being forgotten even more profoundly? The AIDS crisis in the 1980s. As Alfred Crosby writes in the introduction to the second edition of his book The Forgotten Pandemic, it sparked renewed interest, and book sales.

“For some of us, the malady recalled to memory what the Surgeon-General of the United States Army Victor Vaughan, had written about the peak of the 1918 pandemic: “At that moment I decided to never again prate about the great achievements of science.” – Alfred Crosby on AIDS

Crosby’s book came out in the 1970s, and sold very few copies. But it did have an impact.

“It starts the historiography of the flu,” Beiner says. “There were a few books before that, but after Crosby, that’s when historians start noticing the flu… It starts a trickle. Some PhDs begin appearing after Crosby, he’s a landmark in many ways.”

That was in the late 1970s. Crosby’s book was reissued by the publisher in the 1980s, and sold fast. The reason was AIDS. The pandemic created a newly receptive audience. The same happened again during SARS in 2003. New pandemics lifted public interest in the old, and what little material existed memorialising the Spanish Flu became of vital importance, bringing old private memories to the surface.

Whether things are remembered or forgotten is not static. Obviously individuals forget. But for society memory can move the other way. If we try – if we want to – we can remember things that are previously forgotten. We can reverse social forgetting of floods and storms, wars and even genocides, so long as the private memories remain alive. And doing public memorials will strengthen those private memories.

We can stop the process of social forgetting that Guy Beiner describes and make these memories vivid and relevant. And, importantly, heed their lessons. The world is doing that with the Spanish Flu right now, which is good, but might it be coming just a tiny bit late?!

That’s why this topic is so important. If we can learn how society forgets, how it errs, how it stumbles into the same traps again and again, we can – hopefully – start remembering before it’s too late.

How do we remember? Stories. Since forever. Long before TV. Long before books. Humanity is hard-wired to LOVE stories, and pay attention to them.

In recent history, one story stands out. An epic narrative that gripped the west, the English speaking world in particular. Including parts of the world that have, incidentally, done a terrible job of handling the pandemic. Game of Thrones.

George R R Martin has sold around 100 million copies of his book series A Song of Ice and Fire. The television adaptation – Game of Thrones – drew up to 20 million viewers. That’s for each episode, when it was shown live. Total viewership would be in the billions. This narrative had reach, it had impact, it was celebrated: The TV show won more Emmy awards than any TV drama ever and regularly tops the list of best TV shows of all time. In the decade preceding the pandemic, it was the dominant piece of popular culture.

So what does this very long story have at its heart? A forgotten disaster.

Now, why did we need this again?

The fictional world of A Game of Thrones is centered on Westeros, a land with a big wall at its north. A wall – 200 metres high – separates the kingdom from badlands beyond. The story opens “beyond the wall,” where we discover a terrifying enemy is rising. An invasion force this society faced before, but to which it now pays scant heed.

Has the society of Westeros been investing in its defences? Oh no it has not. Once upon a time the wall boasted an enormous force, no longer. The wall has nineteen fortresses and towers but these days only three are staffed. Furthermore, the recruits into the force – known as the Night’s Watch – are the dregs of society, supposedly criminals given the opportunity to join instead of being sentenced to death.

This is the set-up. Thousands of pages of gripping narrative ensue, dozens of hours of extremely expensive premium television, lovingly shot on location. And the tension that illuminates the whole damn thing is that of a pantomime:

The frustration where the crowd yells “He’s behind you!!” and the actor looks over the wrong shoulder? Not seeing the threat that is totally obvious? This iswhat powers the book series A Song of Ice and Fire and the TV series A Game of Thrones.

The kingdom of Westeros lavishes attention on power plays and assassinations – and gives thousands of lives to internecine wars – while vigorously ignoring desperate warnings that an existential threat is building.

Palace intrigue. Oooh Shiny!

The watchers on the wall are out of sight and out of mind for the decision makers, who live at the opposite end of the kingdom. Few powerful people have ever visited the wall. When one does, it is a surprise. That happens right at the start of the story, and notably the powerful person who makes that visit, (Tyrion Lannister, brother of the Queen) becomes a hero of the book.

The Night’s Watch use the surprise visit to make a request for additional help. Which is ignored. Its inability to raise much in the way of manpower is a consistent theme of the story. Even the organisation itself seems to have experienced strategic drift. It is now focused on repelling attacks by humans who live on the far side of the wall. The folly of this is apparent to the reader, but eventually, deep in the narrative, in book forty-four or something, Martin also spells it out:

“The Night’s Watch has forgotten its true purpose …. You don’t build a wall seven hundred feet high to keep savages in skins from stealing women.”

Which is to say: there’s a bigger threat than the one we are focusing on. What’s interesting about the White Walkers – this invasion force that is building, is the parallels with disease. They share similarities with zombies and can easily be read as a metaphor for infection.

So Game of Thrones is about a society that ignores its own history and warnings. Of course, it is about our society too, our petty spats and pathetic attention spans that mean we forget what matters and focus on what excites us. We run down our defences until it is almost too late. We take the bearers of warnings, and laugh at them. We let a pandemic run riot.

WINTER IS COMING

There is one clan in the book that warns of impending doom. The Starks. Their motto: Winter is Coming. They’re the main heroes of the book, and – I hope I won’t spoil the story too much here – few Starks get to have an especially lovely time of it.

Stark, adj. providing no shelter or sustenance. “A stark landscape.”

Now, what’s clever about the fictional world author George RR Martin has created is that winter is unpredictable. It comes when it pleases, lasts for an unknown amount of time. Winters are frightening. Some are brief, few are harsh. A pareto distribution. Then every so often – just like quakes and fires and floods, volcanoes and recessions – a really big one comes.

“Thousands of years ago, there came a night that lasted a generation. Kings froze to death in their castles, same as the shepherds in their huts; and women smothered their babies rather than see them starve, and wept, and felt the tears freeze on their cheeks… In that darkness the White Walkers came for the first time. They swept through cities and kingdoms, riding their dead horses, hunting with their packs of pale spiders big as hounds.“

This story is told by a character named Old Nan. She’s a fulltime childcarer. She has no status, meets with no powerful people. But this story – not told by anyone else – is one of the most important warnings in the entire narrative.

Her story – a kind of oral history if you like – has apparently been passed down for thousands of years. Of course, truth is stranger than fiction. If you write a book about a society that has forgotten its history, you must put in hundreds of generations between the last disaster and the present to help readers believe it is forgotten.

But of course the last huge global pandemic was in some people’s lifetime. In real life, we apparently discard memories and lessons of the last disaster rather sooner.

“If we forget where we’ve been, what we’ve done, we’re not men anymore. We’re just animals.” – Samwell Tarly, A Game of Thrones.

A bit over ten years ago, the city of Brisbane flooded. It was a major event. I watched a lot of news that week, and they played and replayed this amazing video. It captures one perspective on the floods, from a town just outside Brisbane.

The 2011 flood was the costliest flood in Queensland history – but not the biggest. A flood in 1974 had brought higher water levels. The incredible urban growth in the intervening years, however, meant 2011 was a bigger deal, affecting more people.

We learn a couple of surprising things about memory from this event.

First, the 1974 floods helped save Brisbane from even worse in 2011. One of the good things about the flood was the small amount of warning authorities were able to provide of imminent rising waters. (Albeit not enough to save the cars in the above video!)

Before the flood peaked, news media was able to warn local residents. An episode of current affairs program 7.30 aired before the waters peaked. Presenter Leigh Sales: ‘Even with the emergency response in full-swing, some experts in disaster management believe it’s not too late to learn lessons from the devastating floods of 1974’. The segment interviewed a survivor of 1974, and others.

I thought whether or not an event is publicly and widely remembered would be set in stone at the time of the next disaster. But that is not the case. So long as records exist somewhere, so long as memories are held by private citizens, they can be flushed out and made into public memories Another example: the ABC in Brisbane got people to send in photos of flood markers and flood memorials from the 1974 event – many of which were unobtrusive, mousy little things you’d easily miss – and collated them on a digital map in Brisbane.

One of the tenets of disaster memory is that memory of old events is re-activated by new events. You can see this in the very blog you’re reading – the obvious reason I’ve become focused on memories of Spanish Flu is the current pandemic!

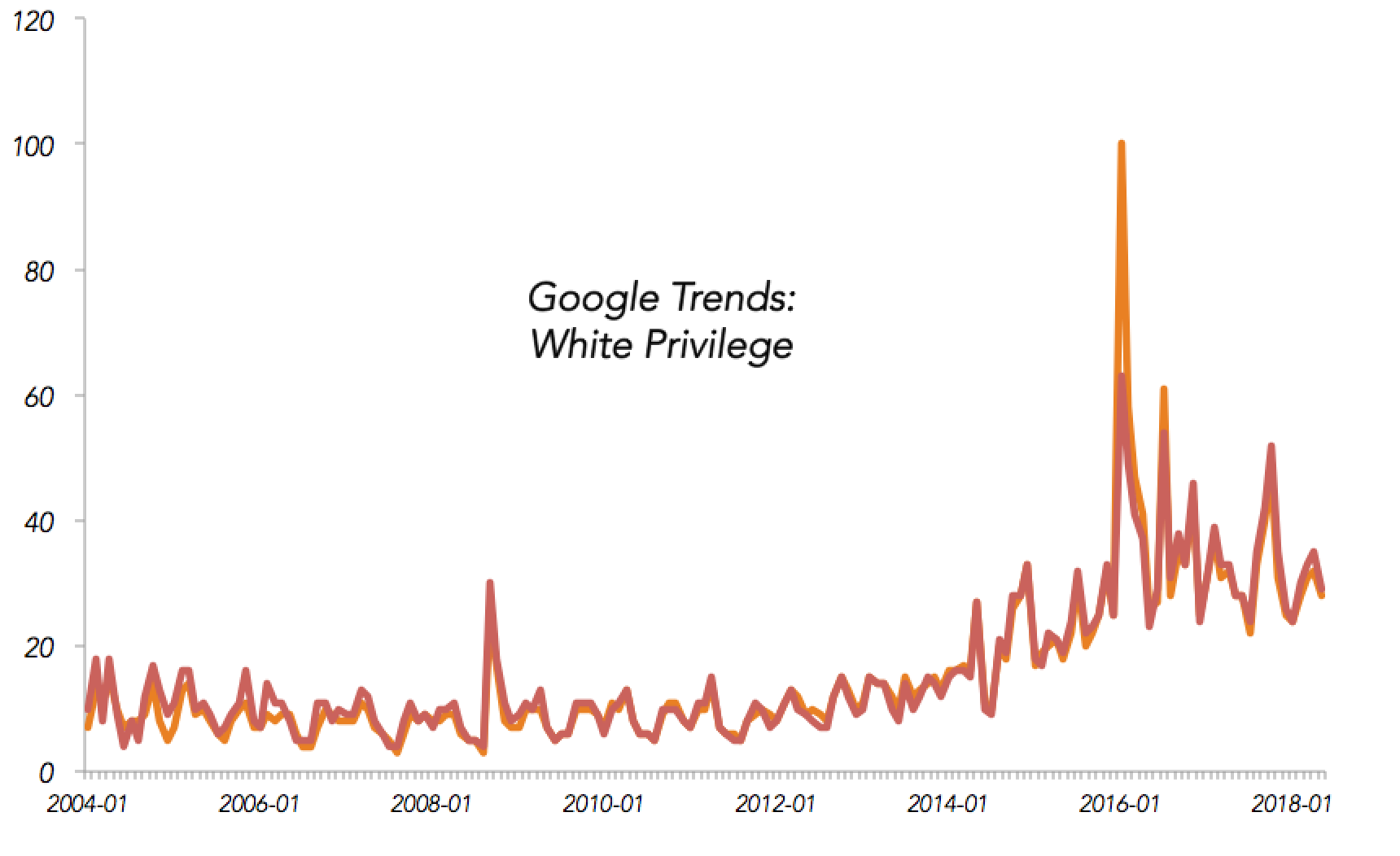

This Google Trends data shows the same thing – Spanish Flu emerged from obscurity to become suddenly a scorching hot topic in 2020.

The historian whose work I’ve relied on for understanding the Brisbane Floods is Scott McKinnon. His paper “Remembering and forgetting 1974: the 2011 Brisbane floods and memories of an earlier disaster” is brilliant. Here’s a great quote from it:

“Sally and her partner, Jane, for example, lived in the ground floor flat of a two-storey and two-home dwelling. Their actions in the flood were largely determined by the memories of a neighbour.

“A lady across the road, Margaret, was in the ‘74 flood and she came over and said, “If it’s going to be worse than ’74, you girls have to get out, or else be up top and get everything you can up”.”

Sally and Jane were shocked into action, and despite being trapped, survived.

Memory matters. It helps determine how we respond to the next disaster. We can reactivate memories. This is why it’s so important to understand how we forgot the Spanish Flu. But as McKinnon points out, our memories are not always helpful.

HISTORY IS WRITTEN BY THE VICTORS

You’ve probably heard the expression. This – it turns out – is true not only of wars but, in a strange way, of disasters too. History is written by survivors. In Brisbane, the memory of the floods is of triumph over adversity.

“I want us to remember who we are. We are Queenslanders. We’re the people that they breed tough, north of the border. We’re the ones that they knock down, and we get up again.” Queensland Premier Anna Bligh.

McKinnon’s whole bit is digging out the memories that are excluded by this way of looking at history. The marginalised communities. The people who died. The ones who got PTSD.

This really speaks to me because I am fascinated and appalled by war stories that involve a narrator who survives against terrible odds. I have been since I read about Roald Dahl’s ludicrous run of good luck that led him to survive World War 2 and go on to be an author.

His story is survivorship bias at its most obvious, but it is there in every war story. Actually, all the stories we hear are survivor stories. People who die in wars, people who die in disasters, they don’t get to tell a story. Their story can be told by someone else, but we never hear their perspective

“It was horrible, but somehow we survived,” people say. Somehow the city survived, somehow the country survived. The thing that survived is abstract – but lots of very real things didn’t survive at all. The “somehow we pulled through” narrative emphasises what endured.

This statue in Lisbon honours King Joseph I’s response to the Great Earthquake of 1755, which opened up 5-metre wide cracks in the earth and killed 30,000-40,000 people.

McKinnon cites renowned memory researcher Astrid Erll: “Things are remembered which correspond to the self-image and the interests of the group’. This is the second major lesson of the Brisbane Floods.

We make public memories that make us feel comfortable and reassured, ones that don’t make waves.

I never imagined this when I dived into learning about disaster memory. It’s not just time that kills memories, such that they die off slowly over time, it’s not just convenient narratives either. It’s power. Oh shit.

“What should we remember about ourselves?” is arguably the question that sparks the culture wars. Once you start thinking about this, it is strange how memory is at the forefront of culture war topics. It could be pulling down statues, or re-naming parks. It could be a Prime Minister objecting to a “black armband view of history”. It could be a major journalistic effort like the 1619 project, which aimed to give new perspective on the history of the USA.

In a way I’m horrified by this – I wanted to write about volcanoes, not the bloody culture wars! But the more I look at it the more I can’t deny our identity is formed by remembering certain bits of the past and forgetting others. Which is affected by who has power. It’s not the only factor but you can’t address collective memory without thinking about it.

When we make collective memories about disasters we need to be aware of the fact that they are also affected by these powerful forces. Even in the context of something seemingly apolitical, like a flood, this happens. The ten-year memorial video made by the ABC, for example, focuses on the rescuers – the heroes – and concludes with a rescue technician talking about a letter he got from someone he rescued. “That’s probably one of the things I cherish as a memory of that day,” he says.

It’s a nice note to end a video on. But is the rescuer the most important thing to remember about the floods? Is it the sort of memory that will make us change? Or is it just a memory that makes us feel safe and comfortable? As McKinnon puts it, one of the way we create memories of disasters is as “successfully negotiated moments securely located in the past.”

It’s over, it’s finished, we handled it, we don’t need to worry about it.

Such memories discourage people from rocking the boat. Which is exactly the way of thinking that meant we weren’t ready for Covid-19.

“We believe that if an event is historically significant – if it affects many, many people, if it changes the fate of countries in the world, if many people die from it, it will inevitably be remembered. That’s not at all how it works.

We go through earth-shattering disasters. Ones we can learn from. Afterwards, we forget the disasters and throw away the lessons. When the disaster happens again, we are flabbergasted. We throw our hands in the air. The word unprecedented issues incessantly from our stupid mouths. Millions of people die.

We need to learn from the pandemic. But the lesson of the pandemic is not to prepare for pandemics. I mean, that has to be part of it. We should harden our defences against rogue strands of RNA. Staff the labs. Stock up on swabs. But if all we learn is that, the most obvious point, we’re missing the big upside.

The opportunity here is to learn the pattern. The next major crisis probably won’t be a pandemic. It will be something else we’ve gone through before, swore we would never endure again and are busily forgetting.

An earthquake? A volcano? Floods? A financial crisis? A computer virus? Terrorism? Rising fascism? A big war?

Flood marker, Albury NSW

The incidence of these events comes in a Pareto distribution, as discussed in Part 1. Occasionally severe versions clump together and scare us senseless. Occasionally they disappear, lulling us into a state of complacency. We encounter a lot of the mild versions of each class of disaster – low floods, gentle earthquakes – and begin to see them as regular benign background events. But in a Pareto distribution a majority of the impact comes from a tiny fraction of the instances. Yes, the last computer virus hit a few hospitals who recovered quickly. The next will be small too. The one after that though? It could be the big one.

Disaster memory is a thrilling field to be learning about. I started thinking about how we remember disasters a couple of months ago. Before long, I found I couldn’t stop thinking about it, and began looking for information. Often that’s a dead end. But in this case, boom. Loads of research! And it’s fresh. This is a major area of interest right now. The researchers are young, dynamic and they are active.

THE HOWLING WIND

I jumped on Skype last week with a guy from Cambridge called Dr Rory Walshe. He has done a ton of really amazing field work on cyclones in Mauritius. That’s right, his latest research required him to quit rainy England for a tropical island, so you know he’s a smart guy.

Walshe’s paper on that research was published in the International Journal of Disaster Risk Reduction in 2020. Cyclones are a particularly important type of disaster to remember accurately. Because the eye of a cyclone is a trap. If you forget that a cyclone has a lull then returns with a vengeance, you can be a long way from safety when the wind returns.

Walshe’s research involved over 130 community interviews with citizens on what they remember about cyclones. It revealed, in some pockets, dangerous beliefs about the cyclone eye.

“If the rain stops and the wind goes away, it is safe to go outside, it never comes back,” said one respondent.

You might think old timers would know about the eye of the storm and kids would be ignorant.

But Walshe finds the picture is more complex:

“The results demonstrate that the dynamics of forgetting are not as simple as a steady demographic churn over time as eyewitnesses pass away. Cyclones (and other events) are not forgotten in a gradual, uniform or passive process over time, contrary to the statement; “the forgetting curve is logarithmic, the more time that has passed since an event, the weaker are the memories about it” (Fanta et al., 2019). Mauritius demonstrates several exceptions to this statement and those like it, which suggests that the creation and loss of memory is a complex process.”

It isn’t just time that kills memories. They don’t die of old age. We kill them. And the weapon of choice is narratives we create to explain the world as we experience it.

“Throughout the history of Mauritius there were periods when we were cyclone free, and people attributed that to the island being deforested, [they said] cyclones will not come anymore.” – Mauritius expert interviewee, reported by Walshe.

Nothing could be more natural than for people to create narratives to explain their perceptions. Long quiet periods get explanations – perfect, simple and wrong – and those explanations, when the next disaster comes, are fatal. In Mauritius it has now been quite a long time between cyclones, and dangerous beliefs are rising.

“We have noticed climate change here; summer is very hot, and winter is very cold. that’s due to climate change, and its why we will not have the same kind of cyclones like we used to have,” – Mauritius community interviewee, reported by Walshe.

Hearing about how Mauritius explains away cyclones, I can’t help thinking about The Great Moderation. This once-popular theory on why recessions were so rare these days reached peak popularity in the 2000s …. just prior to the Global Financial Crisis. Among the anguished howls of the millions cast into enduring unemployment, if you listened closely, you could hear the embarrassed murmuring of the macroeconomists.

Lucas, you sweet summer child. This was published in 2003.

The belief recession risk had been moderated might even have been a contributing factor in regulators permitting all those crazy home loans. Speaking about dangerously glib explanations, we should also cast a side-eye at the Golden Arches Theory of Global Conflict, the very appealing claim that two countries with a McDonald’s have never gone to war. The implication is economic linkages reduce the risk of major global conflict. (Of course China and America seem to be fighting because of trade as much as anything.)

A medium Sprite and a side of global peace, thanks.

PINING FOR THE CALDERAS

When I spoke to Walshe, he felt a bit cloistered by the pandemic. Supposed to be in South America right now learning how societies respond to the threat of volcanic eruptions he is instead trapped in a flat somewhere in the UK. About six times during our conversation he expressed his desire to be in Patagonia instead of at home!

Rory was a delight to speak to, well-informed, insightful, generous with his time. He apologised afterwards for being “off his game” having had the AstraZeneca vaccine the day before our chat and suffering through a sleepless feverish night. I hadn’t noticed he was off his game, but the fact of his vaccination brought to the forefront the reason for my inquiries: the pandemic.

We began to forget the Spanish Flu almost as soon as it had ended. What other events are out there, ignored by history, waiting to come back and bite us?